Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Milestones

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

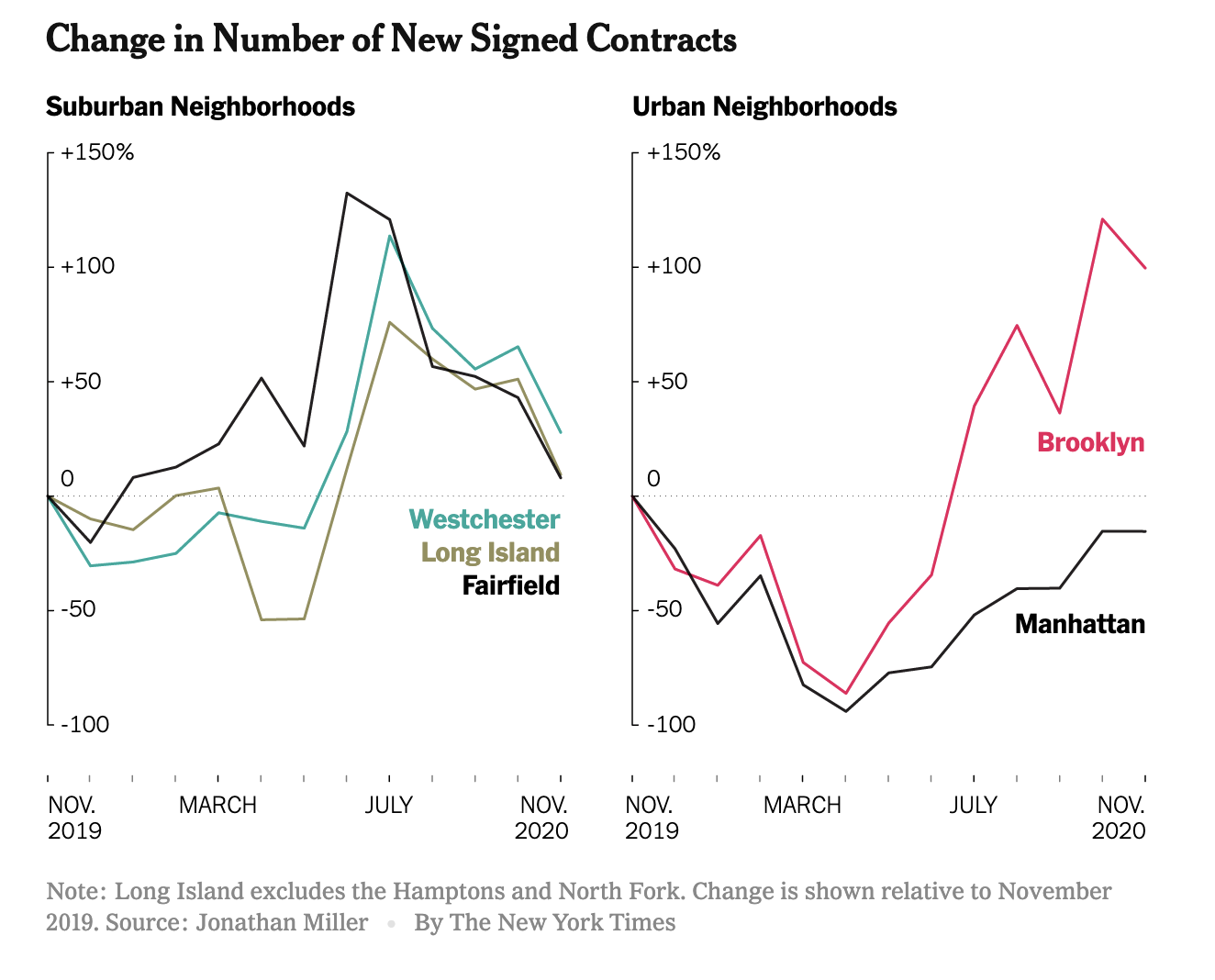

Peak Suburb Has Passed

read more

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

March 24, 2020

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Weather & Natural Disasters

Real estate appraisers are an essential business and here to protect the public trust

read more

March 18, 2020

Affordability, Affordable Housing

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Explainer

,

Homebuying Process

,

International

,

Weather & Natural Disasters

Flattening The Curve And Seeing The Shift From Greed To Fear

read more

December 28, 2019

Manhattan

Manhattan Annual Price Records By Property Type Since 1982

read more

April 27, 2019

Appraising

,

Continuing Education & Licensing

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

BREAKING The New York State AMC Law Is Now In Effect

read more

March 19, 2019

Affordability, Affordable Housing

,

Brooklyn

,

Government, Politics, Regulations & Policy

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Taxes, Insurance, Fees

The Proposed NYC “Pied-A-Terre Tax” Looks Catastrophic to NYC Real Estate

read more

November 30, 2018

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Remember liar loans of a decade ago? Those same people want to do away with appraisers.

