Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› International

March 28, 2020

Charts, Maps, Images, Infographics, Video

,

International

,

Weather & Natural Disasters

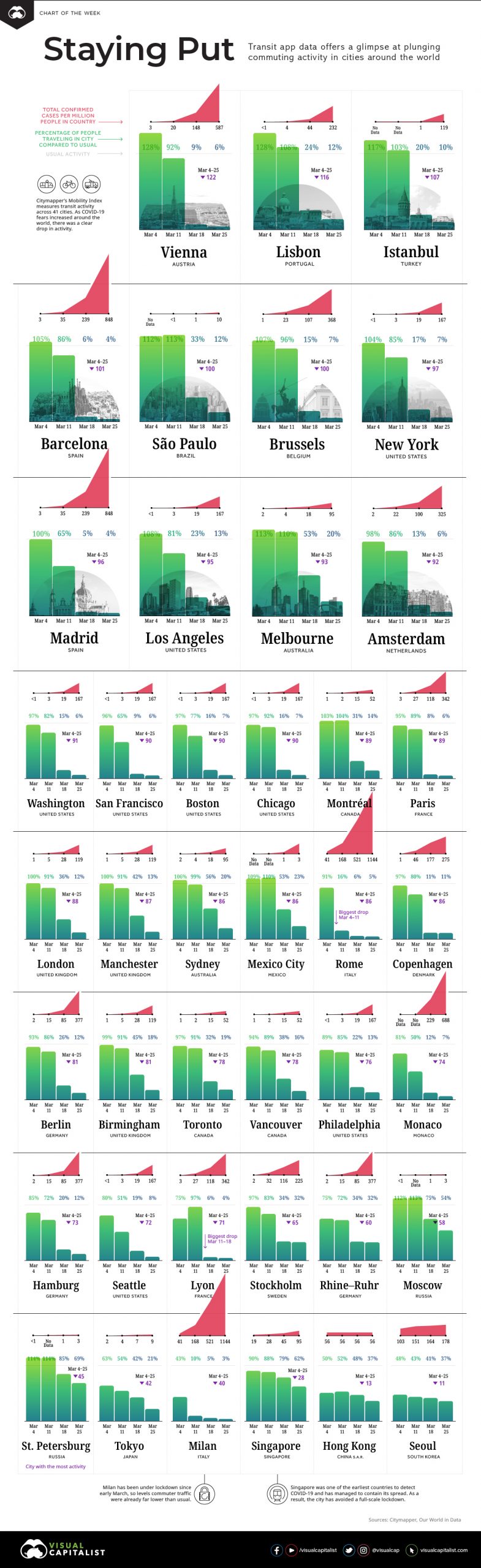

Staying Put Locally = Saving Lives Globally

read more

March 18, 2020

Affordability, Affordable Housing

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Explainer

,

Homebuying Process

,

International

,

Weather & Natural Disasters

Flattening The Curve And Seeing The Shift From Greed To Fear

read more

September 11, 2018

Bloomberg TV

,

Credit, Finance, Mortgage, Rates

,

International

,

Luxury, Super, Ultra, Mega

,

Manhattan

Bloomberg Markets TV: September 11, 2018, Looking back at 9/11 and the Financial Crisis

