Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Brooklyn

August 20, 2021

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Fairfield County, CT

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

Queens

,

Westchester County, NY

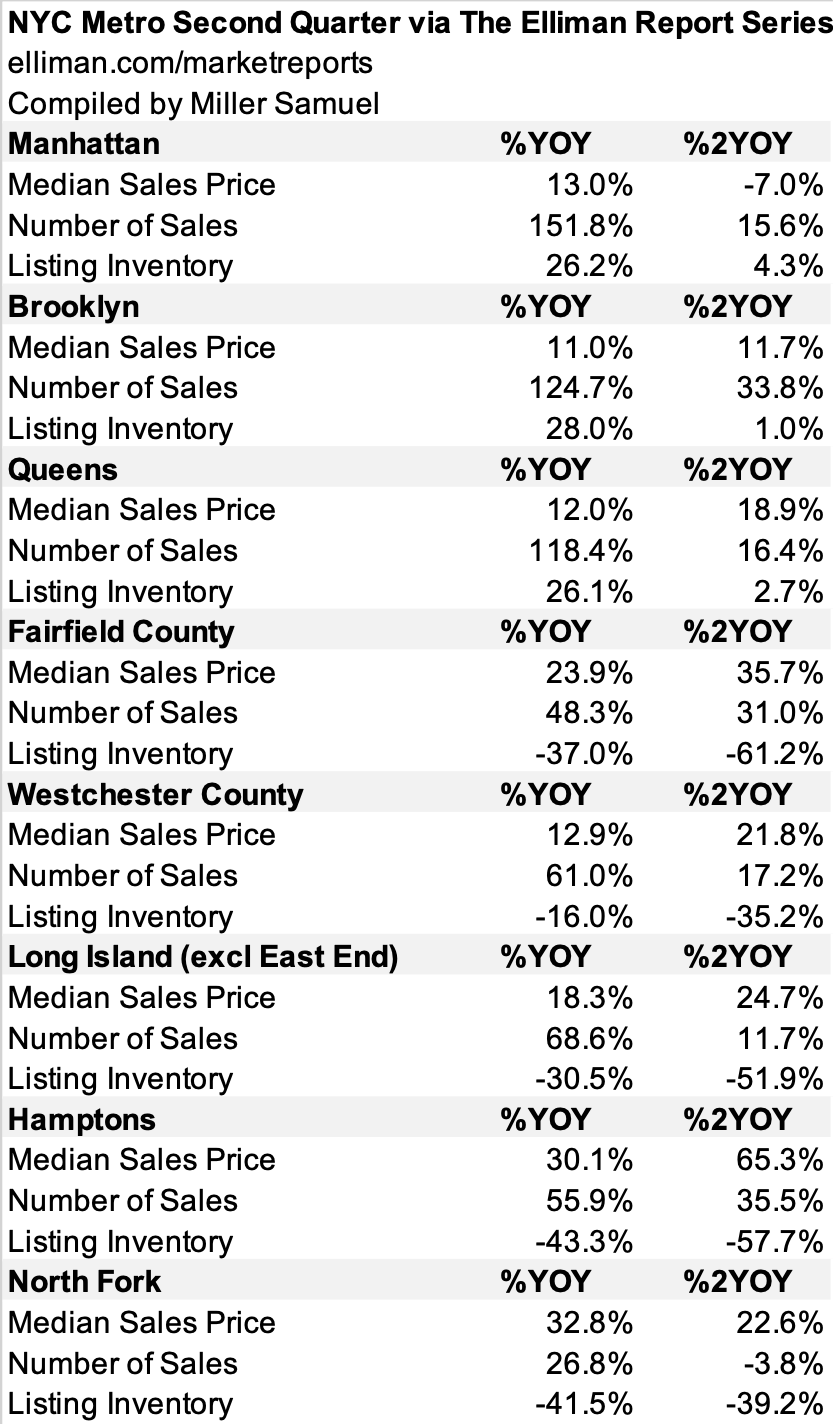

NYC Metro Conditions Much More Robust Than Two Years Ago

