Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Analysis & Research

June 15, 2017

Analysis & Research

,

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Media

[Forbes] Penthouse Juxtaposition – What Developer Wants v. What Market Supports

read more

March 26, 2017

Analysis & Research

,

Manhattan

Agricultural Land versus Manhattan Parking Per Acre

read more

December 11, 2016

Analysis & Research

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Palm Beach

John Burns Has It Wrong, Luxury Home Sales Are Not Increasing

read more

November 25, 2016

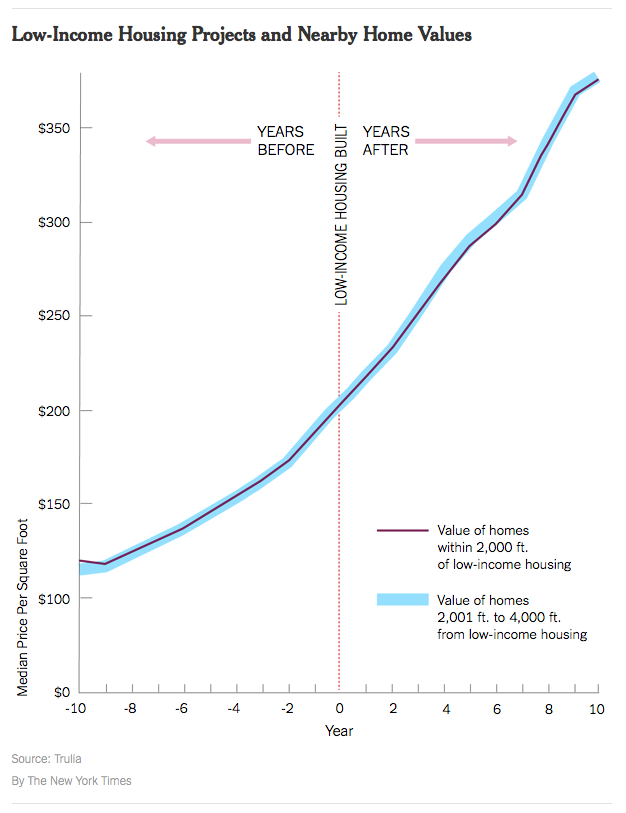

Affordability, Affordable Housing

,

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

New York Times

,

Trulia

YIMBY: Low-Income Housing

read more

March 7, 2016

Analysis & Research

,

Federal Reserve, New York

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Weather & Natural Disasters

New Yorkers Are Busy During Week So Big Snowstorms Need to Occur On Weekends

read more

September 22, 2015

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

Sales

Manhattan Monthly Absorption Rate – August 2015

read more

August 31, 2015

Analysis & Research

,

Aspen

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Luxury, Super, Ultra, Mega

[Three Cents Worth #291 Ski] Aspen Sales at $10 Million and Above Stay Consistent