read more

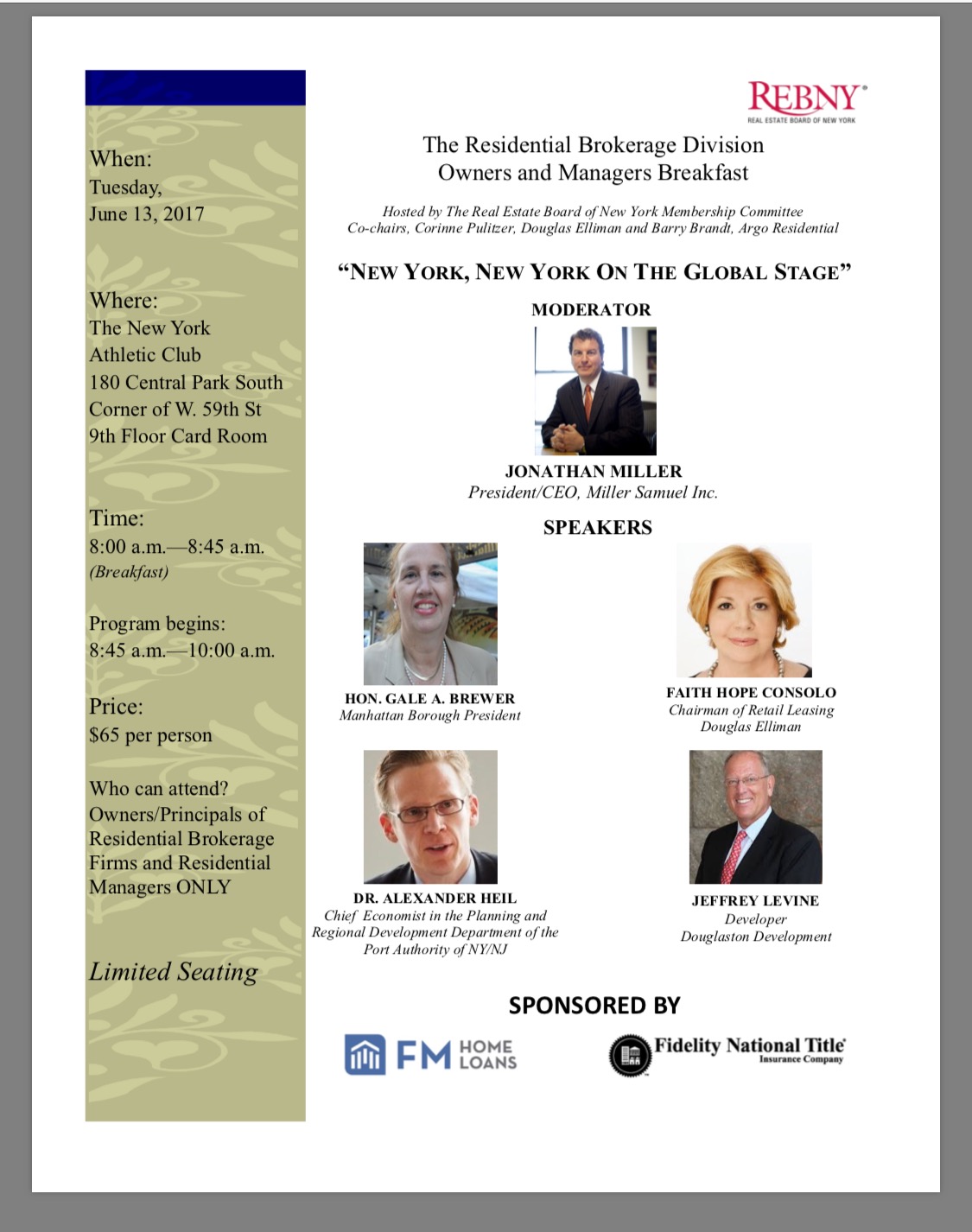

May 28, 2017

International

,

Manhattan

,

Public Speaking

,

REBNY

Moderating REBNY Panel: New York, New York On The Global Stage

read more

November 27, 2016

China

,

Development, Construction, Architecture & Land

,

International

,

The Real Deal

China: A Housing Market Without Re-sales?

read more

December 1, 2015

Charts, Maps, Images, Infographics, Video

,

International

,

Market Reports

,

New York City

,

New York Times

,

Rentals, Investing

,

Wall Street Journal

NYT v. WSJ Smogdown: Status of Chinese Investment in U.S. Real Estate

read more

August 31, 2015

Charts, Maps, Images, Infographics, Video

,

Commercial, Retail

,

Development, Construction, Architecture & Land

,

International

,

Manhattan

,

Media

,

Yahoo! Finance

[Video] China’s investors and the safe haven of American real estate

read more

July 15, 2015

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

International

Will London (or any large city) Become a Bad Version of Dubai?

read more

July 5, 2015

Celebrity, Pop Culture

,

Fox Business

,

International

,

Media

[Video] Fox Business Risk & Reward w/Deirdre Bolton 7-2-2015

read more

May 4, 2015

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

International

,

Knight Frank

,

Manhattan

,

Rentals, Investing

Bloomberg View Column: Invest in a Painting, Not a Condo

read more

April 29, 2015

Adventures in Media & Marketing

,

Development, Construction, Architecture & Land

,

International

,

Migration, Psychology, Demographics

,

New York Times

[VIDEO] Chinese Housing Bubble Version of ‘The Truman Show’

read more

February 9, 2015

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

International

,

Law, Ethics & Fraud

,

Los Angeles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

,

South Florida

Good and Bad Super-Luxury Condo Buyers Love the LLC

read more

1

2

Next

Load More Posts

Page load link

Go to Top