read more

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

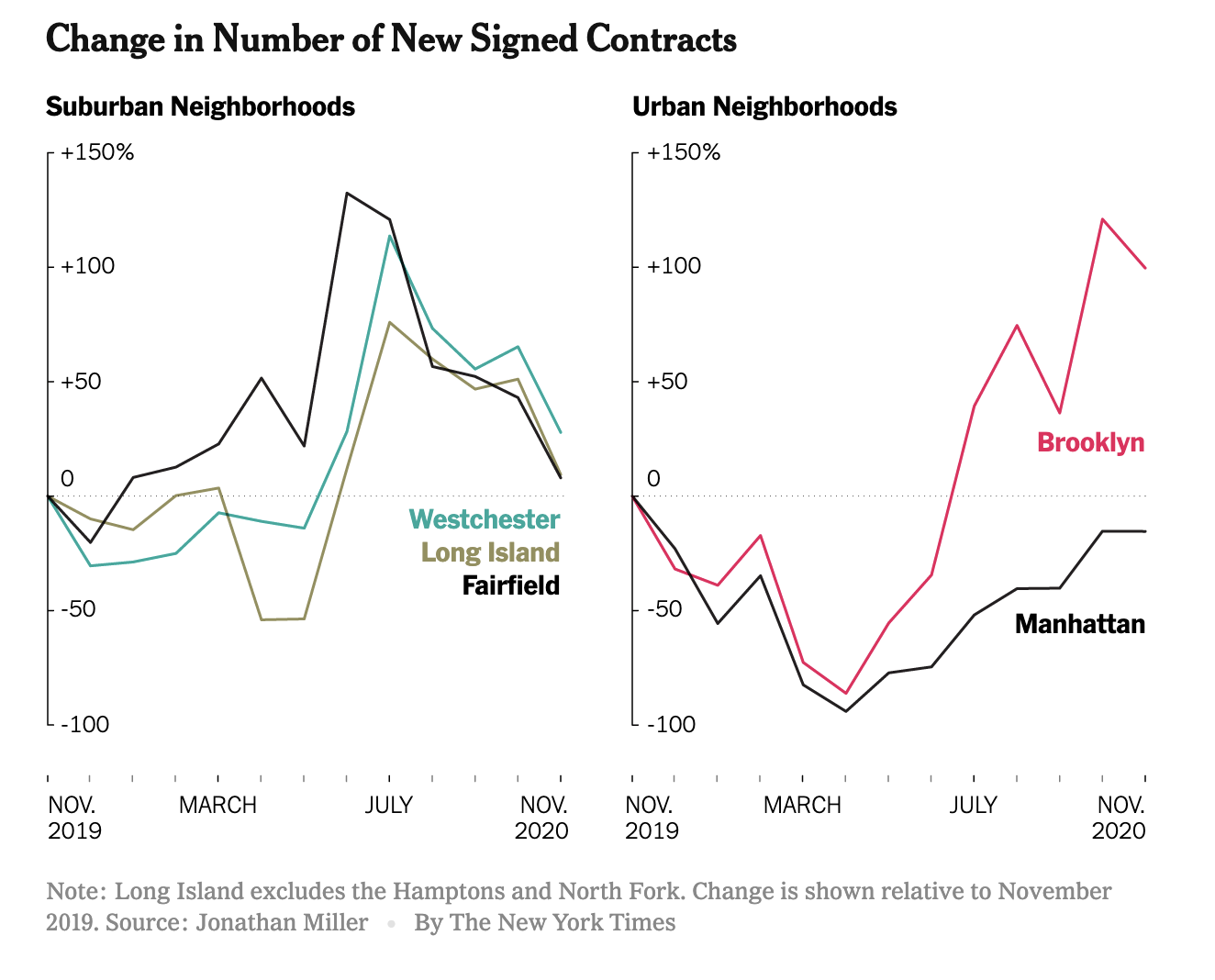

Peak Suburb Has Passed

read more

December 28, 2020

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

The Real Deal

,

Westchester County, NY

TRD Quick Question: Jonathan Miller “What’s Happening in the NYC Real Estate Market?”

