Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Brokers, Agents, MLS, NAR

June 28, 2014

Amenities, Adjustments & Value Logic

,

Brokers, Agents, MLS, NAR

,

Celebrity, Pop Culture

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Records, Thresholds and Outliers

,

Wall Street Journal

Cluttering Luxury Housing Markets with Listings Made for TV – Manhattan Edition

read more

June 28, 2014

Adventures in Media & Marketing

,

Brokers, Agents, MLS, NAR

Gold Jacket: How Does The Real Estate Brokerage Industry Change Its Image?

read more

June 23, 2014

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

New Angle: Blame Low Mortgage Rates

read more

June 8, 2014

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Migration, Psychology, Demographics

Status Quo Bias: ‘Linear” Thinking in the Real Estate Industry

read more

April 28, 2014

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

IRS

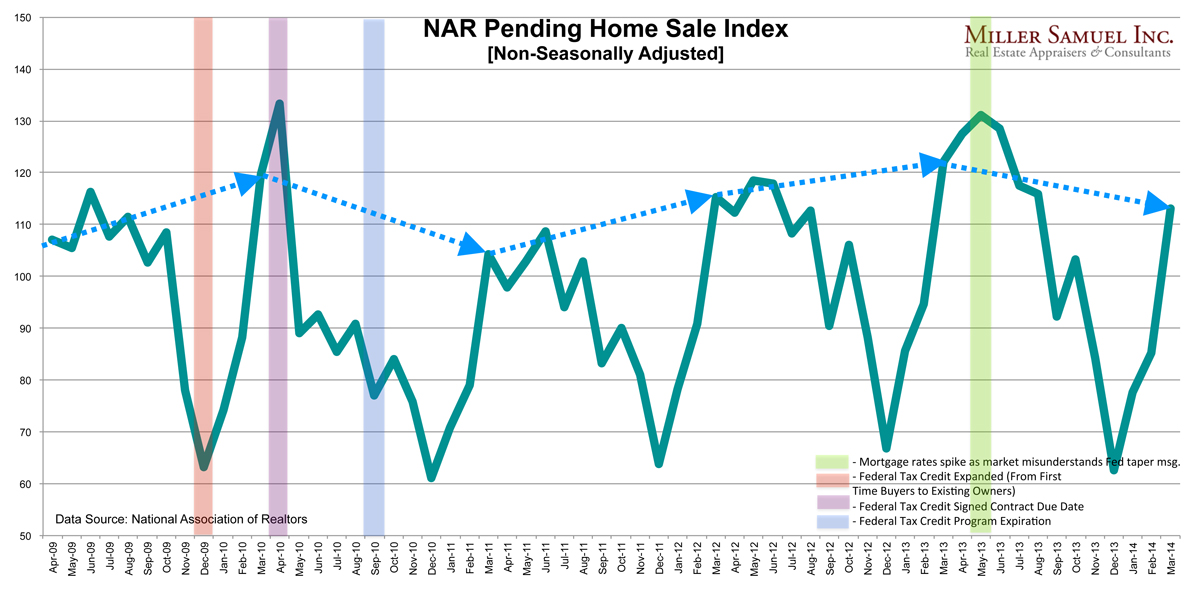

NAR Pending Home Sales Had Biggest “February to March” Jump in 4 Years

read more

March 29, 2014

Books & Movies

,

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Homebuying Process

,

