Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Case-Shiller

January 28, 2013

Economy

,

Homebuying Process

,

Housing Indices & Portals

,

Language, Jargon & Quotes

,

New York Times

,

RealtyTrac

Falling Inventory Has Created a Housing “Pre-Covery,” not “Recovery”

read more

December 27, 2012

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

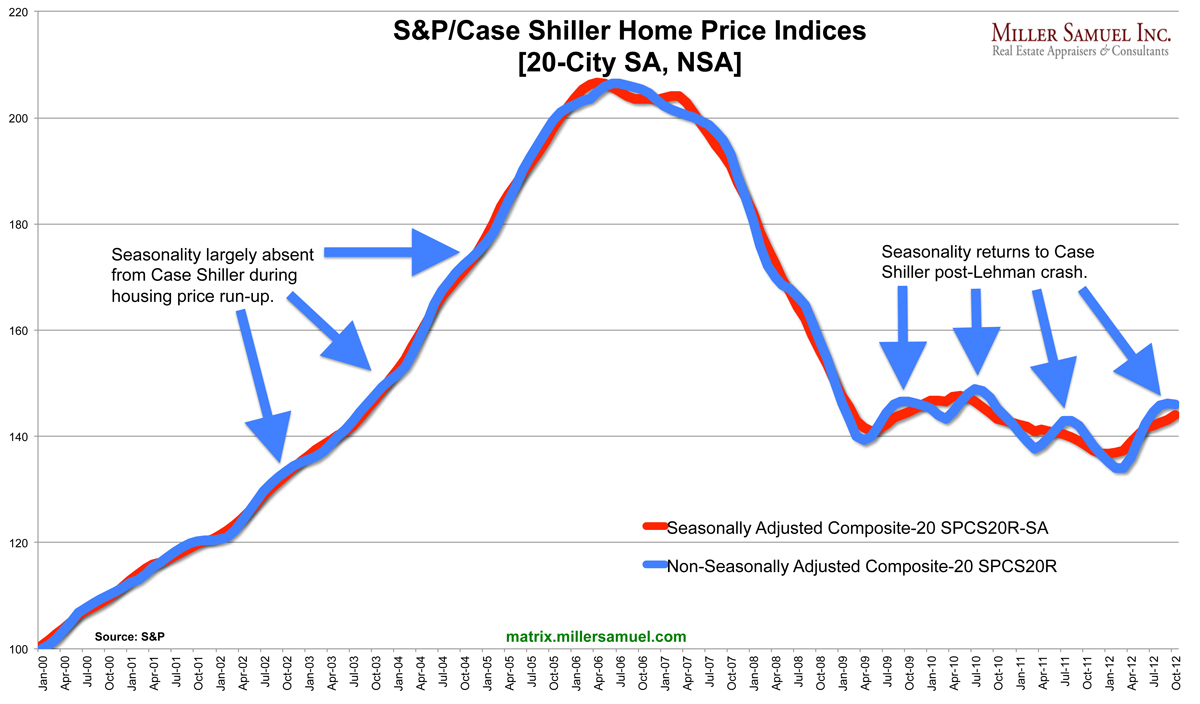

[Case Shiller] Recovery Is Back In Season

read more

December 13, 2012

Housing Indices & Portals

,

International

,

Knight Frank

,

Market Reports

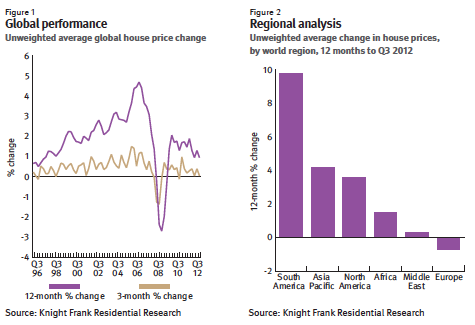

[Knight Frank] Global Reports That Look Forward and Backward : Europe As Denominator

