Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Wall Street Journal

September 16, 2013

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

New York Times

,

Wall Street Journal

The Low Appraisal “Hassle” is a Symptom of a Broken Mortgage Process

read more

July 1, 2013

Charts, Maps, Images, Infographics, Video

,

Economy

,

Wall Street Journal

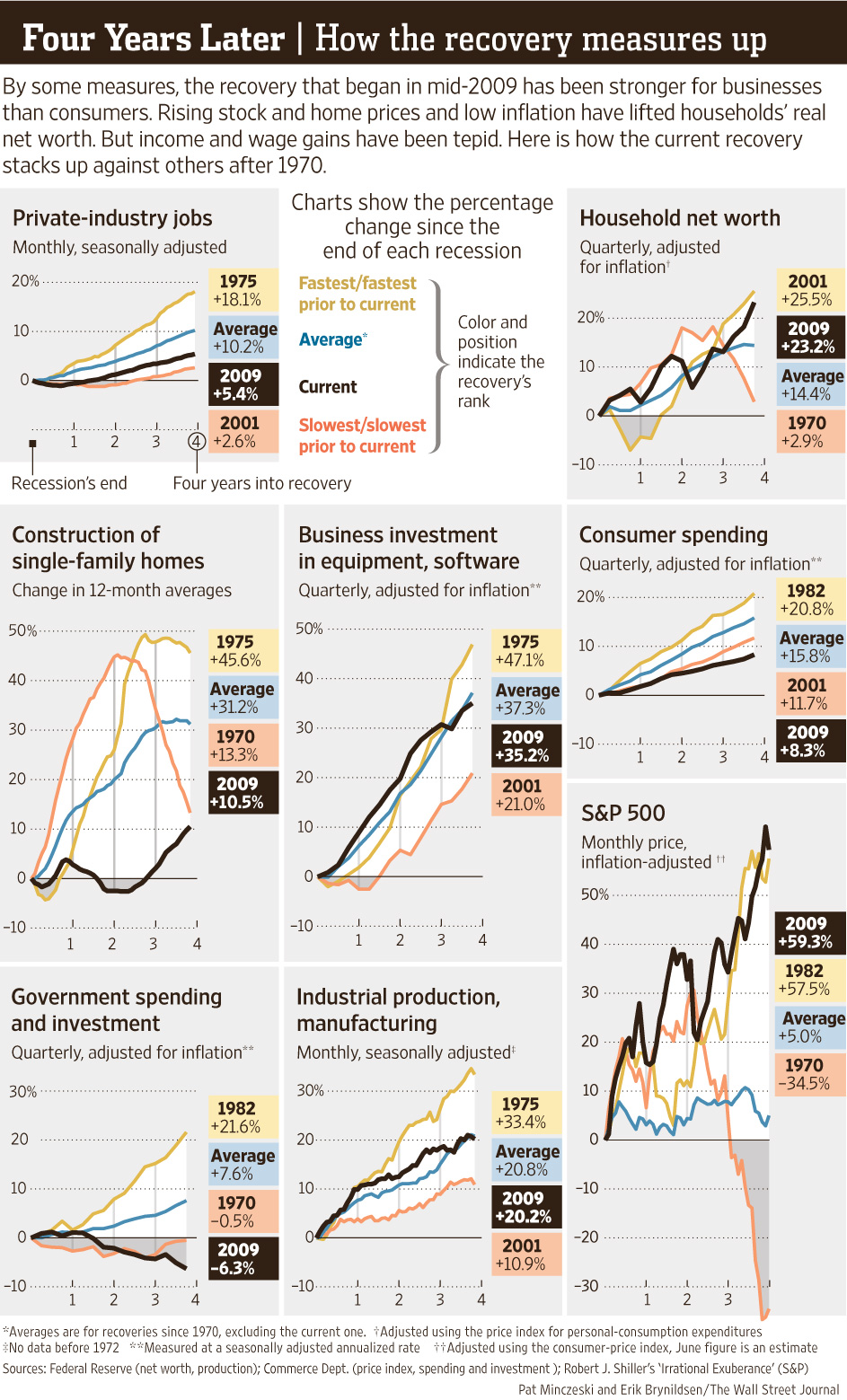

Cool WSJ Infographic on Economic Recovery Since End of Recession

read more

February 4, 2013

Amenities, Adjustments & Value Logic

,

Trulia

,

Wall Street Journal

Should We Adjust Housing For Inflation?

