Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› StreetEasy

December 28, 2020

Bloomberg News

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Fairfield County, CT

,

Greenwich

,

Hamptons/North Fork

,

Housing Trends & Cycles

,

Long Island

,

Manhattan

,

New York Times

,

Rentals, Investing

,

Sales

,

Westchester County, NY

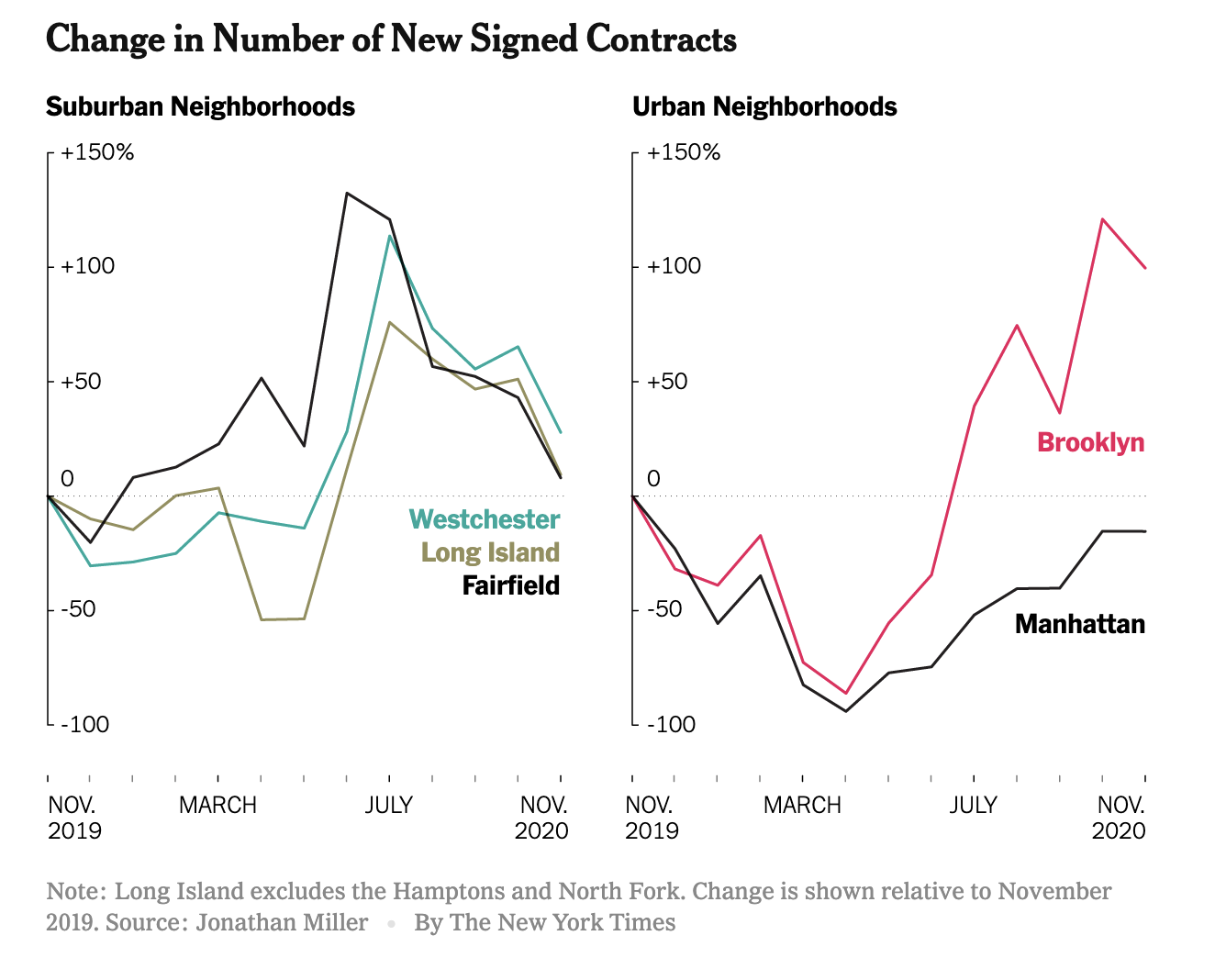

Peak Suburb Has Passed

read more

June 28, 2020

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

New York City

,

Op-Ed

My Forbes Column: Keeping Housing Market Results From The Public Is Never Justified: An Expansive View