read more

December 6, 2012

Brokers, Agents, MLS, NAR

,

Elliman Reports

,

Housing Indices & Portals

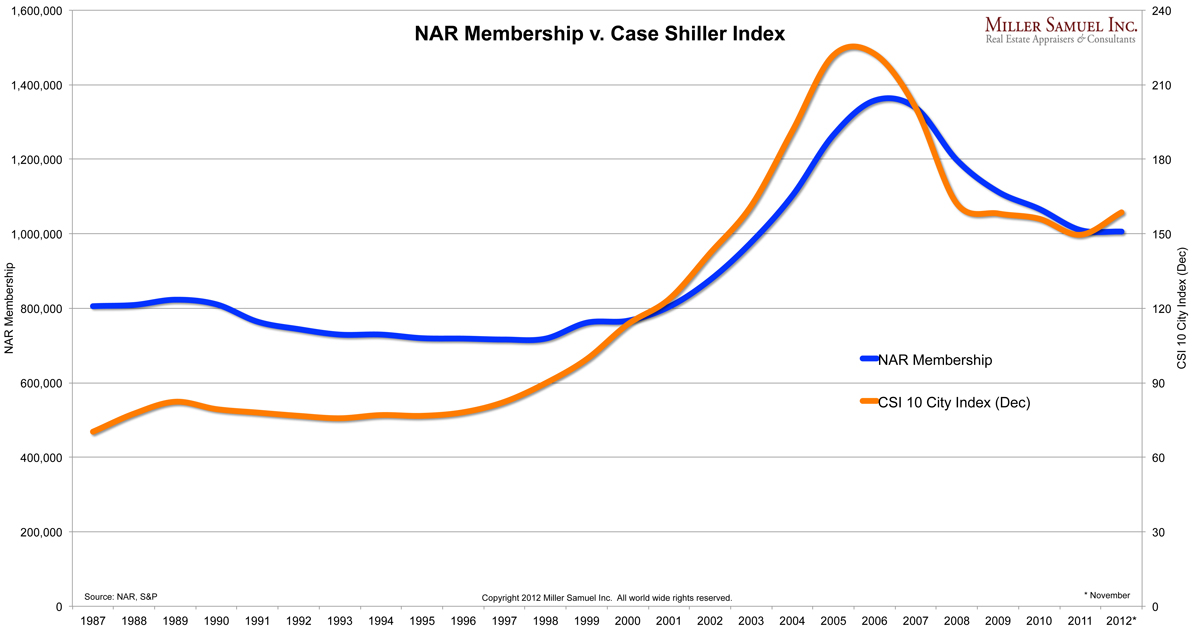

NAR Membership Flows With Housing Market

read more

December 4, 2012

Brooklyn

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

[NewYork Fed] Excellent Mapping of Housing’s Recovery Process in Region

read more

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

September 25, 2012

Appraising

,

Elliman Reports

,

Housing Indices & Portals

[Breaking News] CNN Gives Housing Followers Heart Attack, Case Shiller Up 1.2% YOY

read more

September 4, 2012

Brokers, Agents, MLS, NAR

,

Housing Indices & Portals

,

Inman News

,

South Florida

NAR and Florida Realtors to Create Repeat Sales Index: Why?

read more

July 19, 2012

Media

[In The Media] Yahoo!’s ‘The Daily Ticker’ With Dan Gross 7-19-12

read more

June 9, 2012

Elliman Reports

,

Housing Indices & Portals

,

Trulia

,

Wall Street Journal

,

Weather & Natural Disasters

[WSJ] The Crazy 8: Comparing Results of National Home Price Indices

read more

November 18, 2010

Analysis & Research

,

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Interviews

,

Market Reports

,

The Housing Helix

[Interview] Robert Dorsey, Chief Data and Analytics Officer, FNC Co-Founder

read more

May 10, 2010

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve, New York

,

Housing Indices & Portals

,

IRS

,

New York Times

[Bubbletheory] Lets Not Re-write History

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top