Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Boards & Associations

June 18, 2021

Affordability, Affordable Housing

,

Boards & Associations

,

Suburban, Urban, Commuting

Don’t Miss the Unveiling of the 2021-22 Top Ten Issues Affecting Real Estate® 6-23

read more

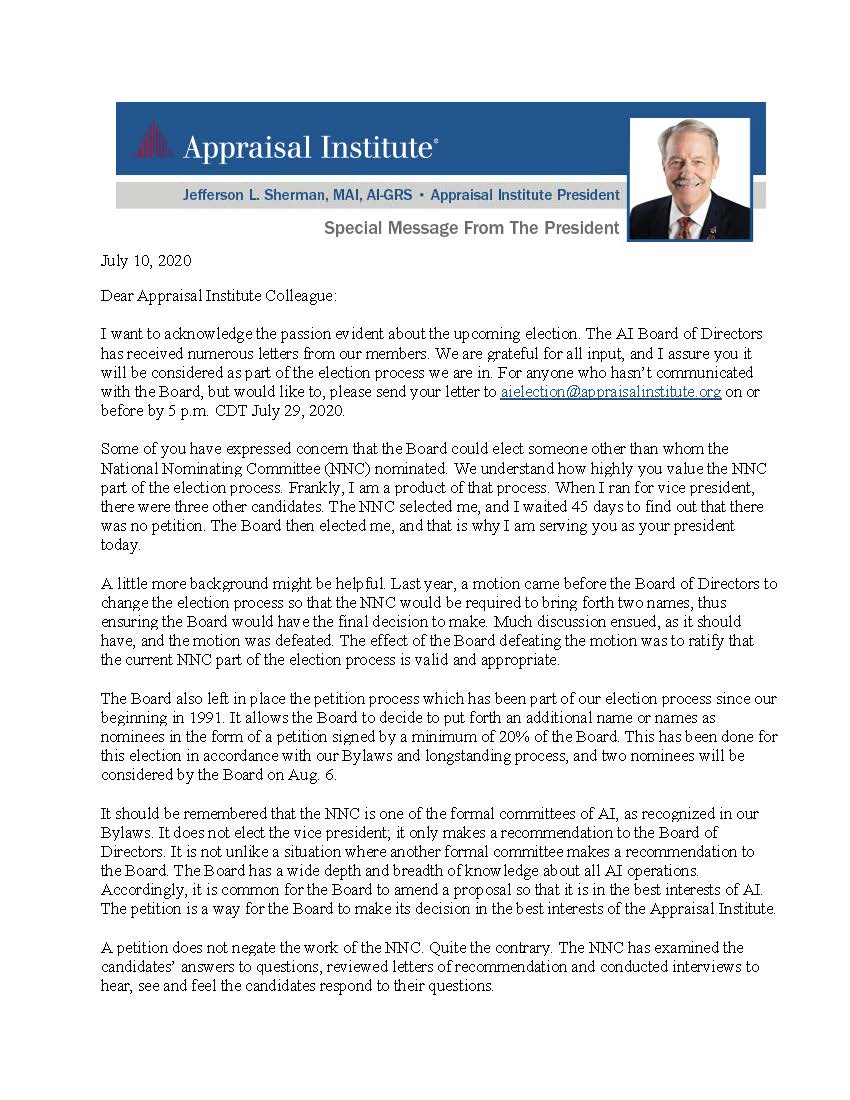

July 13, 2020

Appraising

,

Boards & Associations

,

Law, Ethics & Fraud

The Appraisal Institute Has Missed The Opportunity To Come Clean With Its Members

read more

December 14, 2016

Appraising

,

Boards & Associations

,

Government, Politics, Regulations & Policy

Incredibly, The Appraisal Institute is taking chapter “excess cash” and charging them for the privilege

read more

December 6, 2016

Appraising

,

Boards & Associations

,

Continuing Education & Licensing

,

Government, Politics, Regulations & Policy

Sadly, The Appraisal Institute is now working against its local chapters

read more

May 12, 2016

Amenities, Adjustments & Value Logic

,

Boards & Associations

,

Brokers, Agents, MLS, NAR

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

How Not to Value A Co-op Apartment: Price per Share

read more

June 9, 2014

Boards & Associations

,

Historical, Landmark, Milestone

,

Manhattan

,

Records, Thresholds and Outliers

Manhattan Penthouse Co-op Sold For 2nd Highest PPSF in History

read more

May 6, 2014

Appraising

,

Boards & Associations

,

Manhattan

,

Migration, Psychology, Demographics

,

New York City

,

Queens

Floored: Can/Should A Governing Body Set Minimum Sales Prices?

read more

Page load link

Go to Top