Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Commerce Dept

March 27, 2014

Economy

,

International

,

Manhattan

,

Rentals, Investing

,

Wall Street Journal

,

Wall Street, Financial Services

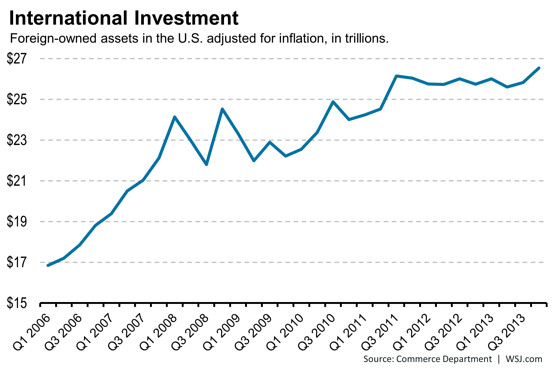

New Record of Foreign-owned Assets in the United States

read more

February 26, 2014

Housing Trends & Cycles

,

Language, Jargon & Quotes

,

Market Reports

,

Trulia

,

Wall Street Journal

[WSJ] Good Overview on 2014 US Housing Expectations – Jed Kolko, Trulia

read more

February 20, 2014

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Media

,

Statistics, Metrics & Data

,

Weather & Natural Disasters

Housing Starts Drop: Whether the Weather or New Trend?

read more

June 17, 2010

Government, Politics, Regulations & Policy

,

Market Reports

,

Statistics, Metrics & Data

[Commerce Dept] US Housing Starts May 2010

read more

June 2, 2010

Government, Politics, Regulations & Policy

,

Migration, Psychology, Demographics

,

Statistics, Metrics & Data

,

Wall Street Journal

[College Degree Sprawl] San Francisco and NYC are Bastions of Smart People

read more

December 22, 2009

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Government, Politics, Regulations & Policy

,

IRS

,

Market Reports

,

Statistics, Metrics & Data

,

Wall Street Journal

[Not Really Counted] 1.7M Units In Shadow Housing Inventory

read more

September 26, 2009

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Market Reports

,

Statistics, Metrics & Data

[New Home Sales] Inventory Falls As Sales Flatten

read more

August 27, 2009

Government, Politics, Regulations & Policy

,

Market Reports

,

New York Times

,

Statistics, Metrics & Data

[New Home Sales] Up 9.6% – New Is Better Too?

read more

July 30, 2009

Blogging Off The Matrix

,

Books & Movies

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

IRS

,

New York Times

,

Statistics, Metrics & Data

[HuffPost] Current Wave of Housing Euphoria May Extend Downturn

read more

July 27, 2009

Government, Politics, Regulations & Policy

,

Market Reports

,

New York Times

,

Statistics, Metrics & Data

[Repetition Watch] New Home Sales Up

read more

May 17, 2009

Government, Politics, Regulations & Policy

,

Guest Post (Vortex)

,

Housing Trends & Cycles

,

International

,

New York Times

,

Statistics, Metrics & Data

[Vortex] Straight from MacCrate: When Will Real Estate Prices Stabilize in the New York Metropolitan Area?

read more

April 13, 2009

Bloomberg News

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Language, Jargon & Quotes

,

Migration, Psychology, Demographics

,

New York Times

,

Statistics, Metrics & Data

,

Wall Street Journal

,

Weather & Natural Disasters

[Pretty Vacant] Shoots of Green Are Blossoming In The Metaphor Business

read more

1

2

Next

Load More Posts

Page load link

Go to Top