Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› New York Magazine

January 28, 2015

Affordability, Affordable Housing

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Media

,

New York Magazine

Flipping Out About East Brooklyn’s Gentrification

read more

July 12, 2014

Adventures in Media & Marketing

,

Amenities, Adjustments & Value Logic

,

Brooklyn

,

Homebuying Process

,

Migration, Psychology, Demographics

,

New York Magazine

…and the Home Seller will give you a Free Tesla!

read more

March 25, 2014

Amenities, Adjustments & Value Logic

,

Manhattan

,

Media

,

New York Magazine

Repost: Measuring Manhattan Values By Floor Level

read more

February 25, 2013

Brooklyn

,

Manhattan

,

Media

,

New York Magazine

NY Mag: Suggestions For Splitting The Rent

read more

February 3, 2013

Amenities, Adjustments & Value Logic

,

Appraising

,

Furman Center

,

New York Magazine

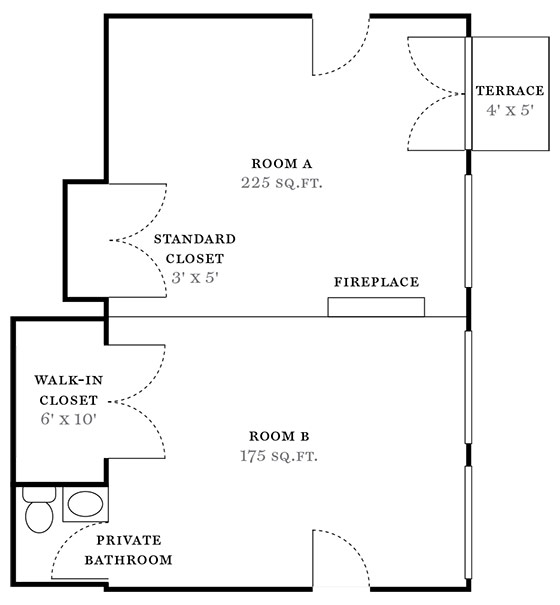

Valuing A Fireplace

read more

December 3, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

New York Magazine

,

New York Times

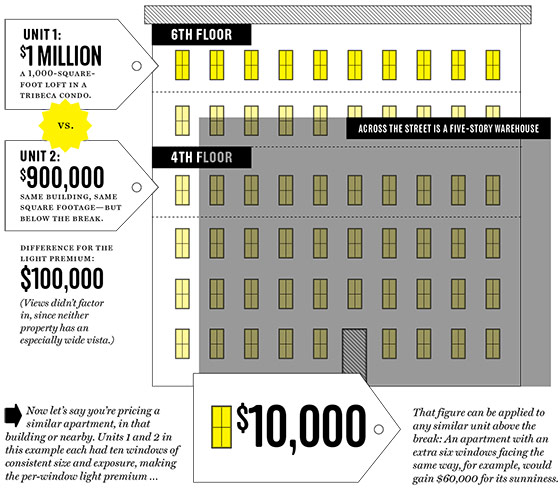

Valuing the Light in Your Condo or Co-op

read more

November 6, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

International

,

Knight Frank

,

Luxury, Super, Ultra, Mega

,

Market Reports

,

New York Magazine

,

The Real Deal

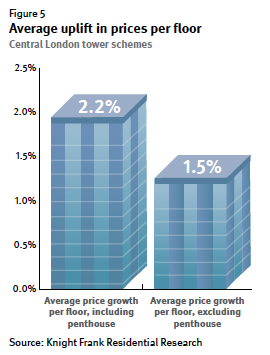

Knight Frank Tall Towers Report Shows London With Similar Manhattan Height Premium

read more

November 4, 2012

Language, Jargon & Quotes

,

Manhattan

,

New York Magazine

,

Weather & Natural Disasters

[Sandy] The SoPo New York Magazine Cover

read more

September 6, 2012

Appraising

,

Manhattan

,

Media

,

New York Magazine

Literally The Narrowest Housing Insight Ever Provided (Hint: Valuing Outdoor Space)

read more

October 26, 2009

Amenities, Adjustments & Value Logic

,

Distressed Housing

,

Humor or Whimsy

,

New York Magazine

[Central Park v. Detroit] $363,538,692,000 v. $4,500,000

read more

November 24, 2008

Boom Bubble Bust

,

Media

,

New York Magazine

,

New York Times

[In The Media] A1 For NYT & NY Mag’s Best Photo Shoot Ever

read more

April 24, 2008

Appraising

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

New York Magazine

,

New York Times

,

Rentals, Investing

[AAA] Ratings Agencies And The New Culture Of Partnership

read more

1

2

Next

Load More Posts

Page load link

Go to Top