Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Charts

June 9, 2014

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Housing Trends & Cycles

,

Op-Ed

,

Statistics, Metrics & Data

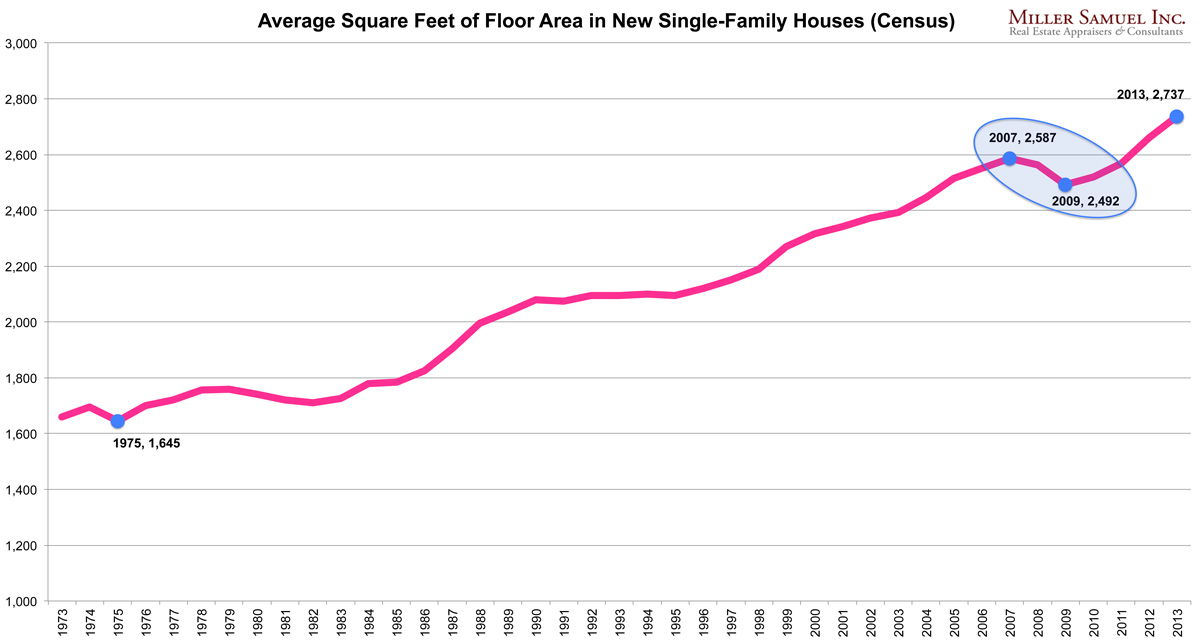

Trends in Home Size and Home Ownership React to Economic Conditions, Not Taste

read more

June 8, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

Manhattan

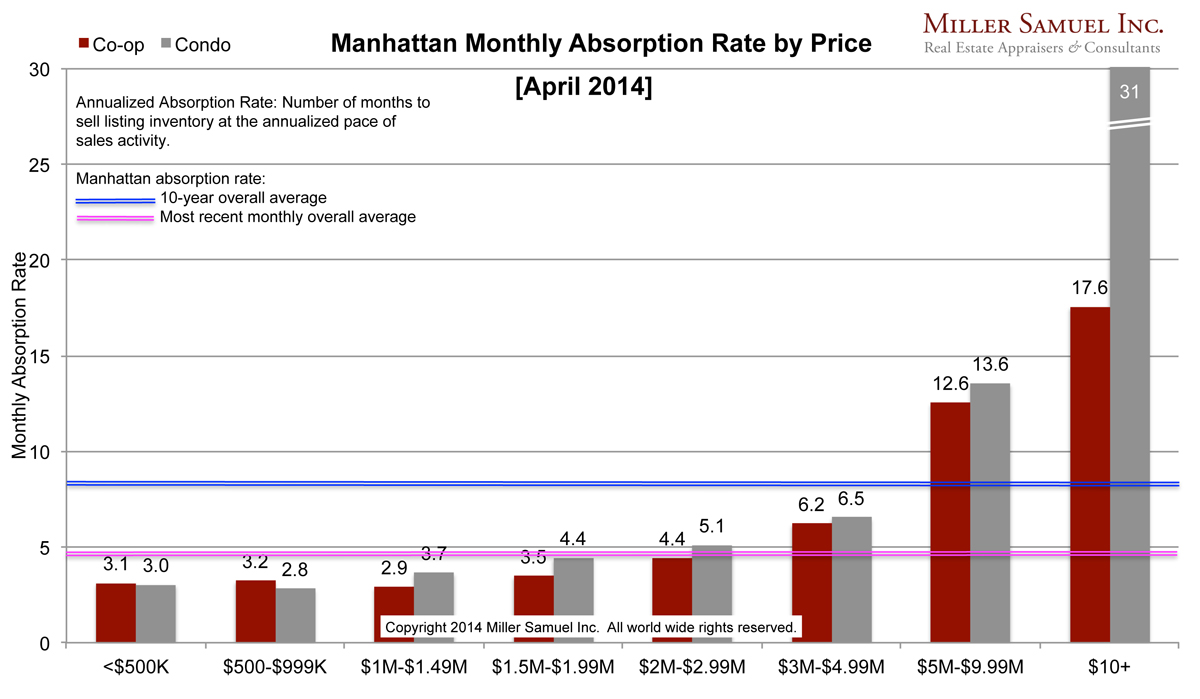

[Manhattan Absorption] May 2014 – Swimming in high-end condos.

