Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Taxes, Insurance, Fees

May 14, 2025

Adventures in Media & Marketing

,

Appraising

,

Blogosphere

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Elliman Reports

,

Government, Politics, Regulations & Policy

,

Public Speaking

,

Taxes, Insurance, Fees

[Podcast] Episode 4: What It Means With Jonathan Miller

read more

April 27, 2019

CNBC

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Luxury, Super, Ultra, Mega

,

Sales

,

Taxes, Insurance, Fees

,

Wall Street, Financial Services

CNBC TV 4-25-19 Coverage of Elliman Reports on Greenwich and Fairfield County, CT

read more

March 19, 2019

Affordability, Affordable Housing

,

Brooklyn

,

Government, Politics, Regulations & Policy

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Taxes, Insurance, Fees

The Proposed NYC “Pied-A-Terre Tax” Looks Catastrophic to NYC Real Estate

read more

January 2, 2018

Brick Underground

,

Explainer

,

Housing Trends & Cycles

,

Interviews

,

Media

,

Taxes, Insurance, Fees

[Media] Brick Underground Podcast January 2, 2018 – Jonathan Miller

read more

December 27, 2017

Bloomberg TV

,

Explainer

,

Media

,

Taxes, Insurance, Fees

Bloomberg TV – Housing Related Issues in Final Version of the Tax Cut and Jobs Act of 2017

read more

December 14, 2017

Media

,

Taxes, Insurance, Fees

NY1 TV, ‘Mornings On 1’ with Pat Kiernan

read more

March 31, 2014

Taxes, Insurance, Fees

,

Weather & Natural Disasters

Incentivized by FEMA, ‘Houses on Stilts’

read more

May 13, 2013

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

,

IRS

,

Taxes, Insurance, Fees

[No Fiscal Cliff Hangover] 1Q 2013 Hamptons & North Fork Reports

read more

January 29, 2013

Hamptons/North Fork

,

Taxes, Insurance, Fees

,

Wall Street Journal

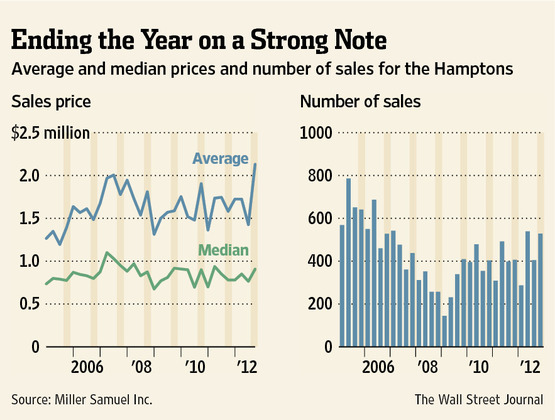

Hampton Year End Sales And Price Spike, Fiscal Cliff Style

read more

December 13, 2012

Taxes, Insurance, Fees

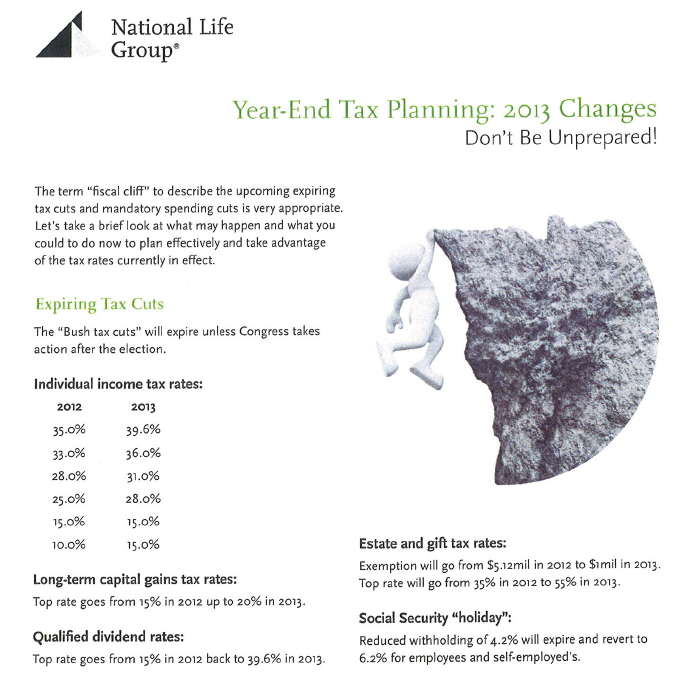

[Fiscal Cliff] Year End Tax Planning 2013

read more

November 25, 2012

Adventures in Media & Marketing

,

Government, Politics, Regulations & Policy

,

International

,

Manhattan

,

Taxes, Insurance, Fees

The Good Life Magazine – The French View of NYC

read more

November 6, 2012

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

,

Luxury, Super, Ultra, Mega

,

Taxes, Insurance, Fees

,

Weather & Natural Disasters

Hamptons High End Market in 4Q: Hedging Against Possible Rise in Capital Gains?

read more

1

2

Next

Load More Posts

Page load link

Go to Top