International

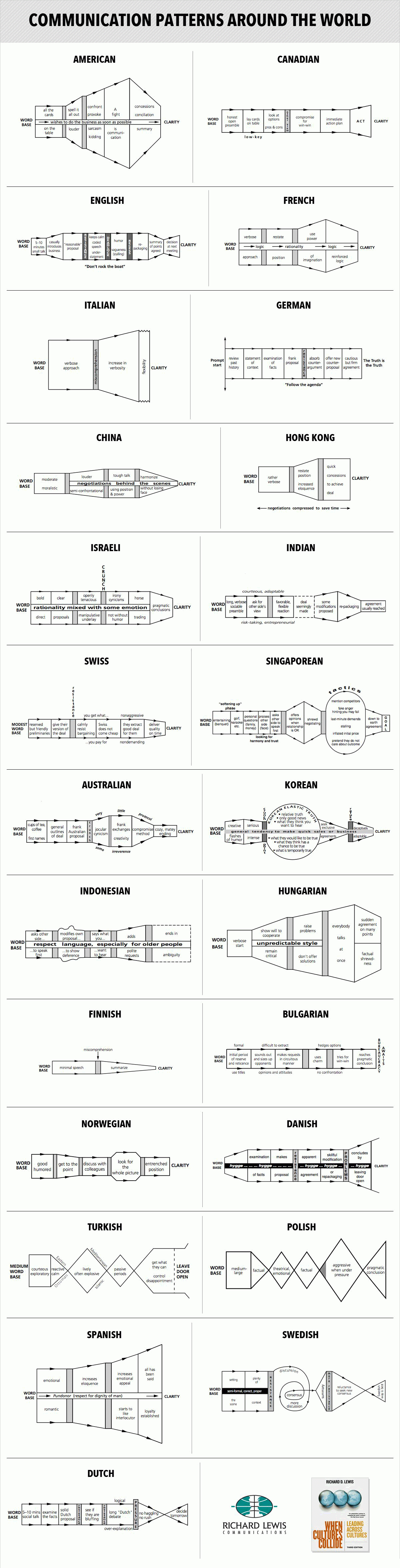

How Real Estate Brokers Can Negotiate With Foreign Buyers, Illustrated

read more

February 14, 2014

Bloomberg News

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Trends & Cycles

,

Media

On Bloomberg TV’s ‘Bottom Line’ 2-12-14 Talking US Housing Slowdown

read more

October 28, 2013

Brokers, Agents, MLS, NAR

,

Market Reports

,

New York Times

NAR Pending Home Sale Index Sort of Goes Negative

read more

August 21, 2013

Brokers, Agents, MLS, NAR

,

Housing Indices & Portals

NAR July 2013 US Existing Home Sales Unexpectedly Rise 6.5% M-O-M

read more

July 1, 2013

Brokers, Agents, MLS, NAR

,

Elliman Reports

NAR: “The Home Price Growth Is Too Fast”

read more

March 14, 2013

Brokers, Agents, MLS, NAR

,

Public Speaking

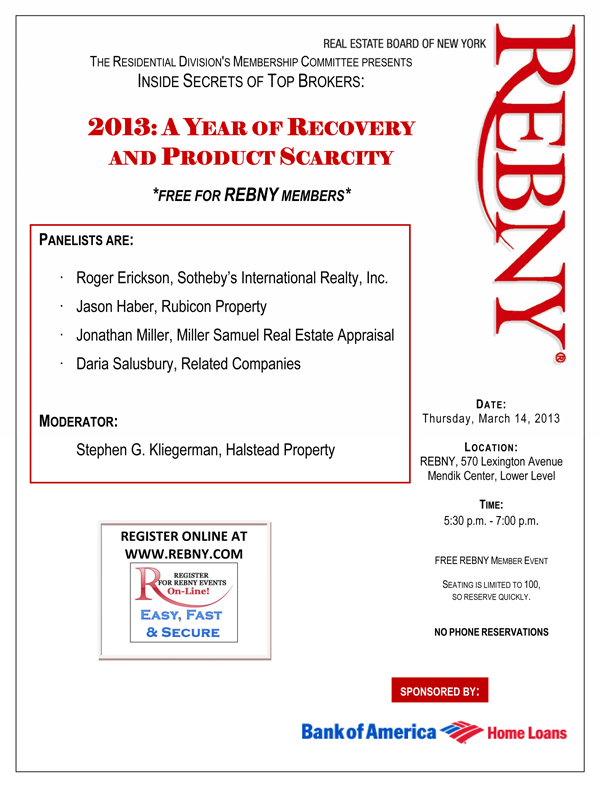

Speaking 3-14-13 REBNY – A Year of Recovery and Product Scarcity

read more

January 27, 2013

Adventures in Media & Marketing

,

Appraising

,

Brokers, Agents, MLS, NAR

,

New York Times

Broken Appraisal: Lack of Market Knowledge Overpowers Lack of Data

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top