Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Historical, Landmark, Milestone

May 7, 2020

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

,

Weather & Natural Disasters

Manhattan Crisis: What Does Our Housing Past Tell Us About Our Housing Future?

read more

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

October 5, 2017

Bloomberg TV

,

Charts, Maps, Images, Infographics, Video

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

On Bloomberg TV: What’d You Miss? 10-5-2017

read more

September 11, 2017

Bloomberg Radio

,

Bloomberg TV

,

Historical, Landmark, Milestone

,

Manhattan

,

Media

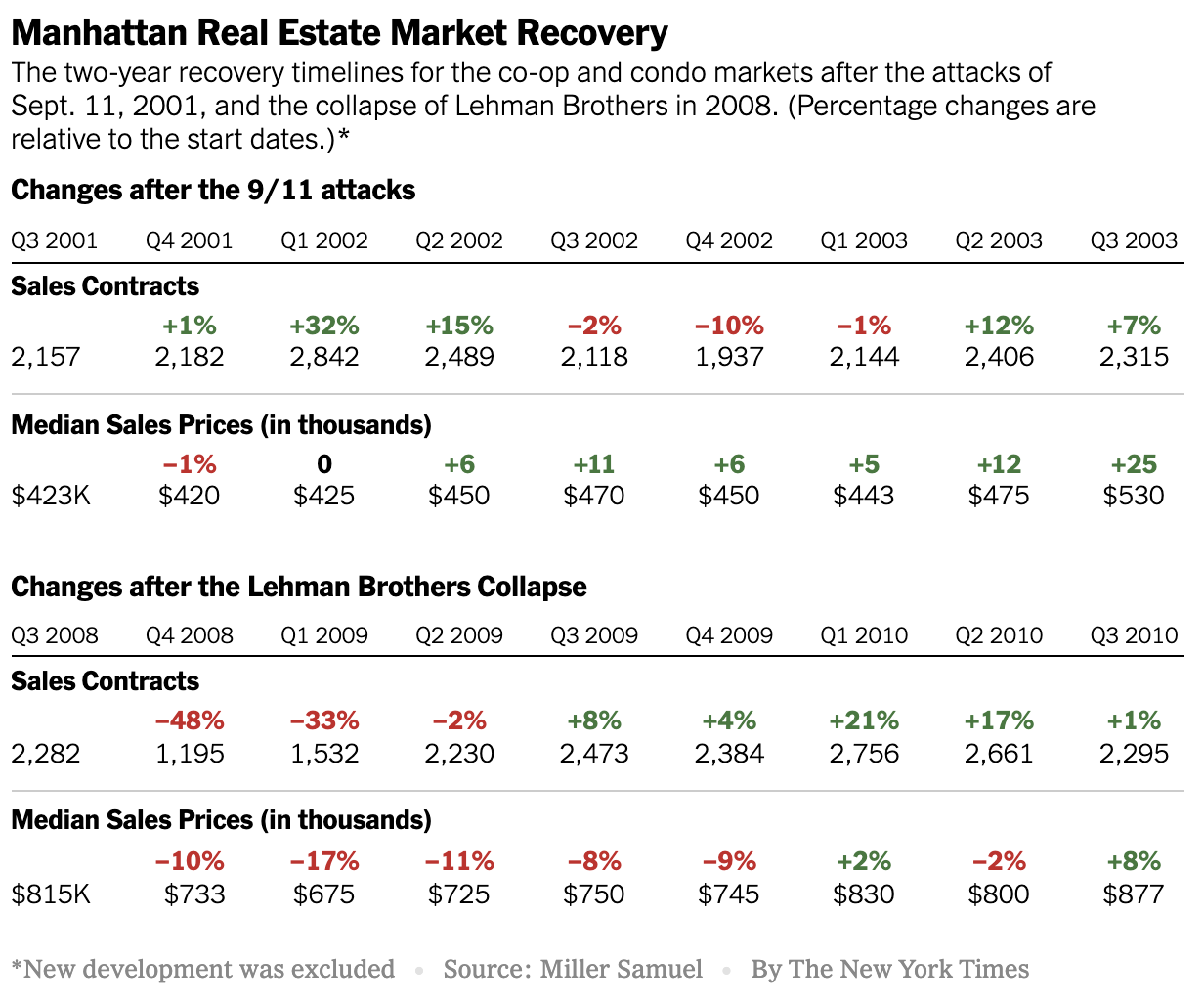

The NYC Downtown Resurgence After 9/11

read more

November 30, 2016

Charts, Maps, Images, Infographics, Video

,

Historical, Landmark, Milestone

,

Housing Indices & Portals

Declaring A Housing Recovery Using A Threshold Based on Fraud

read more

November 9, 2016

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

Housing and the Election Aftermath

read more

October 1, 2015

Appraising

,

Historical, Landmark, Milestone

,

Time Out

Miller Samuel turned 29 today

read more

June 3, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Douglas Elliman

,

Historical, Landmark, Milestone

,

Housing Trends & Cycles

,

Manhattan

,

Rentals, Investing

,

Sales

[Three Cents Worth #287 NY] Tracking New York Rents and Asking Prices Over a Century

read more

January 22, 2015

Blogging Off The Matrix

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Records, Thresholds and Outliers

