Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Backyard BBQ Talk

February 26, 2015

Affordability, Affordable Housing

,

Backyard BBQ Talk

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Manhattan

[Three Cents Worth #278 NY] Murray Hill Has the Most Micro Units in All of Manhattan

read more

February 24, 2015

Affordability, Affordable Housing

,

Backyard BBQ Talk

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Manhattan

[Three Cents Worth #277 NY] Which Manhattan Neighborhood Has The Smallest Studios?

read more

May 18, 2014

Affordability, Affordable Housing

,

Backyard BBQ Talk

,

Brooklyn

,

Credit, Finance, Mortgage, Rates

,

International

,

Luxury, Super, Ultra, Mega

,

Manhattan

Contrary To Popular Belief, The World Has Manhattan All Wrong

read more

May 17, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Manhattan

,

RealtyTrac

,

Statistics, Metrics & Data

Manhattan Home Sales Are NOT 80% All-Cash (They Are 45%)

read more

May 13, 2014

Backyard BBQ Talk

,

Books & Movies

,

Distressed Housing

,

Economy

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

[Vox Video] Housing Crash Fix Explained From Geithner’s Perspective

read more

April 28, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Housing Indices & Portals

,

Market Reports

PBS Newshour – Making Sense of Weak US Housing Reports

read more

April 1, 2014

Backyard BBQ Talk

,

Bloomberg News

,

Books & Movies

,

Manhattan

,

Time Out

My New Book “Flash Appraisals” Just Passed Michael Lewis

read more

March 3, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Manhattan

,

South Florida

,

Suburban, Urban, Commuting

Price per Square Inch for Pizza, Slices for Real Estate Market

read more

January 31, 2014

Backyard BBQ Talk

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

New York Times

,

Records, Thresholds and Outliers

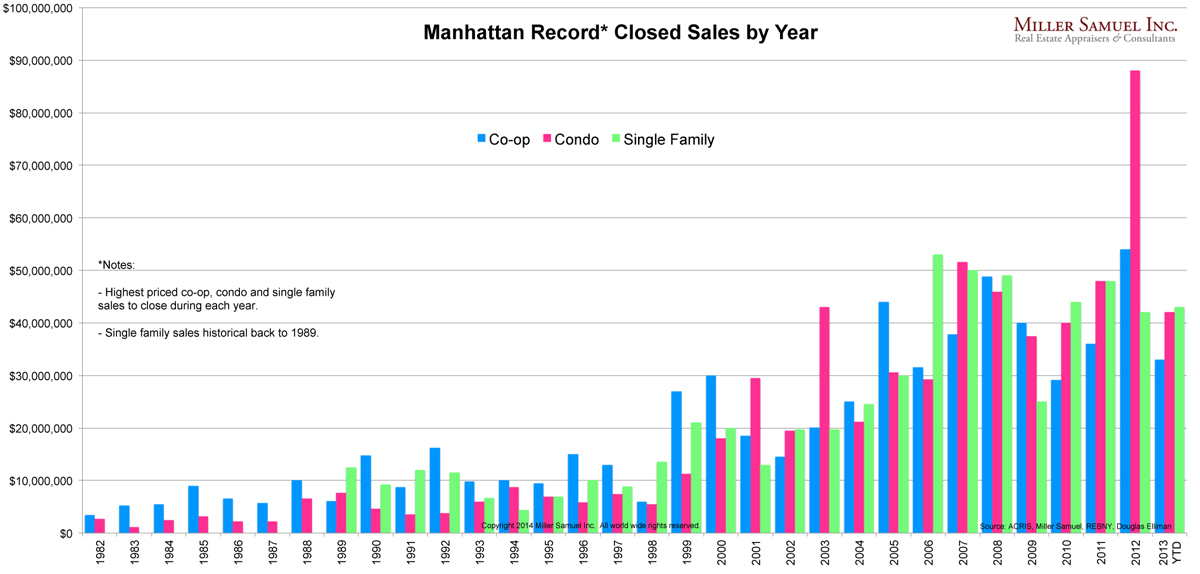

Manhattan Price Records from 1982 to 2013 (Will Soon Be Broken)

read more

May 17, 2009

Affordability, Affordable Housing

,

Backyard BBQ Talk

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Migration, Psychology, Demographics

,

New York Times

,

South Florida

[Promoting The Homeownership Cycle] Obsessive Housing Disorder

read more

Page load link

Go to Top