Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Charts

August 31, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

Bloomberg View Column: Understanding Housing’s Dog Days

read more

August 31, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Crime, Protests, Social-Unrest

,

Housing Indices & Portals

,

Migration, Psychology, Demographics

,

Weather & Natural Disasters

Bloomberg View Column: The Myth of Real Estate Stigma

read more

August 5, 2014

Blogging Off The Matrix

,

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York City

,

Queens

,

Records, Thresholds and Outliers

[Three Cents Worth #267 NY] NYC Sets New Record Average Sales Price

read more

July 31, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Housing Indices & Portals

My Bloomberg View Column: Housing Data Is Old and Moldy

read more

July 28, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Brokers, Agents, MLS, NAR

,

Op-Ed

,

Trulia

,

Wall Street, Financial Services

,

Washington DC

My First Post on Bloomberg View: Homebuying Gets a Housecleaning

read more

July 14, 2014

Charts, Maps, Images, Infographics, Video

,

Manhattan

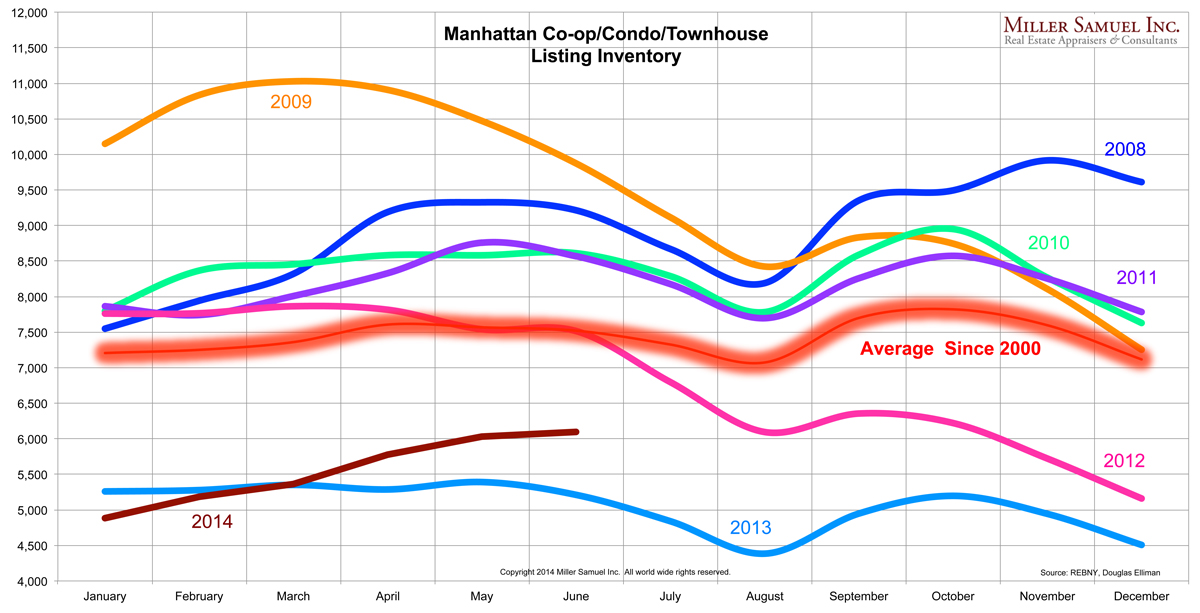

