Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Economy

February 14, 2013

Celebrity, Pop Culture

,

Douglas Elliman

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

,

RealtyTrac

,

The Real Deal

Housing Data as Pop Culture

read more

January 28, 2013

Economy

,

Homebuying Process

,

Housing Indices & Portals

,

Language, Jargon & Quotes

,

New York Times

,

RealtyTrac

Falling Inventory Has Created a Housing “Pre-Covery,” not “Recovery”

read more

December 26, 2012

Economy

,

Government, Politics, Regulations & Policy

,

Homebuying Process

Yes, Mortgage Rates Impact Housing Prices

read more

September 23, 2012

Economy

,

The Housing Helix

,

Wall Street, Financial Services

[The Housing Helix Podcast] Barry Ritholtz Part 2

read more

September 23, 2012

Books & Movies

,

Economy

,

The Housing Helix

,

Wall Street, Financial Services

[The Housing Helix Podcast] Barry Ritholtz Part 1

read more

June 21, 2012

Economy

,

International

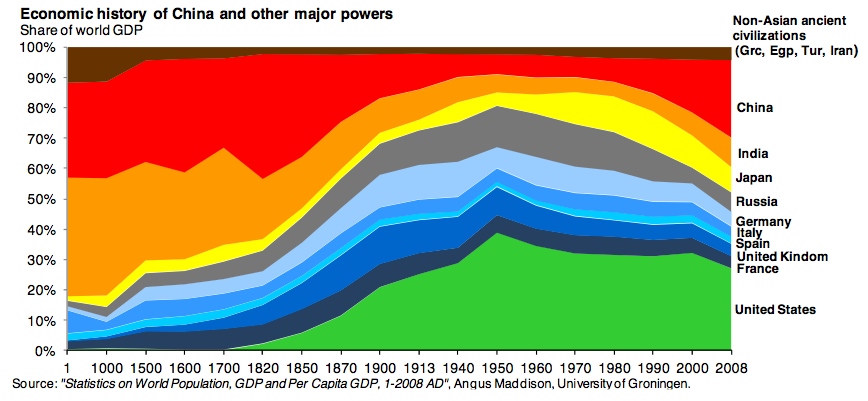

[The Atlantic] 2000 Years of Economic Power Measured by GDP

read more

May 21, 2012

Economy

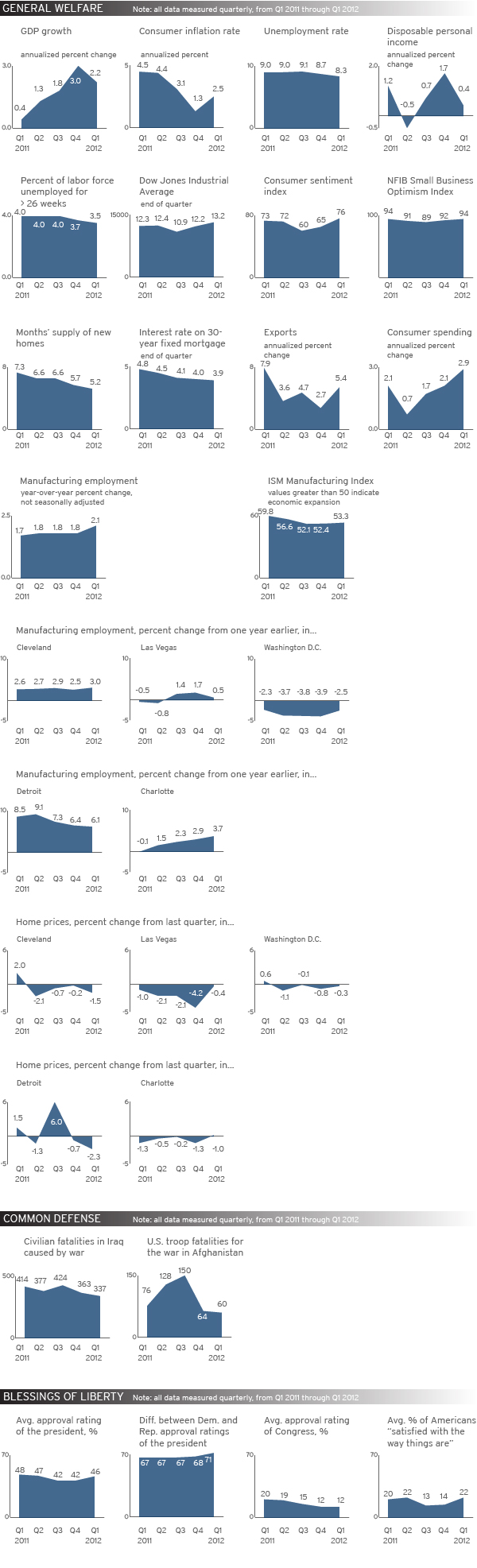

[Brookings] How We’re Doing Index – May 2012

read more

February 7, 2012

Boom Bubble Bust

,

Economy

,

New York Times

,

Wall Street, Financial Services

Buying Manhattan Apartments with Gold

read more

October 6, 2011

Books & Movies

,

Distressed Housing

,

Economy

,

Interviews

,

The Housing Helix

[Interview PART II] Barry Ritholtz, CEO, Director of Equity Research, Fusion IQ, Author, Bailout Nation, The Big Picture Blog

read more

October 5, 2011

Books & Movies

,

Economy

,

Interviews

,

The Housing Helix

[Interview PART I] Barry Ritholtz, CEO, Director of Equity Research, Fusion IQ, Author, Bailout Nation, The Big Picture Blog

read more

January 21, 2011

Books & Movies

,

Economy

,

Interviews

,

New York Times

,

The Housing Helix

[Interview] Barry Ritholtz, CEO, Director of Equity Research, Fusion IQ, Author, Bailout Nation, The Big Picture Blog

read more

December 21, 2010

Books & Movies

,

Economy

,

Interviews

,

The Housing Helix

[Interview] Mark Zandi, Chief Economist, Moody’s Analytics, Author, Financial Shock & Paying the Price

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top