read more

May 29, 2014

Housing Trends & Cycles

,

Market Reports

Pending Home Sales Fall Short of Year Ago Sales Surge

read more

May 27, 2014

Historical, Landmark, Milestone

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

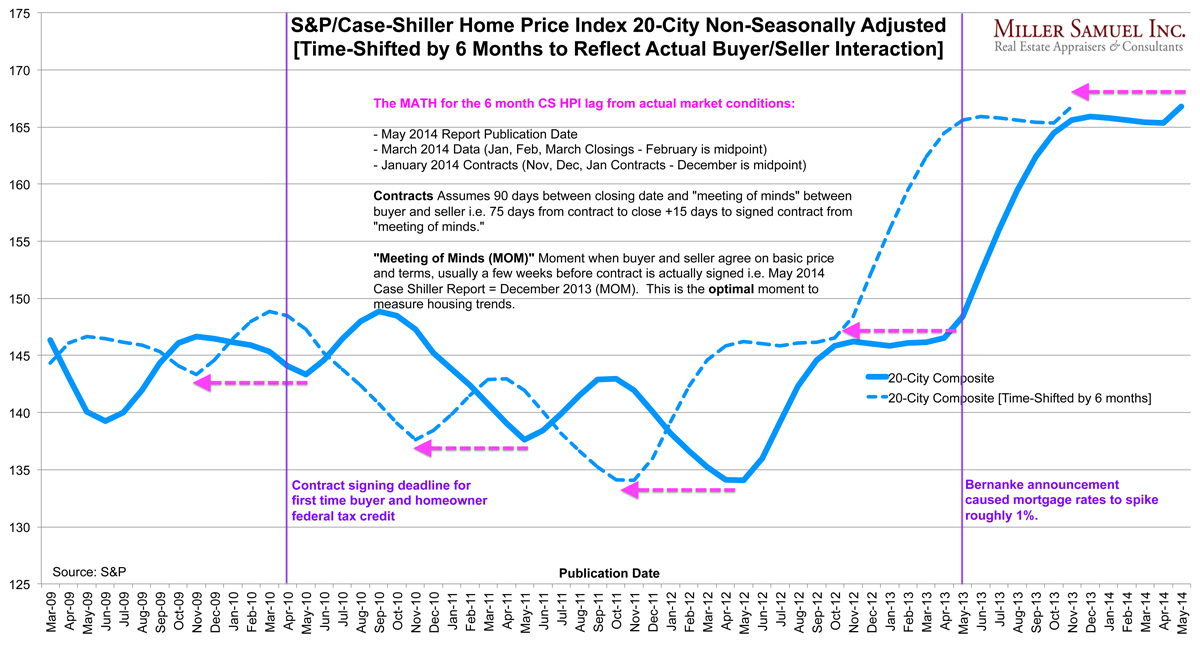

Pulling the Case-Shiller Index Back by 6 Months to Reflect Actual Buyer/Seller Behavior

read more

May 27, 2014

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

Thank Goodness The Pace of US Home Price Growth Will Cool

read more

May 27, 2014

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Manhattan

[Three Cents Worth #266 NY] Inventory Is Rising, Just Not Enough

read more

May 19, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

,

Manhattan

[Manhattan Absorption] April 2014 – Market Pace At Top Eases As Remainder Accelerates