read more

September 11, 2018

Bloomberg TV

,

Credit, Finance, Mortgage, Rates

,

International

,

Luxury, Super, Ultra, Mega

,

Manhattan

Bloomberg Markets TV: September 11, 2018, Looking back at 9/11 and the Financial Crisis

read more

January 11, 2018

Analysis & Research

,

Bloomberg TV

,

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Interviews

,

Manhattan

,

Market Reports

,

Queens

,

Westchester County, NY

[Media] Bloomberg Markets Interview January 11, 2018

read more

December 27, 2017

Bloomberg TV

,

Explainer

,

Media

,

Taxes, Insurance, Fees

Bloomberg TV – Housing Related Issues in Final Version of the Tax Cut and Jobs Act of 2017

read more

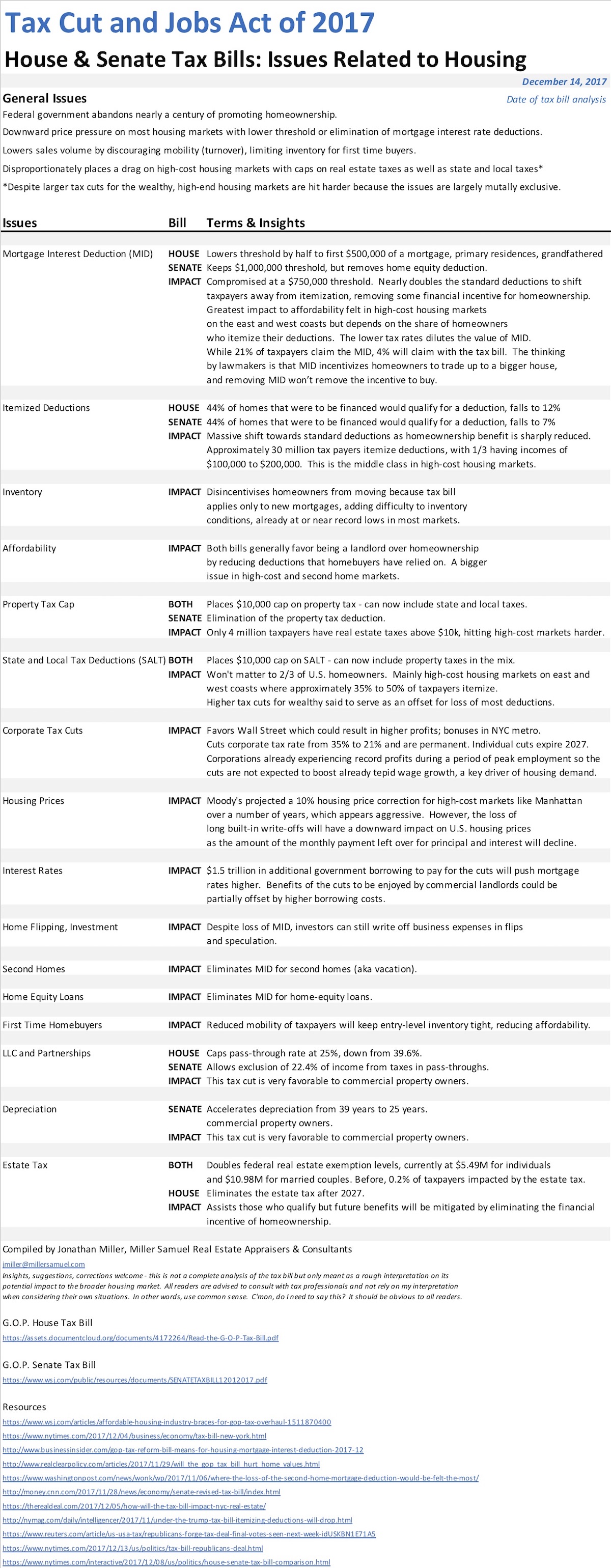

December 14, 2017

Explainer

How the GOP Tax Bill Might Impact U.S. Residential Real Estate

read more

1

2

Next

Load More Posts

Page load link

Go to Top