read more

November 21, 2020

Brooklyn

,

Elliman Reports

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Queens

,

Rentals, Investing

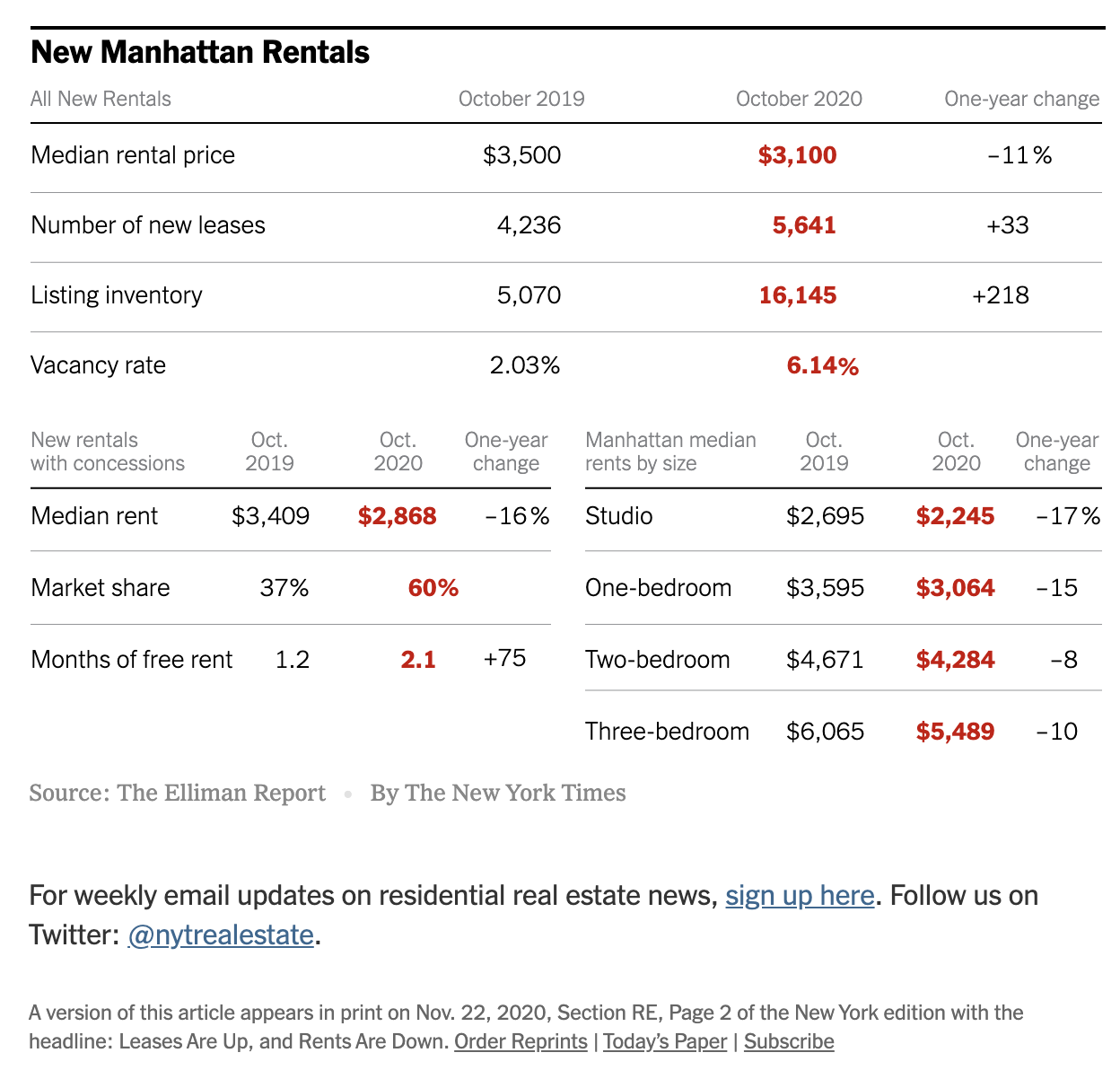

NYT Real Estate: Signs of a Manhattan Rental Market Recovery

read more

August 19, 2020

