Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Federal Reserve, New York

March 7, 2016

Analysis & Research

,

Federal Reserve, New York

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Weather & Natural Disasters

New Yorkers Are Busy During Week So Big Snowstorms Need to Occur On Weekends

read more

July 13, 2015

Charts, Maps, Images, Infographics, Video

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

Fed Charts: How are the Housing Fundamentals Doing?

read more

January 30, 2015

Analysis & Research

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York City

,

Statistics, Metrics & Data

NYC Economy is Expanding Rapidly

read more

June 16, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Economy

,

Federal Reserve, New York

Housing is a Drag: US Student Debt Bubble Made Worse by the Baby Boomer Nanny State

read more

May 13, 2014

Backyard BBQ Talk

,

Books & Movies

,

Distressed Housing

,

Economy

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

[Vox Video] Housing Crash Fix Explained From Geithner’s Perspective

read more

March 21, 2014

Charts, Maps, Images, Infographics, Video

,

Federal Reserve, New York

,

New Jersey

,

New York City

,

Statistics, Metrics & Data

NY Fed: New York City and State Expanding at “Brisk Pace”

read more

February 12, 2014

Appraising

,

Continuing Education & Licensing

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve, New York

,

Long Island

,

Public Speaking

,

Weather & Natural Disasters

[Pre-Nor’easter Keynote] Long Island Housing Market: Transitioning from “Recovery” to “Recovered”

read more

March 28, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

Money for Nothing Movie Trailer

read more

February 14, 2013

Celebrity, Pop Culture

,

Douglas Elliman

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

,

RealtyTrac

,

The Real Deal

Housing Data as Pop Culture

read more

February 6, 2013

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York Times

Tight Credit Is Causing Housing Prices to Rise

read more

December 4, 2012

Brooklyn

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

[NewYork Fed] Excellent Mapping of Housing’s Recovery Process in Region

read more

November 5, 2012

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

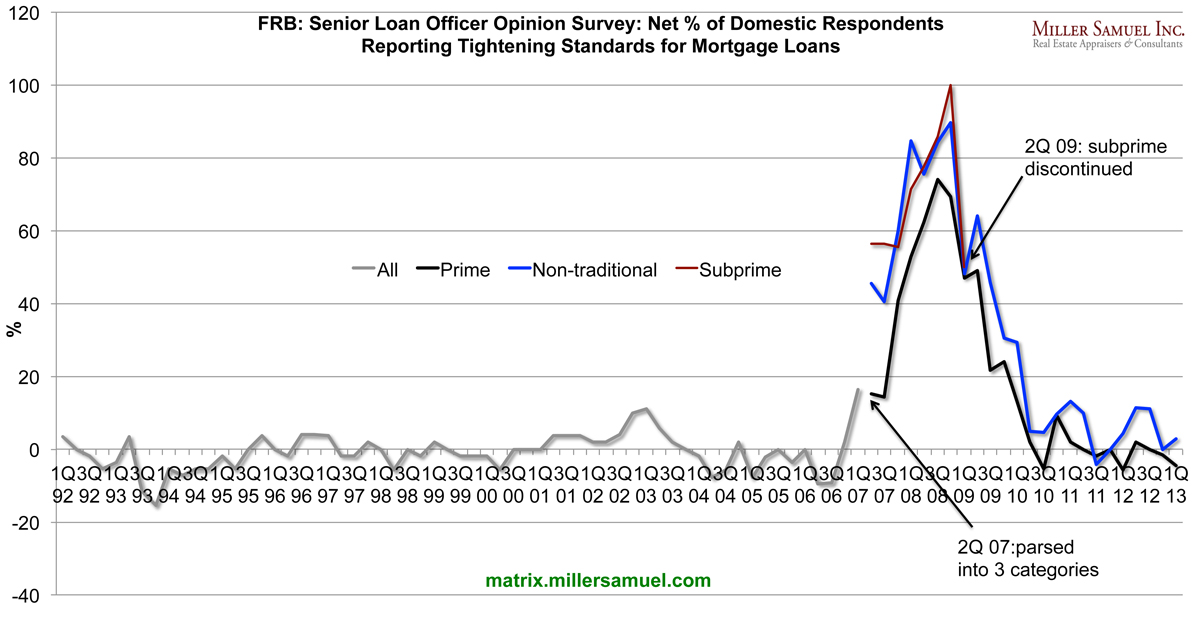

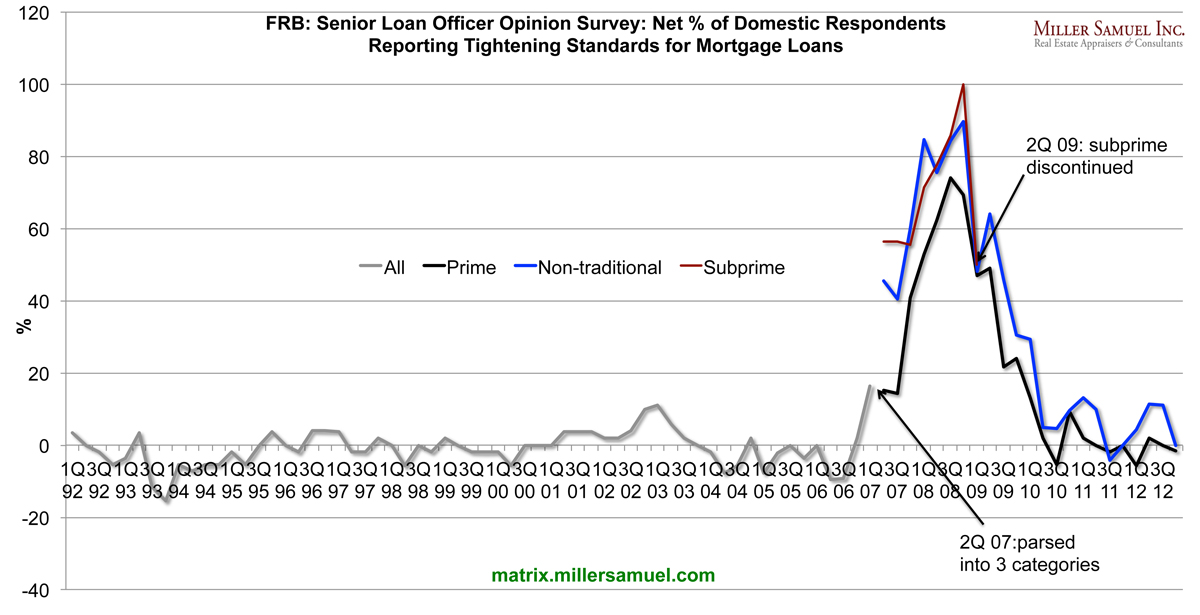

Federal Reserve: Mortgage Underwriting Standards Haven’t Eased

read more

1

2

Next

Load More Posts

Page load link

Go to Top