Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› New York Times

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

Peak Suburb Has Passed

read more

May 20, 2020

Housing Trends & Cycles

,

New York City

,

New York City Suburbs

,

New York Times

,

Public Speaking

NYT Real Estate Event May 21st @2:30 E.T. New York Real Estate: How Low Will Prices Go?

read more

May 7, 2020

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

,

Weather & Natural Disasters

Manhattan Crisis: What Does Our Housing Past Tell Us About Our Housing Future?

read more

November 25, 2016

Affordability, Affordable Housing

,

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

New York Times

,

Trulia

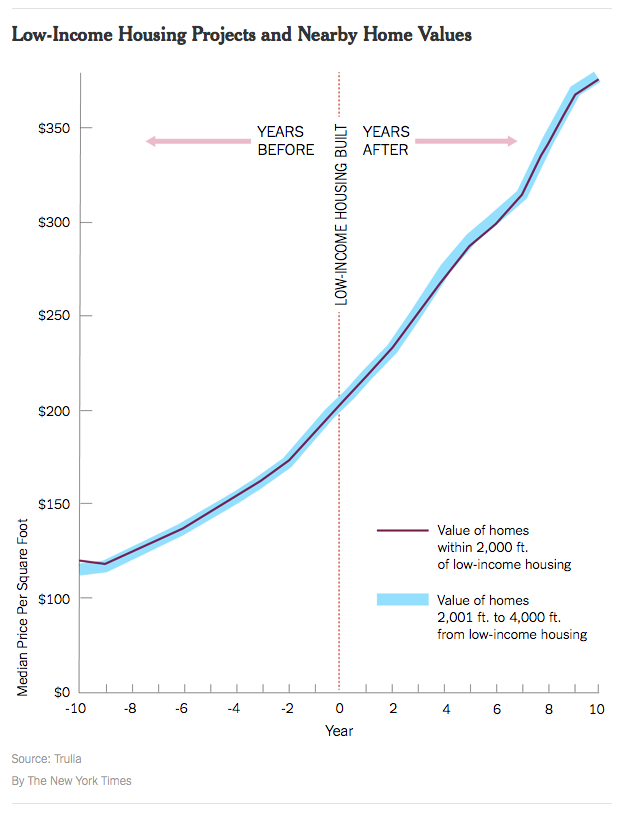

YIMBY: Low-Income Housing

read more

July 14, 2013

Boom Bubble Bust

,

Douglas Elliman

,

Manhattan

,

New York Times

Appearing on New York Times’ Page One NEVER Gets Old…But It’s A Process

read more

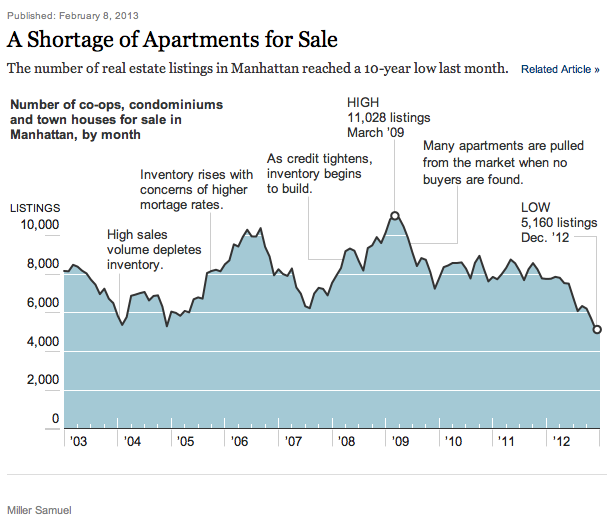

February 12, 2013

Manhattan

,

New York Times

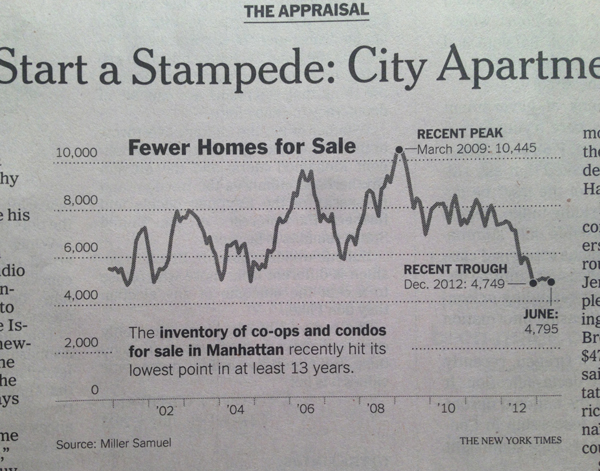

Listing Inventory Is, Well, Listing

read more

January 27, 2013

Adventures in Media & Marketing

,

Appraising

,

Brokers, Agents, MLS, NAR

,

New York Times

Broken Appraisal: Lack of Market Knowledge Overpowers Lack of Data

read more

January 13, 2013

Appraising

,

Credit, Finance, Mortgage, Rates

,

Homebuying Process

,

Media

,

New York Times

Having Fits With Appraisal In Home Buying Process

read more

December 26, 2012

Manhattan

,

New York Times

[NYT] Donut Housing Market Economics Rebranded As “Hard to Trade-up” Market

read more

September 1, 2012

International

,

Luxury, Super, Ultra, Mega

,

New York Times

[NYT Business Day Live] Luxury Real Estate As Art?

read more

August 8, 2012

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

,

New York Times

[On A1, 5 & Dime] New York Times Cover Story On Woolworth Condo Conversion

read more

July 23, 2012

Appraising

,

International

,

Media

,

New York Times

Why “Pull From Air” (P.F.A.) Is An Appraisal Term, Pig v. Sheep Explained

read more

1

2

Next

Load More Posts

Page load link

Go to Top