Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Lehman

March 23, 2014

Bloomberg News

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Wall Street, Financial Services

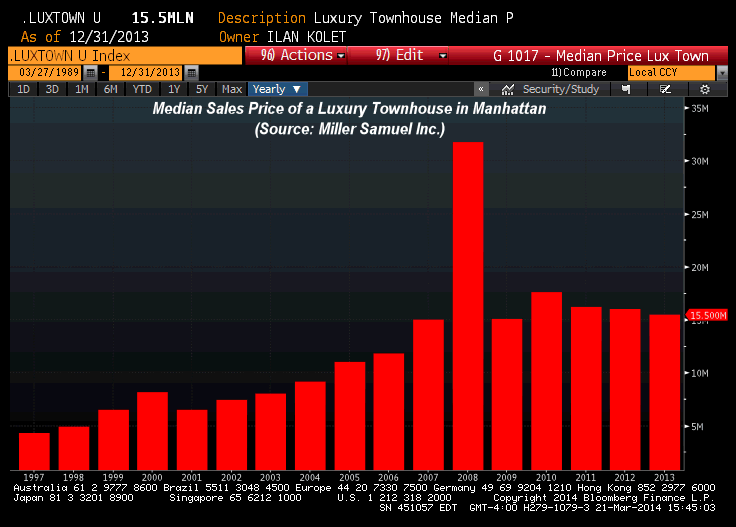

Spot the Manhattan Luxury Townhouse Lehman Effect?