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Elliman Reports

,

Housing Note

,

Housing Trends & Cycles

,

Manhattan

,

New York Times

,

Westchester County, NY

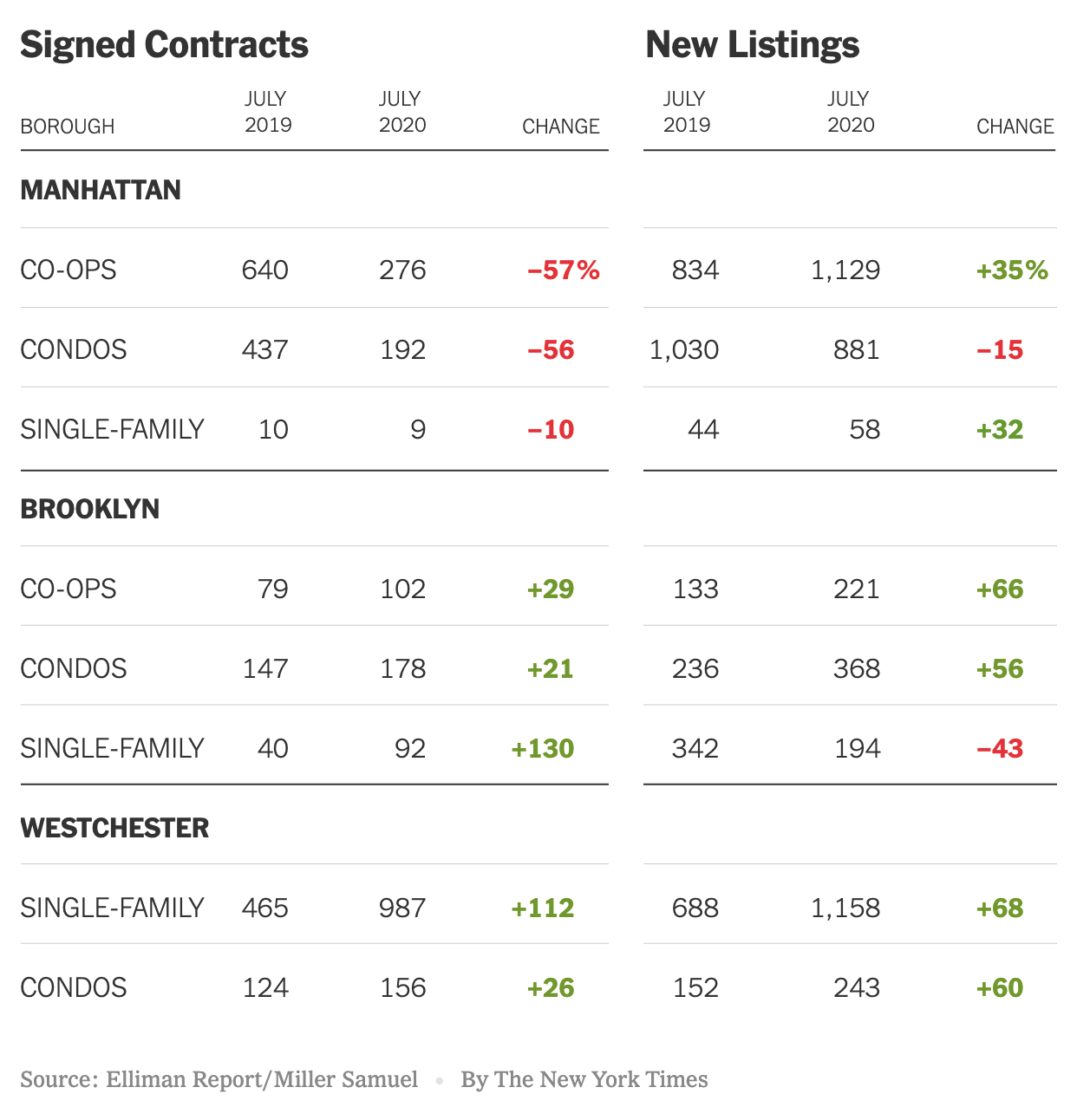

The ‘Urban To Suburban’ Narrative Is Really ‘Manhattan To Suburban’