read more

August 25, 2015

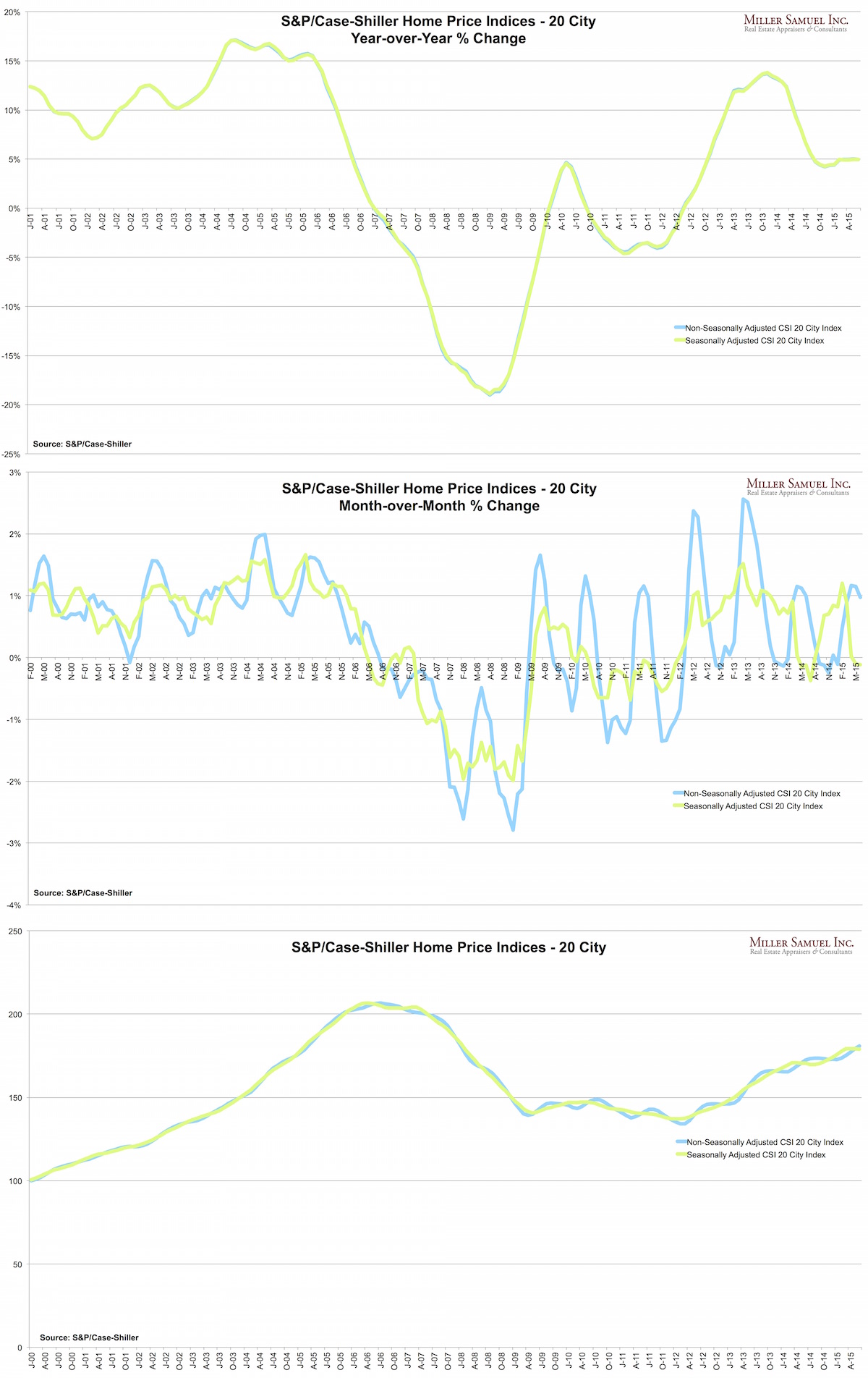

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

Explainer: Three Ways to Look at S&P/Case-Shiller Index Results

read more

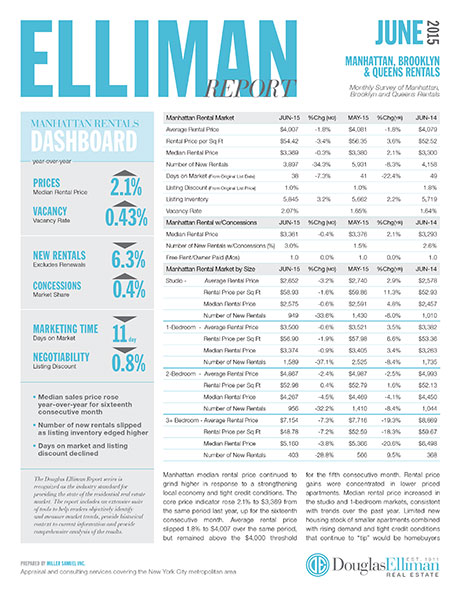

July 9, 2015

Analysis & Research

,

Bloomberg News

,

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Putnam County

,

Queens

,

Records, Thresholds and Outliers

,

Rentals, Investing

,

Sales

,

Westchester County, NY

Record Queens Condo Prices: Bigger Than Crises in Greece, China

read more

July 5, 2015

Analysis & Research

,

Elliman Reports

,

Housing Note

,

Manhattan

,

Records, Thresholds and Outliers

2Q 2015 Manhattan Sales Market Breaks A “Record Number of Records”

read more

January 30, 2015

Analysis & Research

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York City

,

Statistics, Metrics & Data

NYC Economy is Expanding Rapidly

read more

November 30, 2014

Analysis & Research

,

Bloomberg View

,

Housing Trends & Cycles

,

Los Angeles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Miami (Beach + Mainland)

,

Records, Thresholds and Outliers

Bloomberg View Column: The $10 Million Home, Never Hotter

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top