read more

February 1, 2013

Elliman Reports

,

Manhattan

,

Wall Street Journal

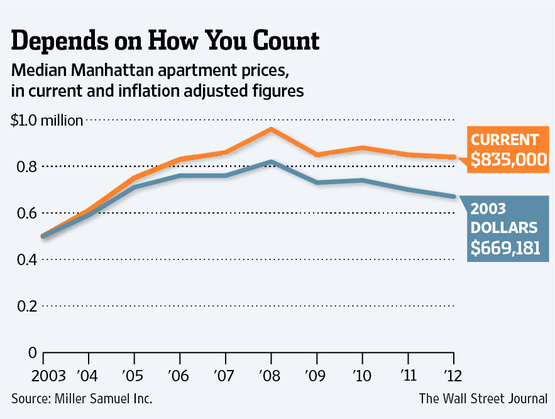

[WSJ Live] InflationWatch: Why Manhattan is a “Bargain”

read more

January 29, 2013

Hamptons/North Fork

,

Taxes, Insurance, Fees

,

Wall Street Journal

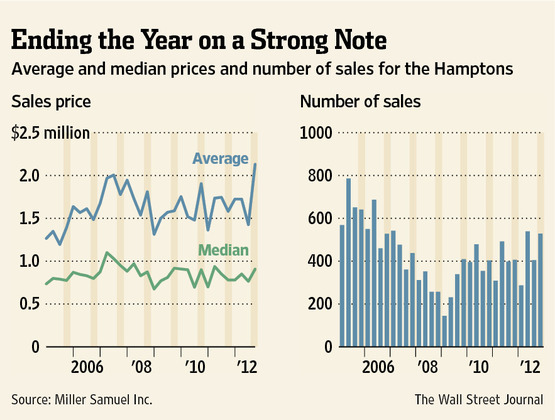

Hampton Year End Sales And Price Spike, Fiscal Cliff Style

read more

December 7, 2012

Housing Indices & Portals

,

International

,

Knight Frank

,

Market Reports

,

South Florida

,

Wall Street Journal

,

Weather & Natural Disasters

Looking For That Ray – Knight Frank’s Sunshine Index

read more

December 5, 2012

Boom Bubble Bust

,

Canada

,

International

,

Wall Street Journal

Housing Bubble – Canada Is Following US Lead

read more

December 1, 2012

Appraising

,

Law, Ethics & Fraud

,

Media

,

Wall Street Journal

Divorce Valuations: Appraiserville Meets Splitsville

read more

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

November 26, 2012

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

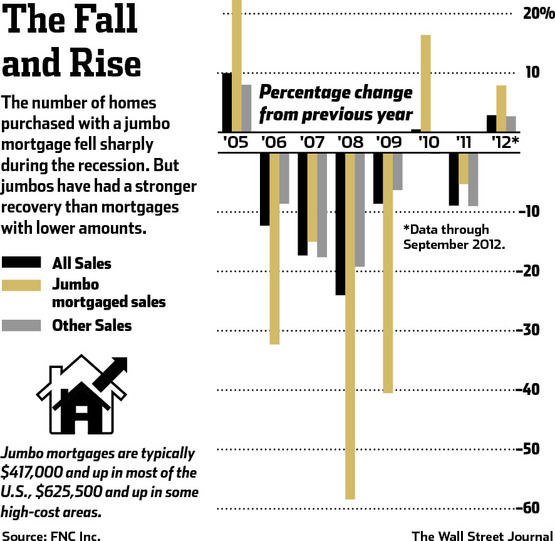

Jumbos Fell Harder, Now Rising Faster, But Off Low Base

read more

July 9, 2012

Distressed Housing

,

Elliman Reports

,

Wall Street Journal

Low Housing Inventory Is NOT A Sign of Housing Recovery

read more

June 9, 2012

Elliman Reports

,

Housing Indices & Portals

,

Trulia

,

Wall Street Journal

,

Weather & Natural Disasters

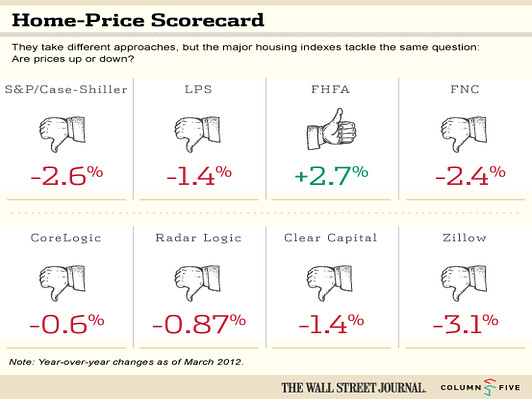

[WSJ] The Crazy 8: Comparing Results of National Home Price Indices

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top