read more

March 19, 2019

Affordability, Affordable Housing

,

Brooklyn

,

Government, Politics, Regulations & Policy

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Taxes, Insurance, Fees

The Proposed NYC “Pied-A-Terre Tax” Looks Catastrophic to NYC Real Estate

read more

December 14, 2018

Aspen

,

Boca Raton

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Greenwich

,

Manhattan

,

Statistics, Metrics & Data

Elliman Magazine Winter 2019 – Market Update

read more

September 7, 2018

Brooklyn

,

Fort Lauderdale

,

Greenwich

,

Los Angeles

,

Manhattan

Fall 2018 Elliman Magazine – Market Update

read more

April 15, 2018

Aspen

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Housing Trends & Cycles

,

Los Angeles

,

Manhattan

,

Palm Beach

Elliman Magazine Spring Edition – 5 Charts

read more

January 11, 2018

Analysis & Research

,

Bloomberg TV

,

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Interviews

,

Manhattan

,

Market Reports

,

Queens

,

Westchester County, NY

[Media] Bloomberg Markets Interview January 11, 2018

read more

December 11, 2016

Analysis & Research

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Palm Beach

John Burns Has It Wrong, Luxury Home Sales Are Not Increasing

read more

November 19, 2016

Brooklyn

,

Housing Trends & Cycles

,

Media

,

New York Times

,

Sales

,

Suburban, Urban, Commuting

,

Westchester County, NY

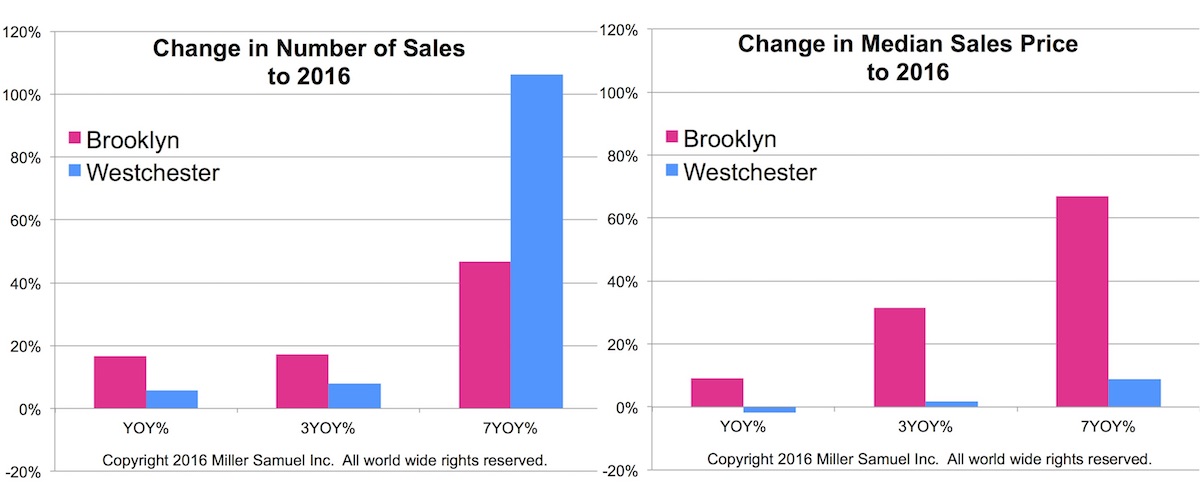

NYT Calculator: Suburban Sales Boom Measured By Houses on Monopoly Board

read more

1

2

Next

Load More Posts

Page load link

Go to Top