Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Distressed Housing

May 7, 2020

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

,

Weather & Natural Disasters

Manhattan Crisis: What Does Our Housing Past Tell Us About Our Housing Future?

read more

February 16, 2016

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Homebuying Process

Contrarians React to Quicken Loans Rocket Mortgage Outrage

read more

September 23, 2015

Books & Movies

,

Boom Bubble Bust

,

Distressed Housing

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

The Big Short: The Movie Coming this December

read more

May 21, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Distressed Housing

,

Douglas Elliman

,

Housing Trends & Cycles

,

Miami (Beach + Mainland)

[Three Cents Worth #284 Miami] Miami Drill Down: Picking Up the Scraps of the Financial Crisis

read more

March 15, 2015

Affordability, Affordable Housing

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

Bloomberg View Column: Income Inequality Hits the Housing Market

read more

December 22, 2014

Boom Bubble Bust

,

Distressed Housing

,

Housing Trends & Cycles

,

Migration, Psychology, Demographics

Economic Bubble Theory Using Bubbles

read more

November 7, 2014

Analysis & Research

,

Blogging Off The Matrix

,

Bloomberg View

,

Distressed Housing

,

Rentals, Investing

,

Wall Street, Financial Services

Bloomberg View Column: Hedge-Fund Guys Have Foreclosure Fatigue

read more

June 9, 2014

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Housing Trends & Cycles

,

Op-Ed

,

Statistics, Metrics & Data

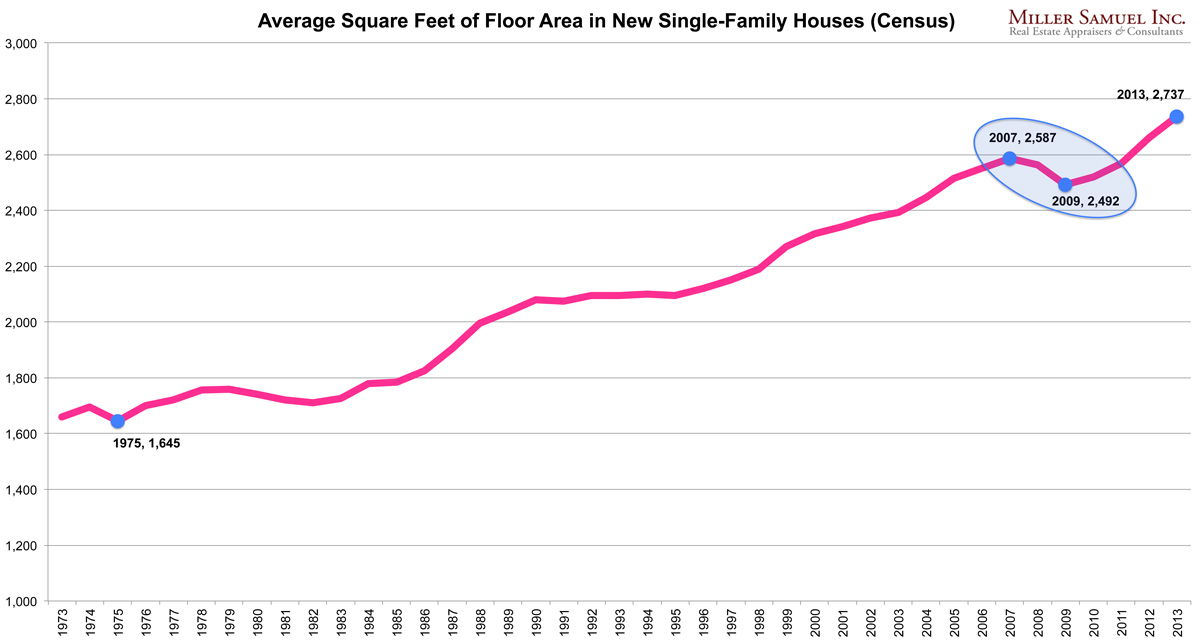

Trends in Home Size and Home Ownership React to Economic Conditions, Not Taste

read more

May 13, 2014

Backyard BBQ Talk

,

Books & Movies

,

Distressed Housing

,

Economy

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

[Vox Video] Housing Crash Fix Explained From Geithner’s Perspective

read more

January 27, 2013

Distressed Housing

,

Miami (Beach + Mainland)