read more

May 4, 2019

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Post

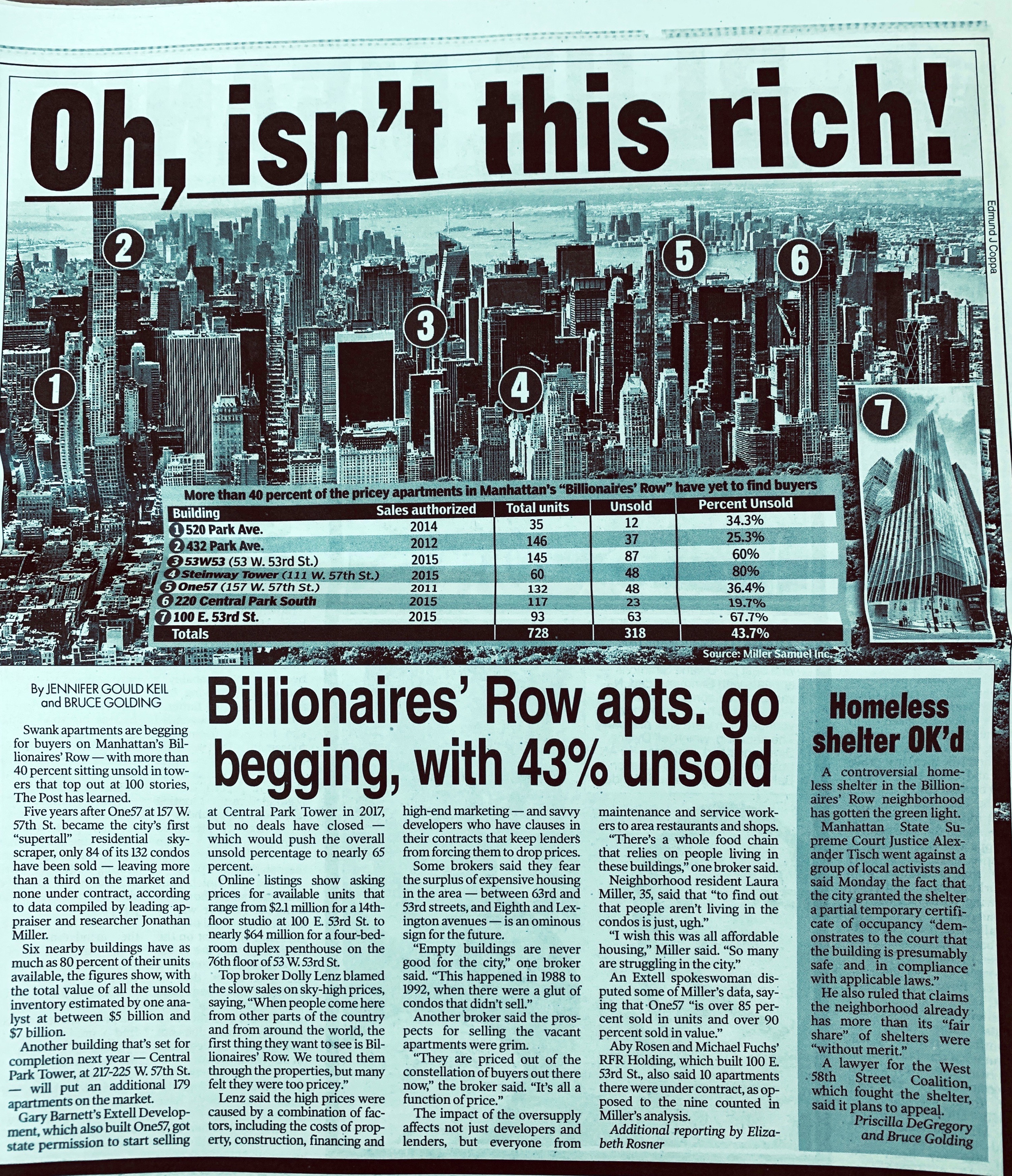

Billionaires Row Continues to be Challenged

read more

August 19, 2013

Analysis & Research

,

Bloomberg News

Zillow Acquires StreetEasy, Goes Vertical, Literally

read more

June 11, 2010

IRS

,

Manhattan

,

New York Times

[Spring Market] In Like a Lion, Out Like a Lamb

read more

Page load link

Go to Top