Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Brokers, Agents, MLS, NAR

December 27, 2023

Bloomberg Radio

,

Brokers, Agents, MLS, NAR

,

Homebuying Process

Bloomberg’s At The Money Podcast (ATM): The Best Way To Sell A House

read more

November 17, 2023

Bloomberg Radio

,

Brokers, Agents, MLS, NAR

,

Homebuying Process

Bloomberg’s At The Money Podcast (ATM): The Best Way To Buy A House

read more

June 28, 2020

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

New York City

,

Op-Ed

My Forbes Column: Keeping Housing Market Results From The Public Is Never Justified: An Expansive View

read more

April 29, 2020

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Contract Data Is Pending Data Is Lagging Data

read more

January 23, 2020

Affordability, Affordable Housing

,

Brick Underground

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

The Brick Underground Podcast: 1-23-20 Talking Peak Uncertainty

read more

January 15, 2020

Appraising

,

Brokers, Agents, MLS, NAR

,

Douglas Elliman

[Podcast] The World of Real Estate with Frances Katzen – Jonathan Miller

read more

August 16, 2016

Aspen

,

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

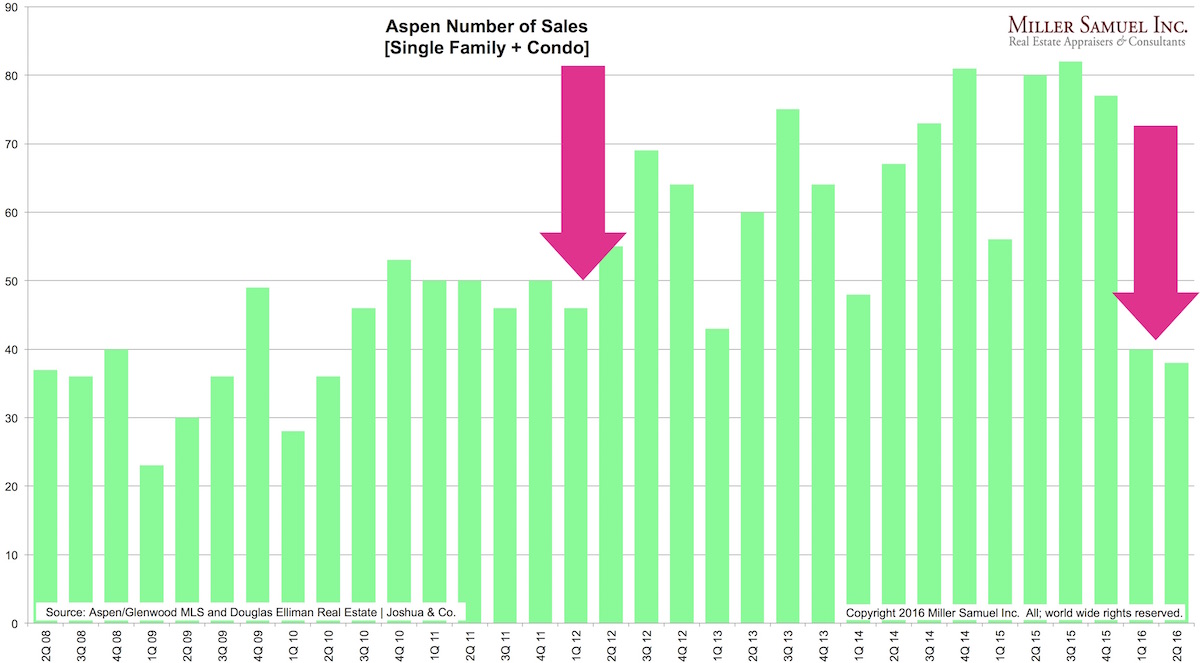

Aspen Sales “Nosedive” as U.S. Luxury Market Returns to Sea Level

read more

May 12, 2016

Amenities, Adjustments & Value Logic

,

Boards & Associations

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

How Not to Value A Co-op Apartment: Price per Share

read more

December 31, 2015

Bloomberg Radio

,

Bloomberg TV

,

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

,

Paris, France

Bloomberg TV’s Surveillance on 12-31-2015

read more

October 4, 2015

Appraising

,

Brokers, Agents, MLS, NAR

,

IRS

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Law, Ethics & Fraud

Multi-millionaire Motivational Speaker Dean Graziosi Shares His Appraisal Wisdom

read more

March 1, 2015

Blogging Off The Matrix

,

Bloomberg View

,

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Homebuying Process

,

Housing Trends & Cycles

Bloomberg View Column: Real-Estate Agents Ride High Again

read more

July 28, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Brokers, Agents, MLS, NAR

,

Op-Ed

,

Trulia

,

Wall Street, Financial Services

,

Washington DC

My First Post on Bloomberg View: Homebuying Gets a Housecleaning

read more

1

2

Next

Load More Posts

Page load link

Go to Top