Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› New York Observer

July 30, 2015

Appraising

,

Media

,

Time Out

An Honest Appraisal – Some Personal Background Including My Favorite Color and Love of Yo-Yos

read more

February 14, 2013

Housing Indices & Portals

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

The Real Deal

Manhattan Diverged From NYC At US Housing Boom Peak

read more

December 27, 2012

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

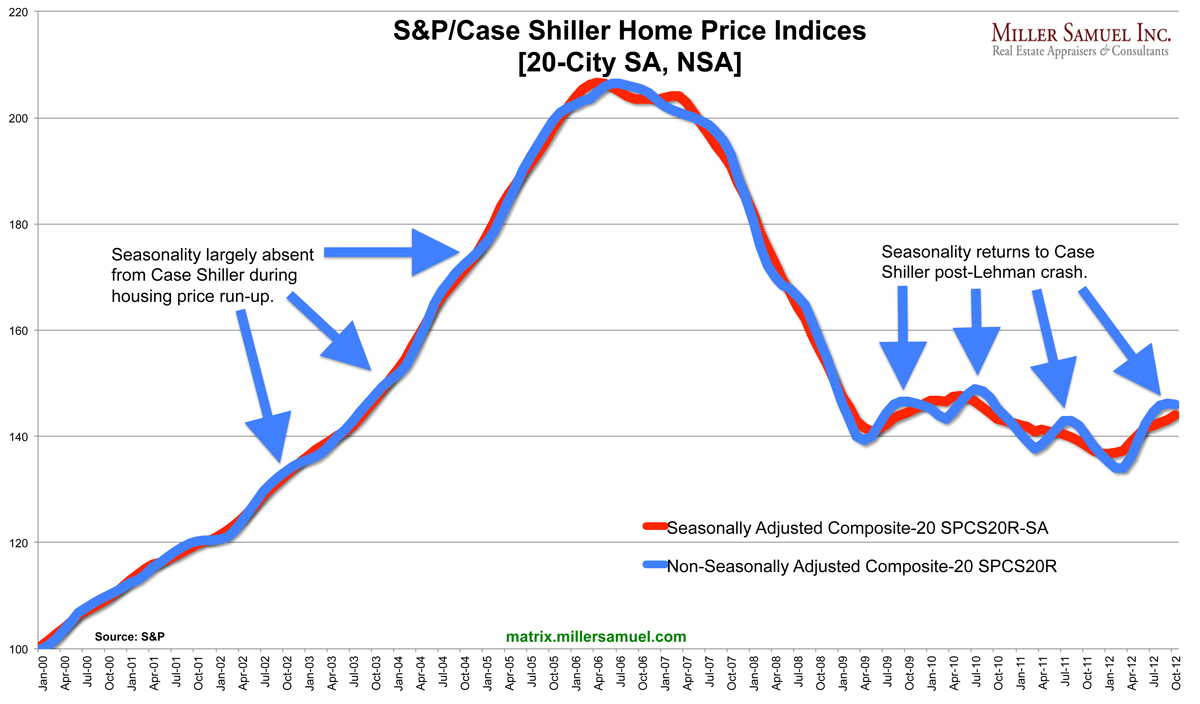

[Case Shiller] Recovery Is Back In Season

read more

November 20, 2009

Commercial, Retail

,

The Housing Helix

[The Housing Helix Podcast] Robert Knakal, Chairman, Founding Partner, Massey Knakal Realty Services

read more

November 20, 2009

Brokers, Agents, MLS, NAR

,

Commercial, Retail

,

Interviews

,

The Housing Helix

[Interview] Robert Knakal, Chairman, Founding Partner, Massey Knakal Realty Services

read more

October 26, 2009

Amenities, Adjustments & Value Logic

,

Distressed Housing

,

Humor or Whimsy

,

New York Magazine

[Central Park v. Detroit] $363,538,692,000 v. $4,500,000

read more

June 3, 2009

Adventures in Media & Marketing

,

Humor or Whimsy

,

Media

[86’d] Up A Notch In Power Poll

read more

May 14, 2009

Bloomberg News

,

Douglas Elliman

,

Media

,

Public Speaking

[Public] Tonight’s Observer Living Real Estate/Tomorrow AM Bloomberg Surveillance

read more

March 9, 2009

Economy

,

New York Times

[Why It’s Not Just About Price] The $39 Dollar Suit Story

read more

January 14, 2009

Bloomberg News

,

Brooklyn

,

Crain's New York Business

,

Curbed

,

Douglas Elliman

,

Elliman Reports

,

Market Reports

,

The Real Deal

[When Brooklyn Was The World] 4Q 2008 Brooklyn Market Overview Available For Download

read more

January 13, 2009

Crain's New York Business

,

Inman News

,

Law, Ethics & Fraud

,

Migration, Psychology, Demographics

Editorializing The Real Estate Hype

read more

January 13, 2009

Blogosphere

,

Curbed

,

Douglas Elliman

,

Housing Indices & Portals

,

Manhattan

,

New York Times

,

Wall Street Journal

[Solid Puff Piece] Goldman Research Note Clouds Manhattan

read more

1

2

Next

Load More Posts

Page load link

Go to Top