Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Luxury, Super, Ultra, Mega

April 1, 2023

Luxury, Super, Ultra, Mega

,

New York City

,

Wall Street, Financial Services

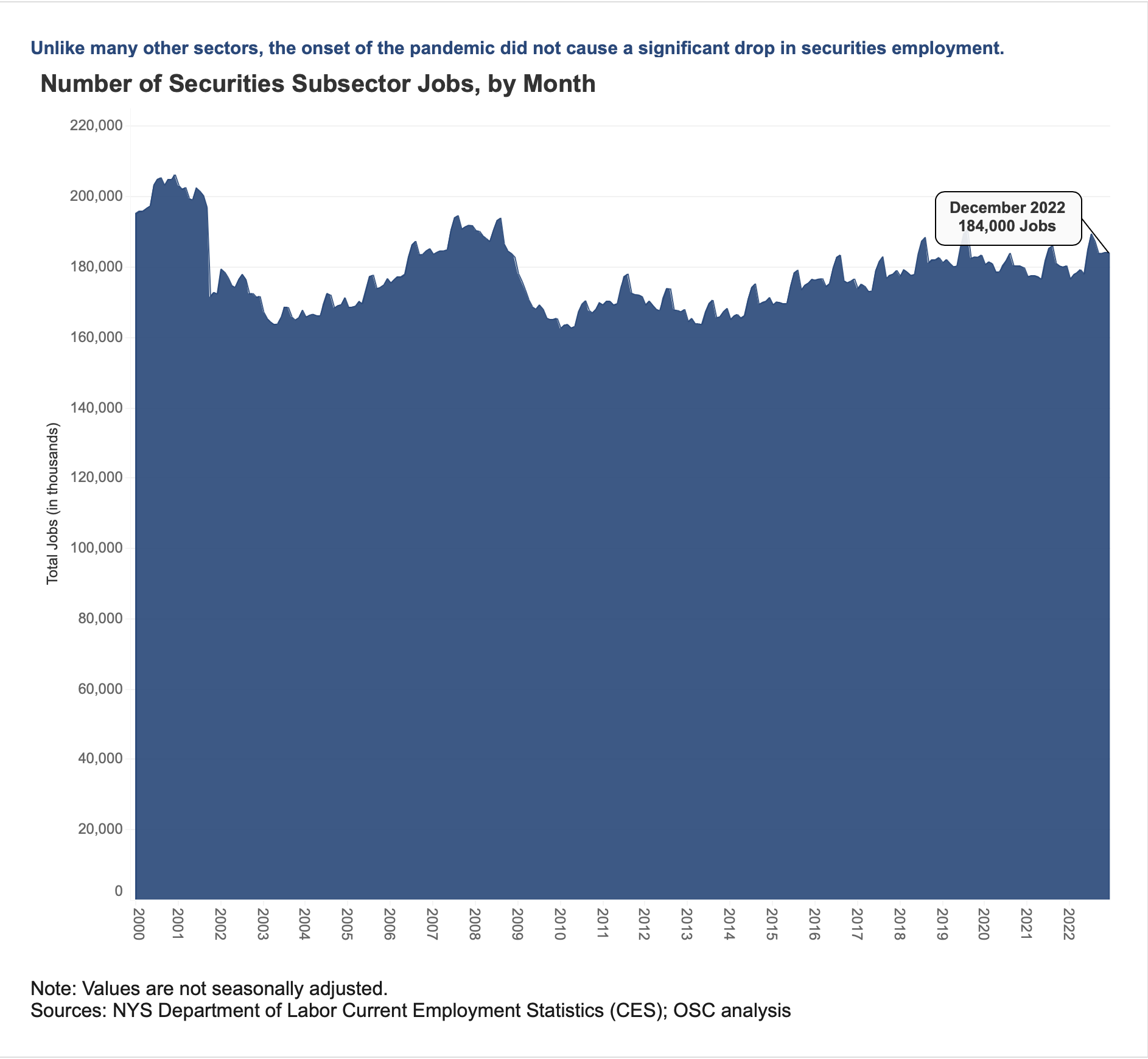

Wall Street Bonuses Fall To Pre-Pandemic Levels

read more

January 23, 2020

Affordability, Affordable Housing

,

Brick Underground

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

The Brick Underground Podcast: 1-23-20 Talking Peak Uncertainty

read more

January 7, 2020

Charts, Maps, Images, Infographics, Video

,

Luxury, Super, Ultra, Mega

,

Manhattan

NY1 Delves Into The Cause of the Manhattan Supertall Skyscraper Boom

read more

January 7, 2020

Bloomberg TV

,

Luxury, Super, Ultra, Mega

,

Manhattan

Bloomberg Markets 1-6-20: Manhattan High-End Hurt By New Tax Laws

read more

December 4, 2019

Bloomberg TV

,

Los Angeles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Miami (Beach + Mainland)