read more

October 4, 2013

Douglas Elliman

,

Elliman Reports

,

Manhattan

[Long List of Records] 3Q 2013 Manhattan Sales Report

read more

September 16, 2013

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

New York Times

,

Wall Street Journal

The Low Appraisal “Hassle” is a Symptom of a Broken Mortgage Process

read more

September 13, 2013

Charts, Maps, Images, Infographics, Video

,

International

,

Knight Frank

,

Wall Street, Financial Services

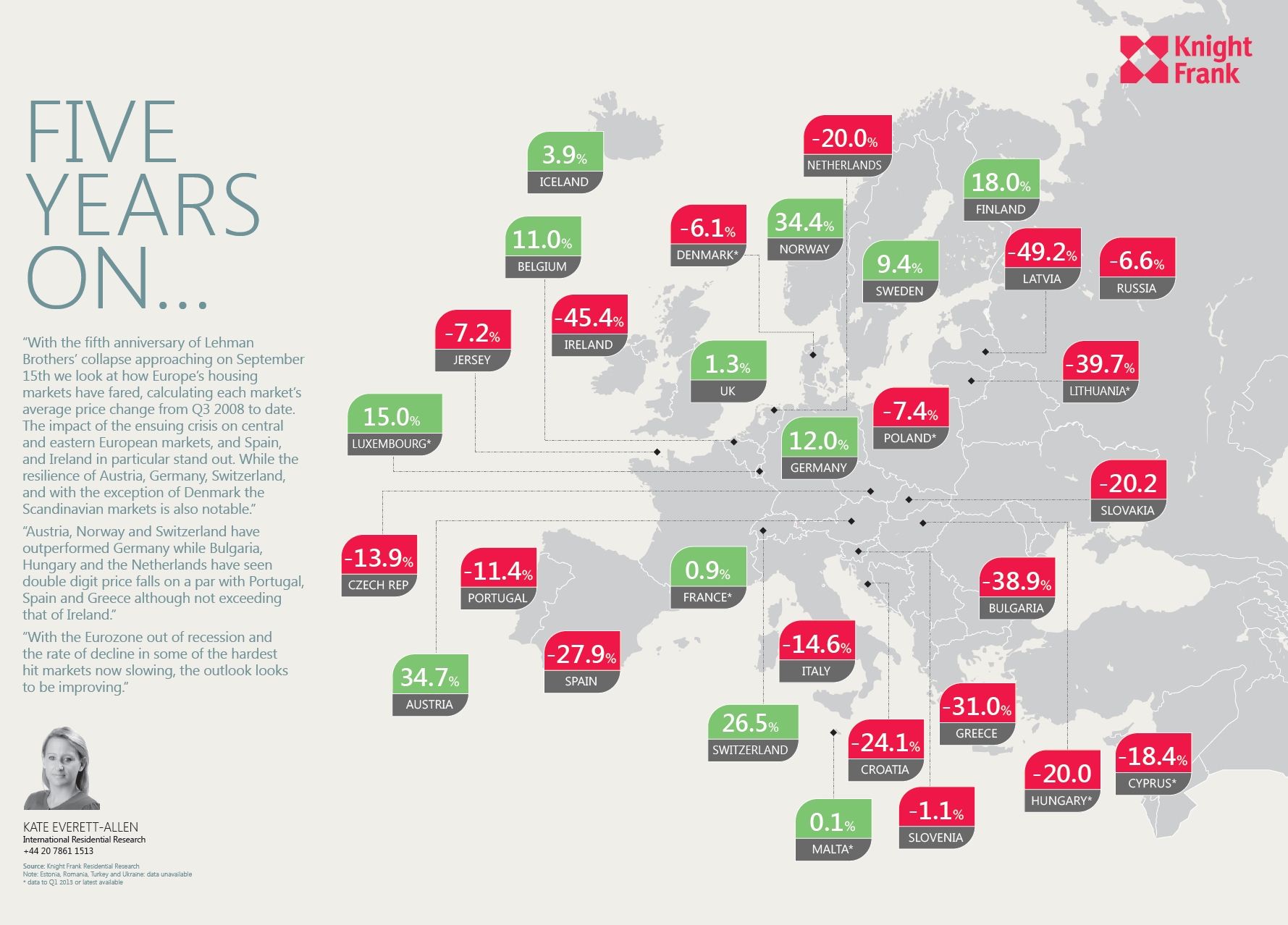

Impact of Lehman Collapse on Housing Prices in Europe

read more

September 3, 2013

Blogging Off The Matrix

,

Curbed

,

Manhattan

[Three Cents Worth #245 NY] Manhattan Puts Best (Square) Foot Forward

read more

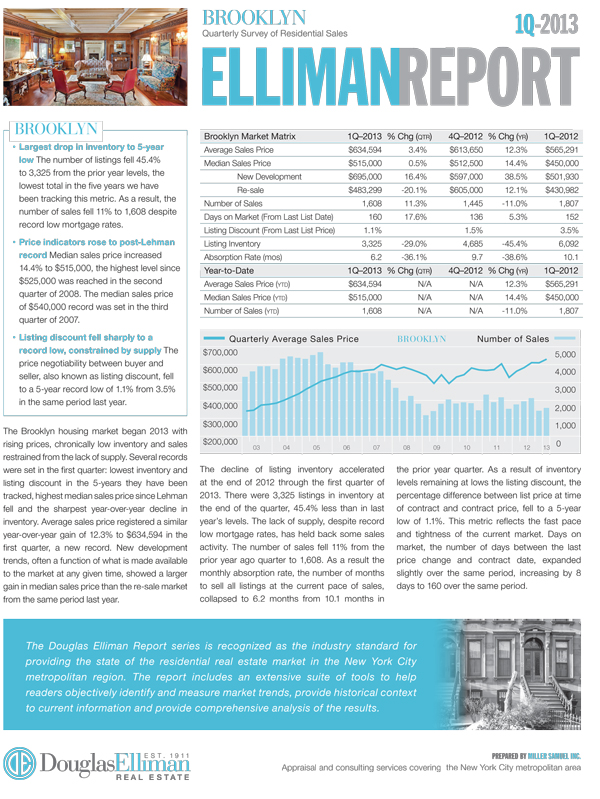

April 11, 2013

Brooklyn

,

Douglas Elliman

,

Elliman Reports

[Tight] 1Q 2013 Brooklyn Report

read more

February 6, 2013

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York Times

Tight Credit Is Causing Housing Prices to Rise

read more

January 31, 2013

Douglas Elliman

,

Elliman Reports

,

Manhattan

[60 Pages of Data Bliss] 2003-2012 Manhattan Decade Report

read more

November 20, 2012

Blogging Off The Matrix

,

Curbed

[Three Cents Worth NY #218] Manhattan’s Thanksgiving Listing Spread

read more

November 18, 2012

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Canada

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

International

,

Knight Frank

,

Luxury, Super, Ultra, Mega

,

Manhattan

Luxury Real Estate as the New Global Currency

read more

November 6, 2012

Douglas Elliman

,

Elliman Reports

,

Hamptons/North Fork

,

Luxury, Super, Ultra, Mega

,

Taxes, Insurance, Fees

,

Weather & Natural Disasters

Hamptons High End Market in 4Q: Hedging Against Possible Rise in Capital Gains?

read more

October 20, 2012

Brooklyn

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Rentals, Investing

[New, Improved, Expanded] 9-2012 Manhattan/Brooklyn Rental Report

read more

1

2

Next

Load More Posts

Page load link

Go to Top