Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Economy

May 4, 2015

Affordability, Affordable Housing

,

Economy

,

Luxury, Super, Ultra, Mega

,

Migration, Psychology, Demographics

,

Rentals, Investing

,

Wall Street Journal

[Video] Why The Rich Get Richer

read more

January 30, 2015

Analysis & Research

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York City

,

Statistics, Metrics & Data

NYC Economy is Expanding Rapidly

read more

June 23, 2014

Affordability, Affordable Housing

,

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Wall Street Journal

Terrific Chart on Homeownership by Age

read more

June 16, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Economy

,

Federal Reserve, New York

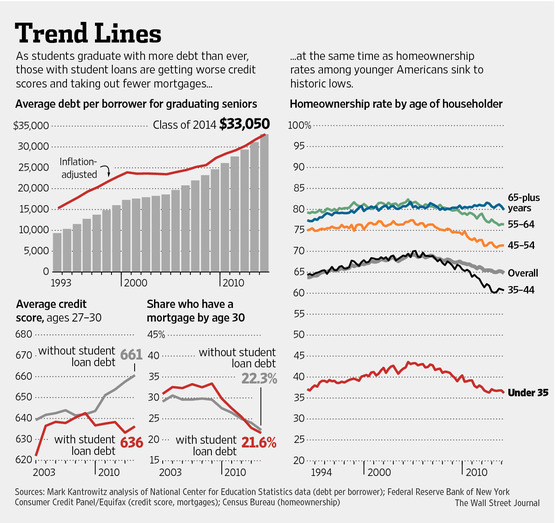

Housing is a Drag: US Student Debt Bubble Made Worse by the Baby Boomer Nanny State

read more

May 13, 2014

Backyard BBQ Talk

,

Books & Movies

,

Distressed Housing

,

Economy

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

[Vox Video] Housing Crash Fix Explained From Geithner’s Perspective

read more

May 10, 2014

Bloomberg News

,

Economy

,

Federal Reserve Bank

,

Housing Trends & Cycles

[Video] “Housing…will be a Necessary Casualty”

read more

March 27, 2014

Economy

,

International

,

Manhattan

,

Rentals, Investing

,

Wall Street Journal

,

Wall Street, Financial Services

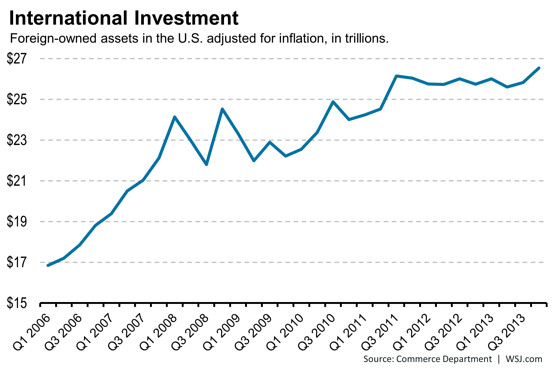

New Record of Foreign-owned Assets in the United States

read more

March 17, 2014

Analysis & Research

,

Economy

,

New York City

,

Wall Street, Financial Services

Bonus for NYC Housing: Wall Street Comp Up 15.1%, Most Cash Paid Out Since ’08 Crash

read more

August 20, 2013

Economy

,

Housing Indices & Portals

Housing Can’t “Recover” Until Fundamentals Recover

read more

July 1, 2013

Charts, Maps, Images, Infographics, Video

,

Economy

,

Wall Street Journal

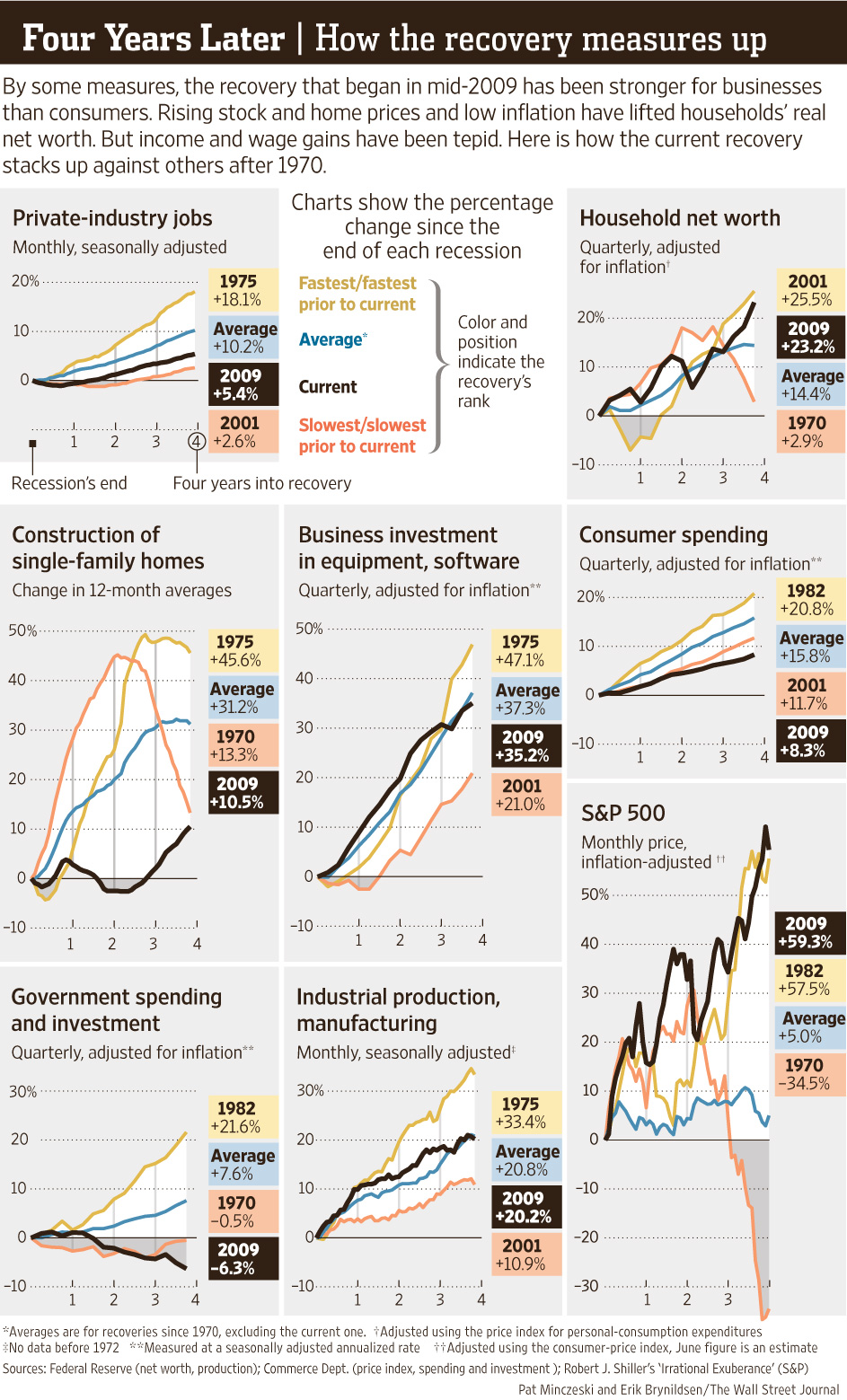

Cool WSJ Infographic on Economic Recovery Since End of Recession

read more

March 28, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

Money for Nothing Movie Trailer

read more

February 27, 2013

Bloomberg News

,

Curbed

,

Economy

,

Wall Street, Financial Services

Wall Streeters Paid 7X The Private Sector

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top