Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Amenities, Adjustments & Value Logic

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

September 26, 2019

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Trends & Cycles

,

Manhattan

Talking Manhattan Podcast: The Market’s Underlying Issues, and How to Value Outdoor space

read more

January 28, 2018

Affordability, Affordable Housing

,

Amenities, Adjustments & Value Logic

,

Charts, Maps, Images, Infographics, Video

,

Commercial, Retail

,

Interviews

The Full Nelson: Tax Reform Impact on Residential and Commercial Real Estate

read more

October 29, 2017

Amenities, Adjustments & Value Logic

,

Explainer

Explainer: Overall Median Sales Price Submarket Changes May Not Fall In Range

read more

May 12, 2016

Amenities, Adjustments & Value Logic

,

Boards & Associations

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

How Not to Value A Co-op Apartment: Price per Share

read more

April 26, 2015

Amenities, Adjustments & Value Logic

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Housing Trends & Cycles

Bloomberg View Column: Want a New House? Good Luck

read more

April 26, 2015

Amenities, Adjustments & Value Logic

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

Bloomberg View Column: House Rich, Land Poor

read more

November 29, 2014

Amenities, Adjustments & Value Logic

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Manhattan

,

Rentals, Investing

[Three Cents Worth #272 NY] The Cost Of Your Doorman Keeps Rising

read more

October 30, 2014

Amenities, Adjustments & Value Logic

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Manhattan

[Three Cents Worth #270 NY] What Is the Value of a Central Park View?

read more

August 1, 2014

Amenities, Adjustments & Value Logic

,

Analysis & Research

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

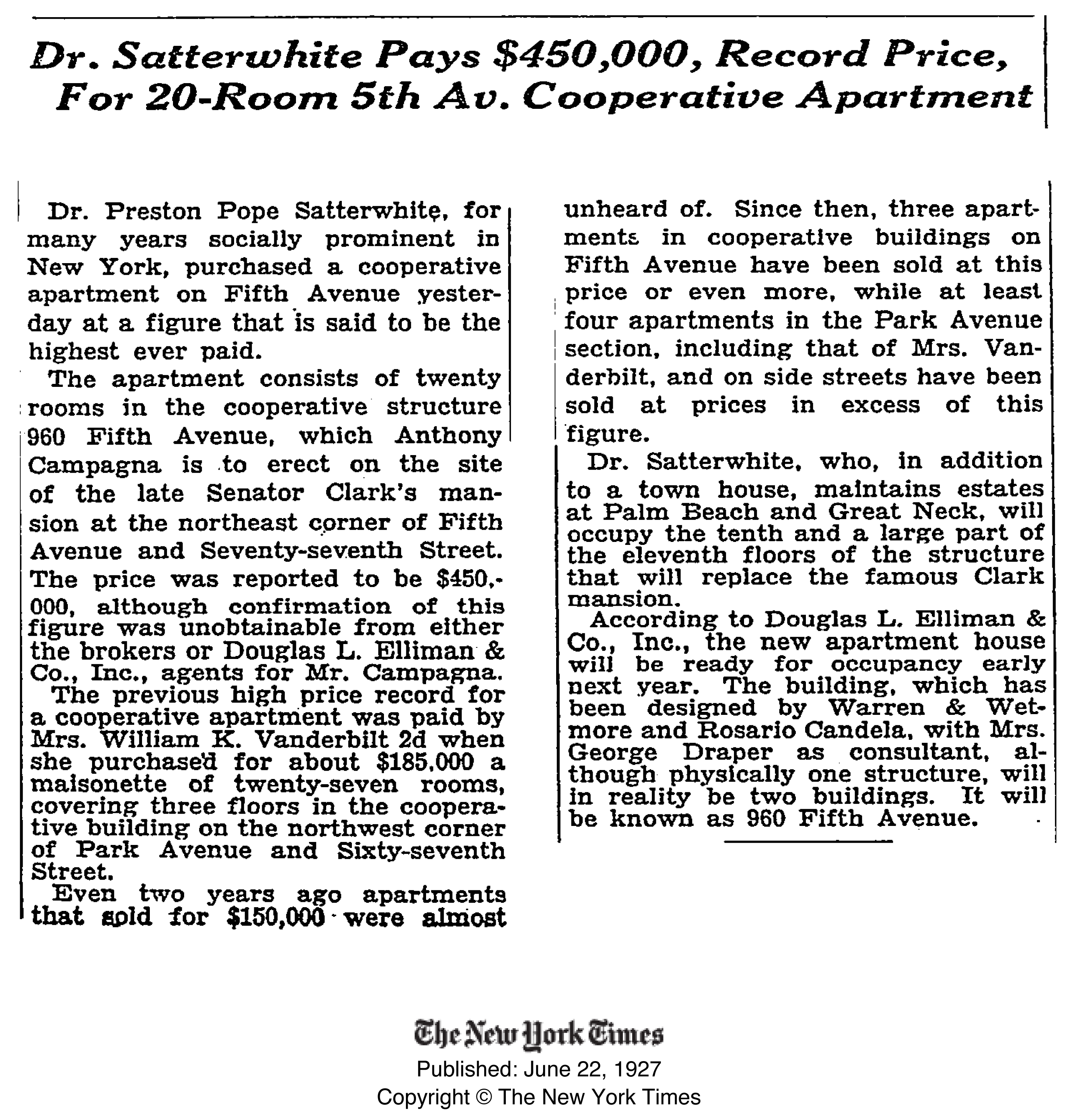

A Fifth Avenue Co-op’s 87-Year Price Increase was 3.6X Rate of Inflation

read more

July 12, 2014

Adventures in Media & Marketing

,

Amenities, Adjustments & Value Logic

,

Brooklyn

,

Homebuying Process

,

Migration, Psychology, Demographics

,

New York Magazine

…and the Home Seller will give you a Free Tesla!

read more

June 28, 2014

Amenities, Adjustments & Value Logic

,

Brokers, Agents, MLS, NAR

,

Celebrity, Pop Culture

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Records, Thresholds and Outliers

,

Wall Street Journal

Cluttering Luxury Housing Markets with Listings Made for TV – Manhattan Edition

read more

1

2

Next

Load More Posts

Page load link

Go to Top