,

Sales

[Three Cents Worth #276 NY] Proving New York’s Blockbuster $100M Sale Is An Outlier

read more

August 1, 2014

Amenities, Adjustments & Value Logic

,

Analysis & Research

,

Historical, Landmark, Milestone

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Times

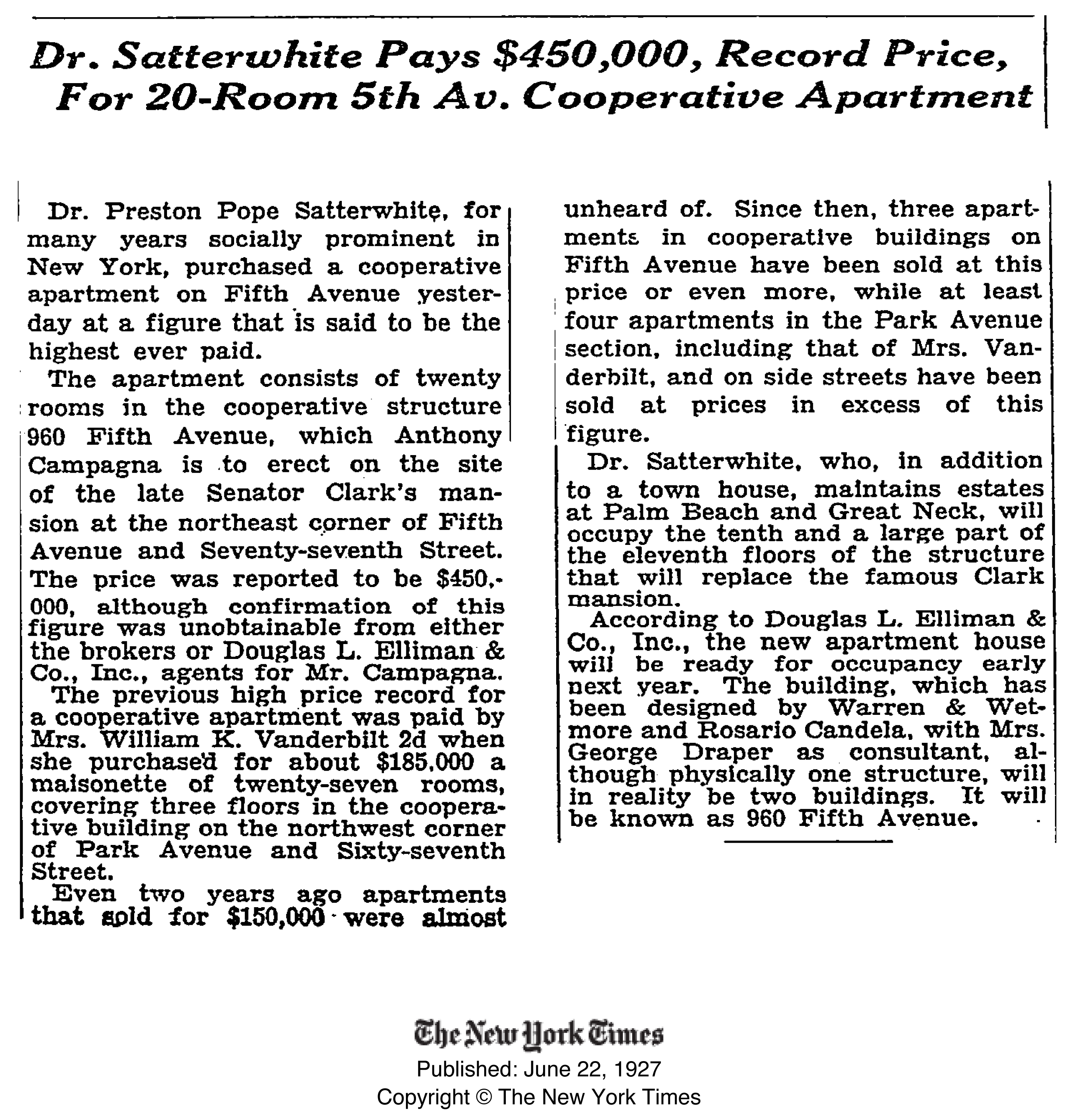

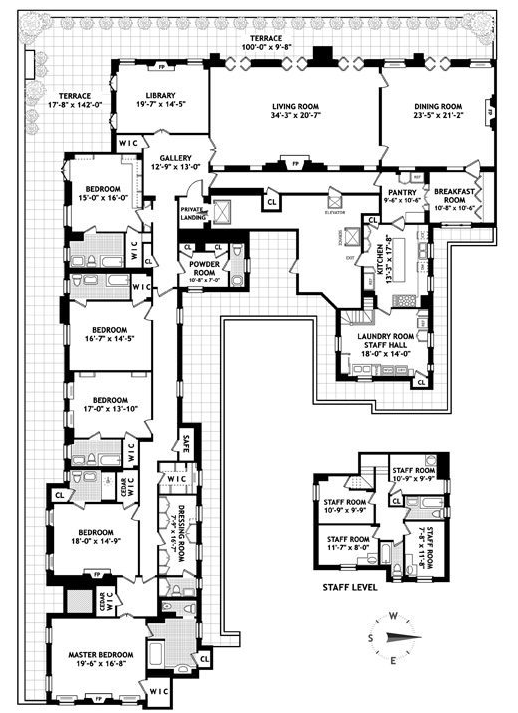

A Fifth Avenue Co-op’s 87-Year Price Increase was 3.6X Rate of Inflation

read more

June 9, 2014