Miami Hype Machine: “Sales Pace Slows Dramatically”

read more

December 14, 2012

Credit, Finance, Mortgage, Rates

,

Distressed Housing

Bank Forgives $1M+ on Short Sale But Lawn Looks Good

read more

December 6, 2012

Distressed Housing

,

New York Times

,

RealtyTrac

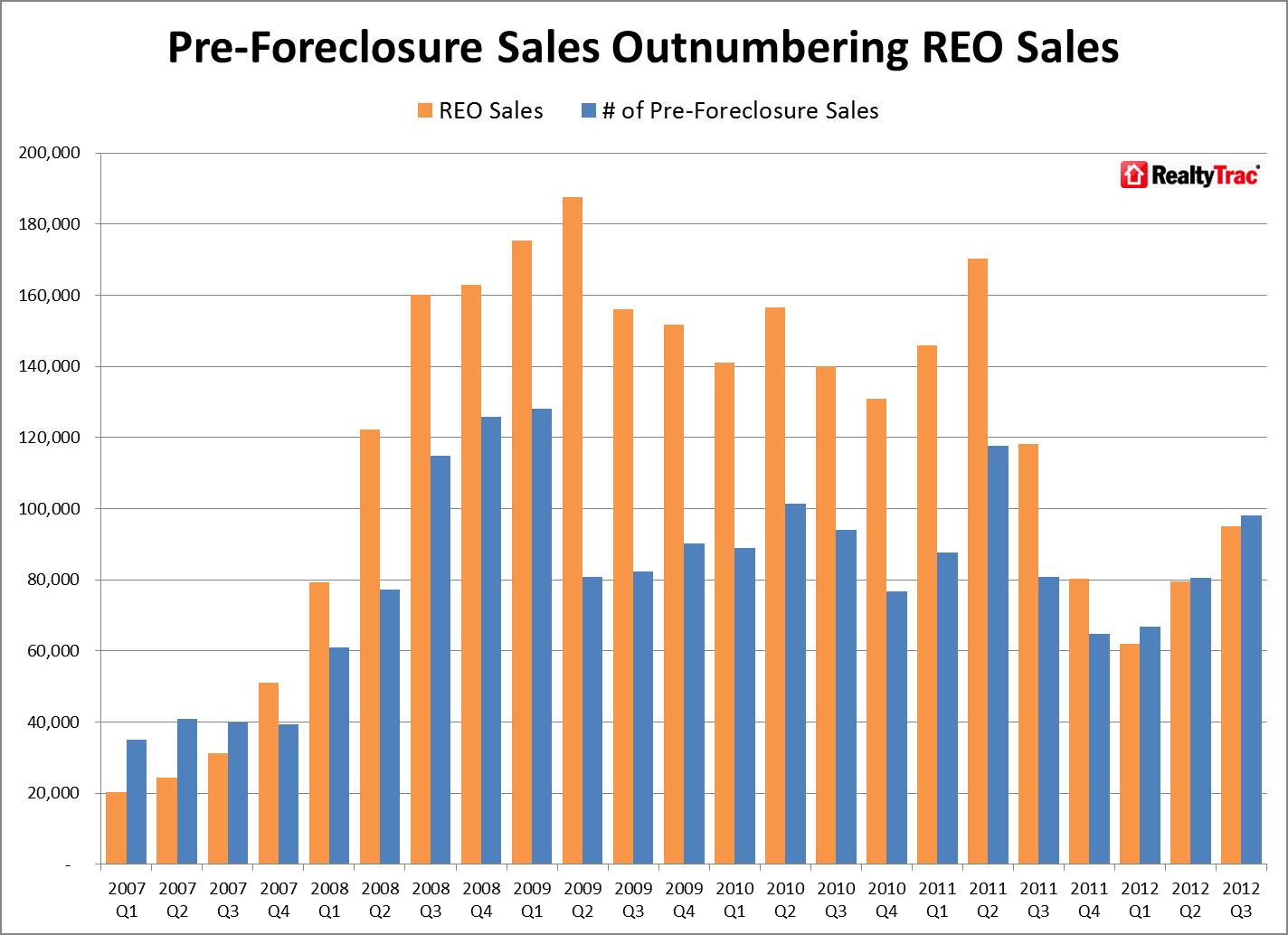

Ignore The False Positives, Foreclosure Sales Are Rising Again Now

read more

1

2

Next

Load More Posts

Page load link

Go to Top