read more

May 14, 2014

Affordability, Affordable Housing

,

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Luxury, Super, Ultra, Mega

,

Manhattan

[Three Cents Worth #265 NY] Gap Between Starter, Luxury Markets Grows

read more

April 4, 2014

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Manhattan

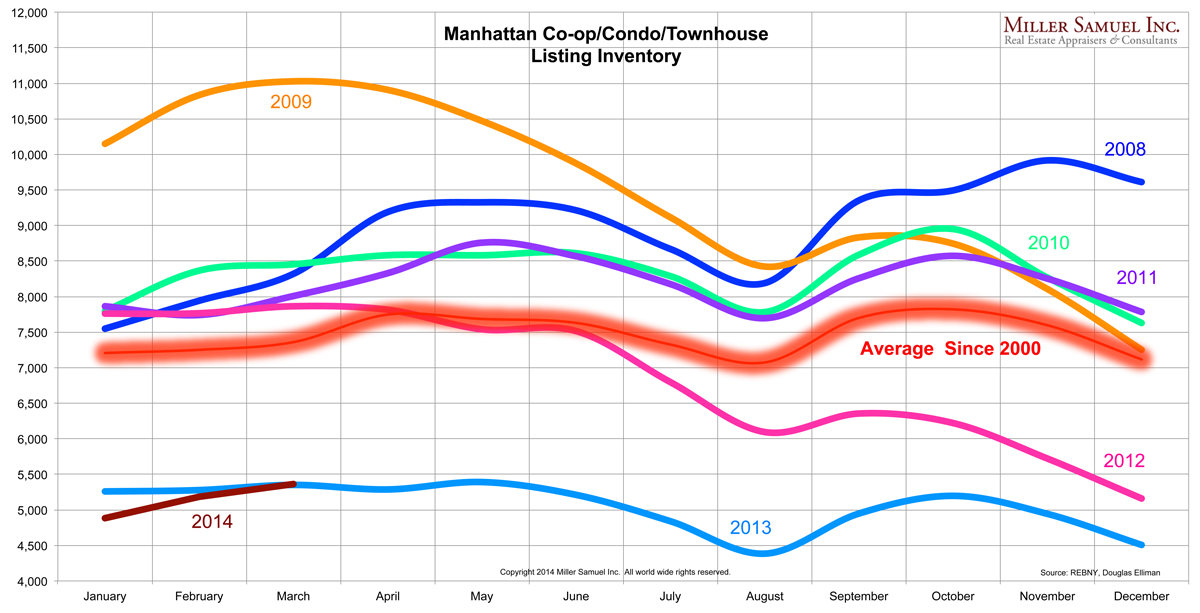

[Chart] Manhattan Inventory Reached Bottom After 4 Years of Decline

read more

April 3, 2014

Elliman Reports

,

Manhattan

,

Statistics, Metrics & Data

[Chart] Manhattan Co-op/Condo/Townhouse Monthly Listing Inventory Remains Woefully Low

read more

April 2, 2014

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Manhattan

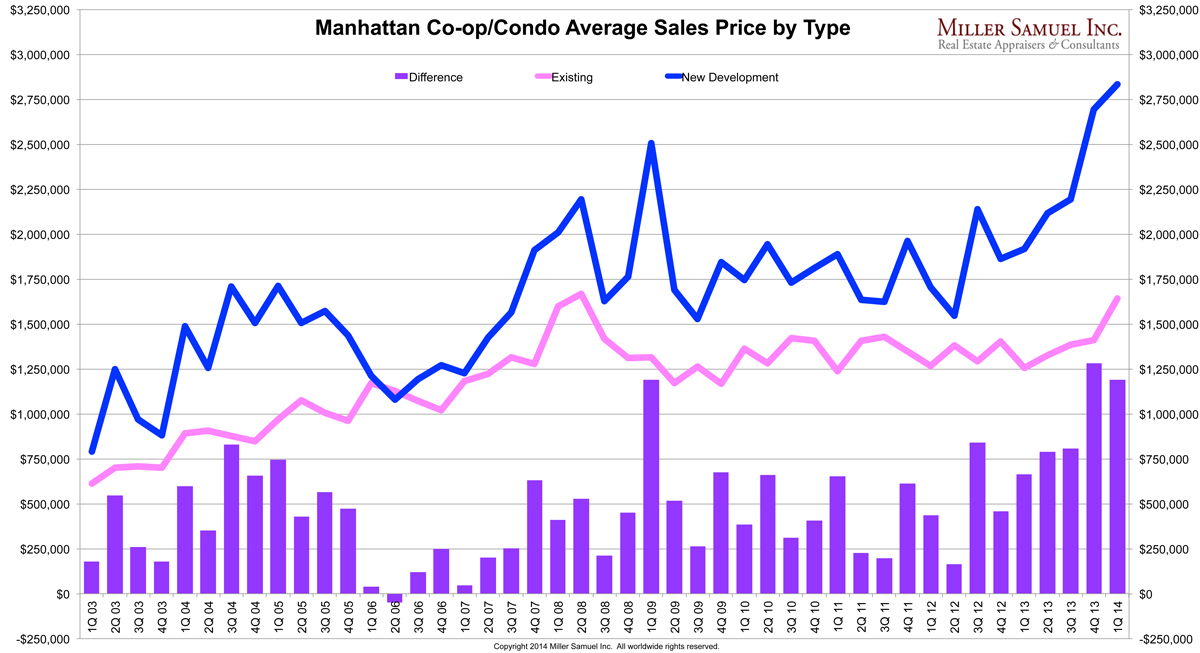

[Chart] Separating New Development From Existing Sales Shows Sharply Higher Trend

read more

March 27, 2014

Analysis & Research

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Market Reports

Pending Home Sales Down 10.2% YOY And That’s Not A Bad Thing

read more

Previous

7

8

9

Next

Load More Posts

Page load link

Go to Top