Boards & Associations

,

Historical, Landmark, Milestone

,

Manhattan

,

Records, Thresholds and Outliers

Manhattan Penthouse Co-op Sold For 2nd Highest PPSF in History

read more

May 27, 2014

Historical, Landmark, Milestone

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

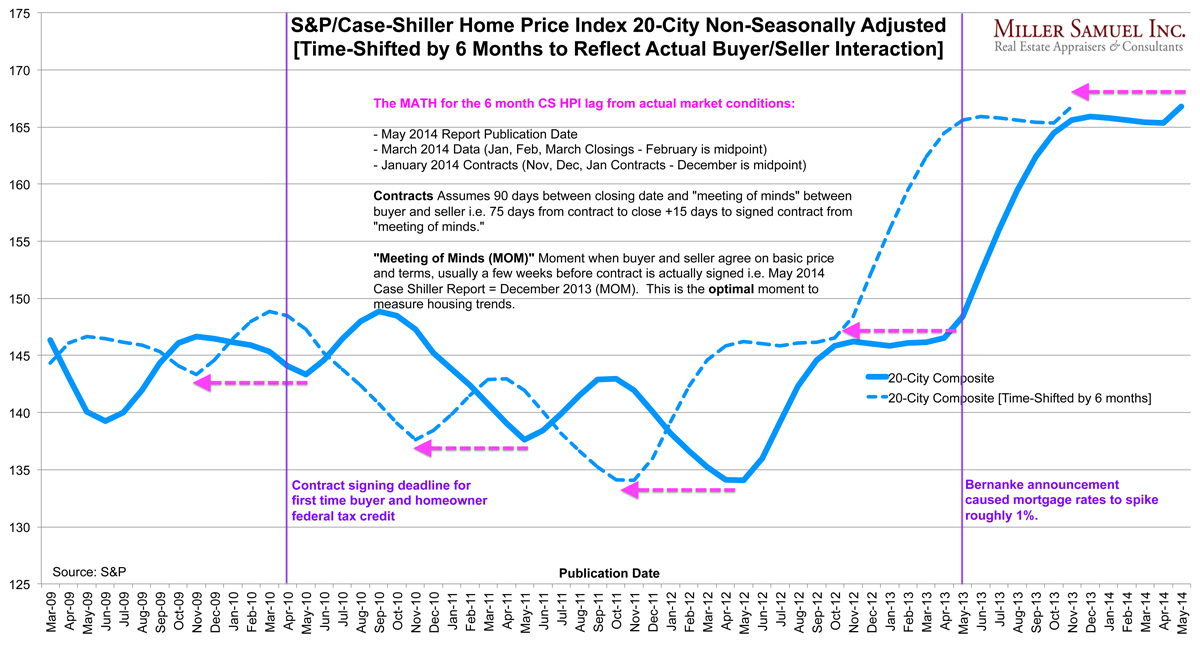

Pulling the Case-Shiller Index Back by 6 Months to Reflect Actual Buyer/Seller Behavior

read more

1

2

Next

Load More Posts

Page load link

Go to Top