Bloomberg TV 12-3-19: Super Luxury Oversupply

read more

July 6, 2019

Charts, Maps, Images, Infographics, Video

,

Cheddar

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Sales

My July 3, 2019 Cheddar Interview on the NYSE Floor

read more

May 16, 2019

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Hamptons/North Fork

,

Luxury, Super, Ultra, Mega

,

New York Times

,

Statistics, Metrics & Data

Hamptons Sellers Are Starting To Get The Message

read more

May 16, 2019

Charts, Maps, Images, Infographics, Video

,

Commercial, Retail

,

Luxury, Super, Ultra, Mega

,

Manhattan

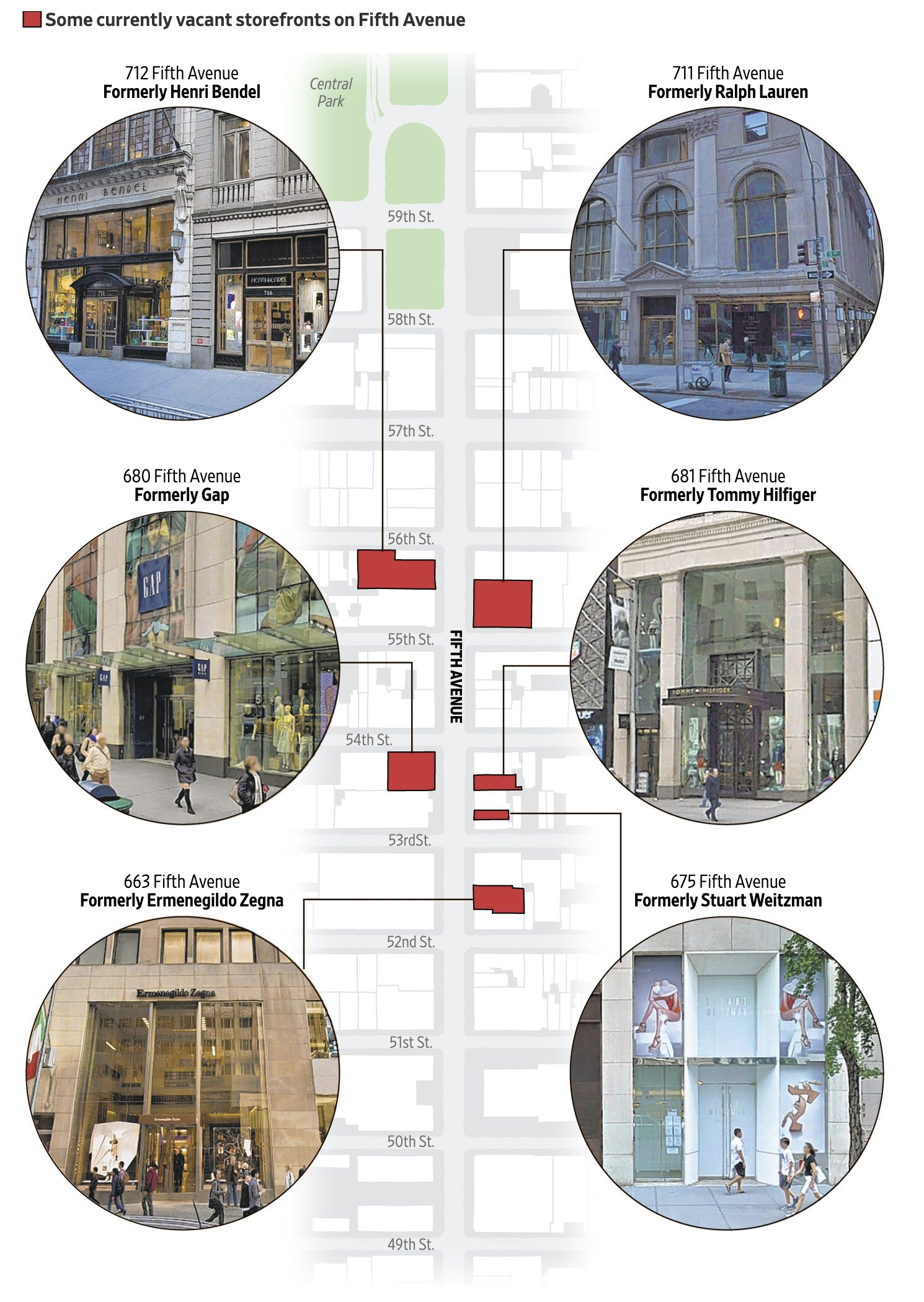

[Inside Edition TV] The Fifth Avenue Retail Apocolypse?