Manhattan Inventory: This is what I mean by rising, but not enough

read more

July 1, 2014

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Sales

2Q14 Manhattan Sales Market: More Supply, But Not Even Close to Enough

read more

July 1, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

Manhattan

Rocket Ship: Manhattan New versus Existing Average Sales Price

read more

June 24, 2014

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

,

Housing Trends & Cycles

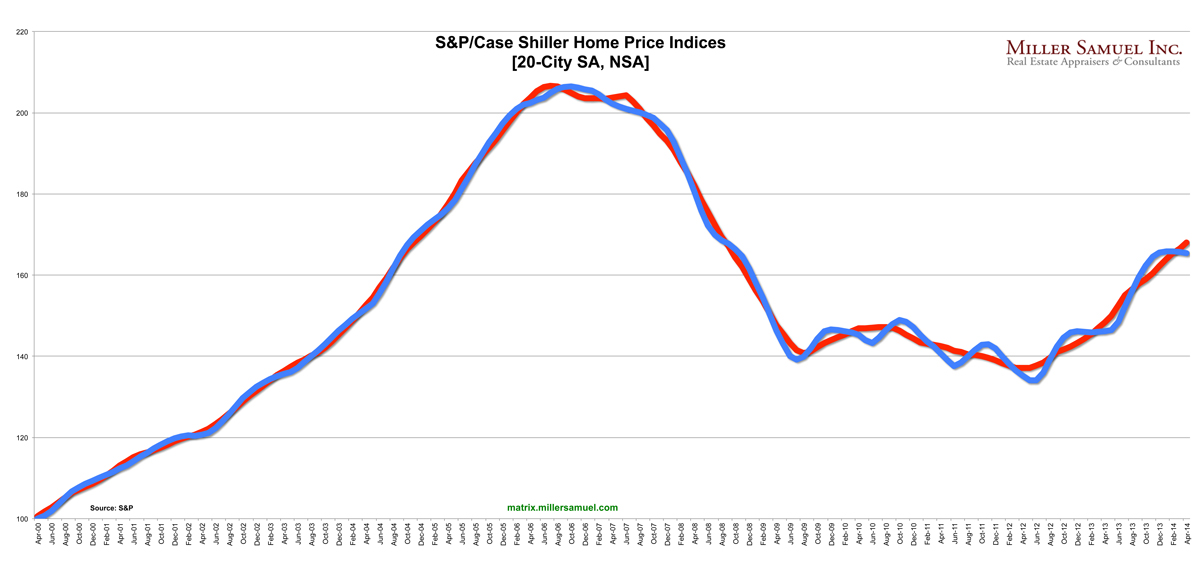

Time-Shifted Case Shiller: Dallas, Denver Crushing it, Polar Vortex a Non-Issue ‘Cause It’s Still December

read more

June 23, 2014

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

NAR May 2014 Existing Home Sales: ‘Heat-up’

read more

June 20, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Douglas Elliman

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Sales

Manhattan New Development: Small Share, But Rising Sharply

read more

June 12, 2014

Brooklyn

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Housing Trends & Cycles

,

Manhattan

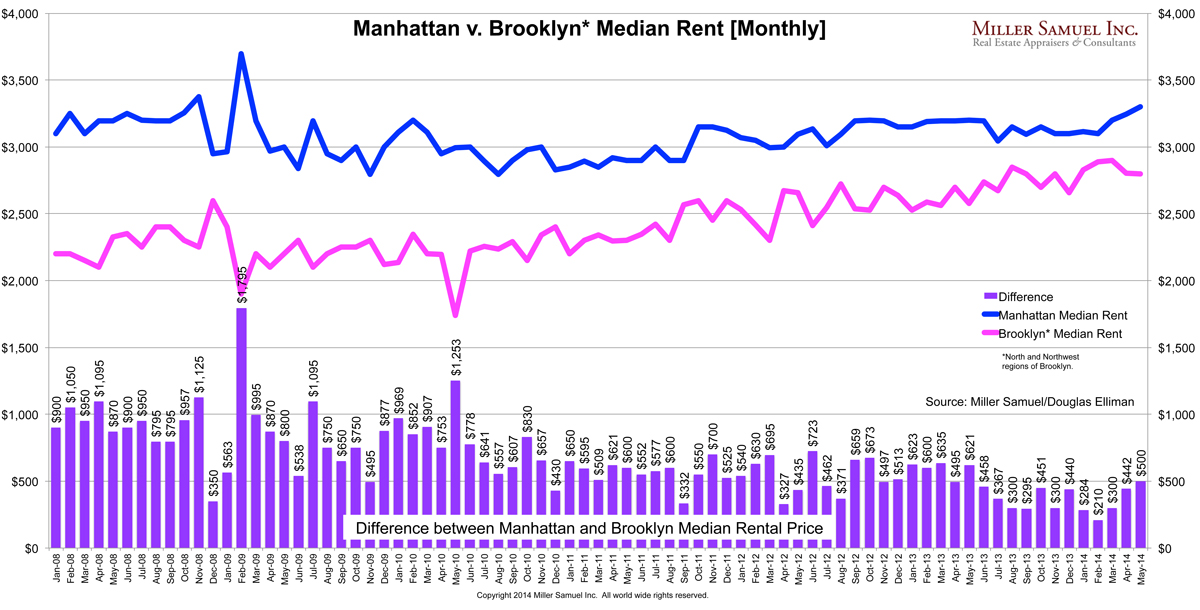

Manhattan-Brooklyn Rental Price Spread Widens to $500

read more

Previous

6

7

8

Next

Load More Posts

Page load link

Go to Top