read more

May 4, 2019

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Post

Billionaires Row Continues to be Challenged

read more

May 4, 2019

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

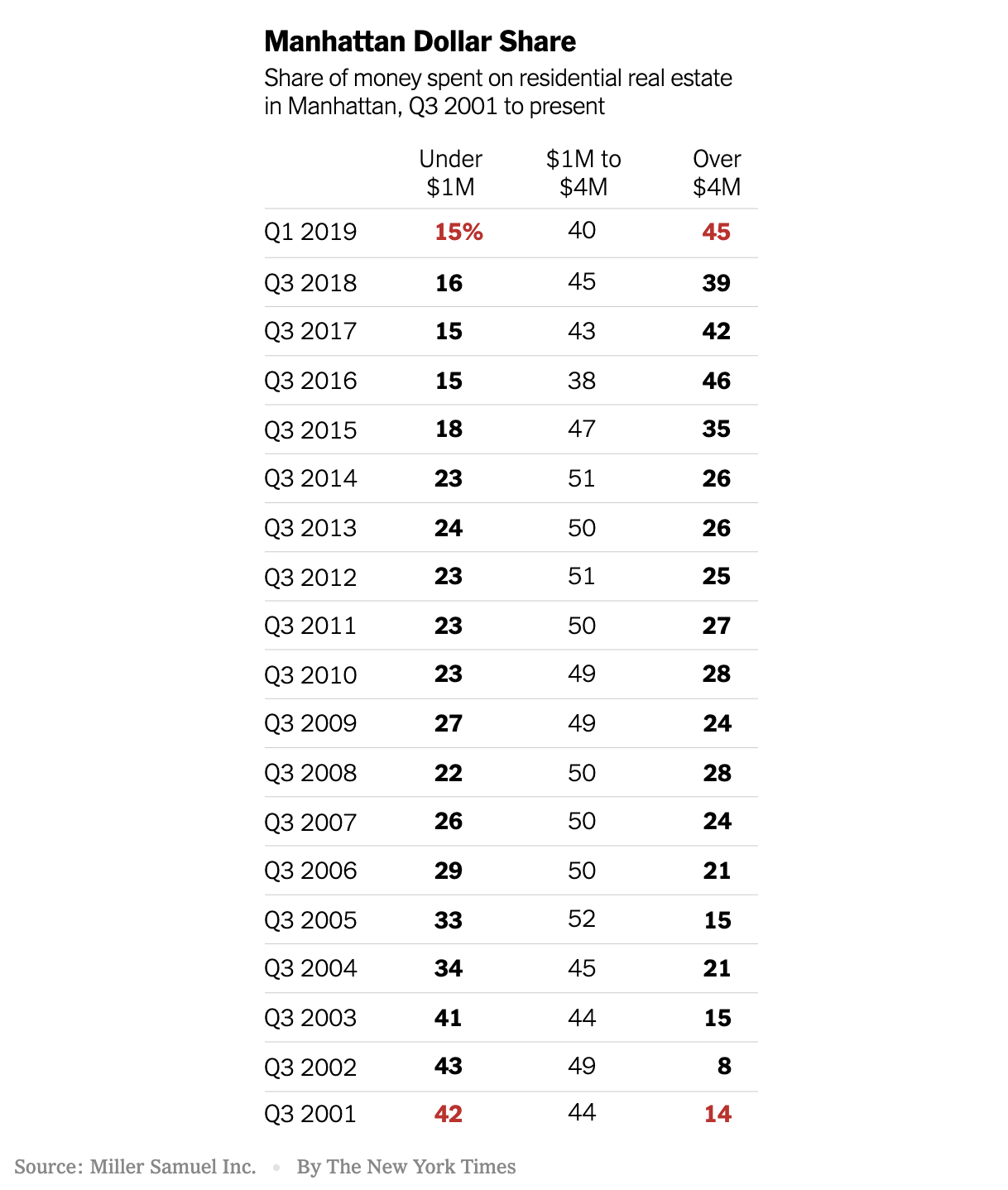

NYT Infographic: Manhattan Real Estate Shift To High End, Illustrated

read more

April 27, 2019

CNBC

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Luxury, Super, Ultra, Mega

,

Sales

,

Taxes, Insurance, Fees

,

Wall Street, Financial Services

CNBC TV 4-25-19 Coverage of Elliman Reports on Greenwich and Fairfield County, CT

read more

March 19, 2019

Affordability, Affordable Housing

,

Brooklyn

,

Government, Politics, Regulations & Policy

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Taxes, Insurance, Fees

The Proposed NYC “Pied-A-Terre Tax” Looks Catastrophic to NYC Real Estate

read more

1

2

Next

Load More Posts

Page load link

Go to Top