Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Seasonal Adjustment

April 26, 2010

Housing Indices & Portals

,

Market Reports

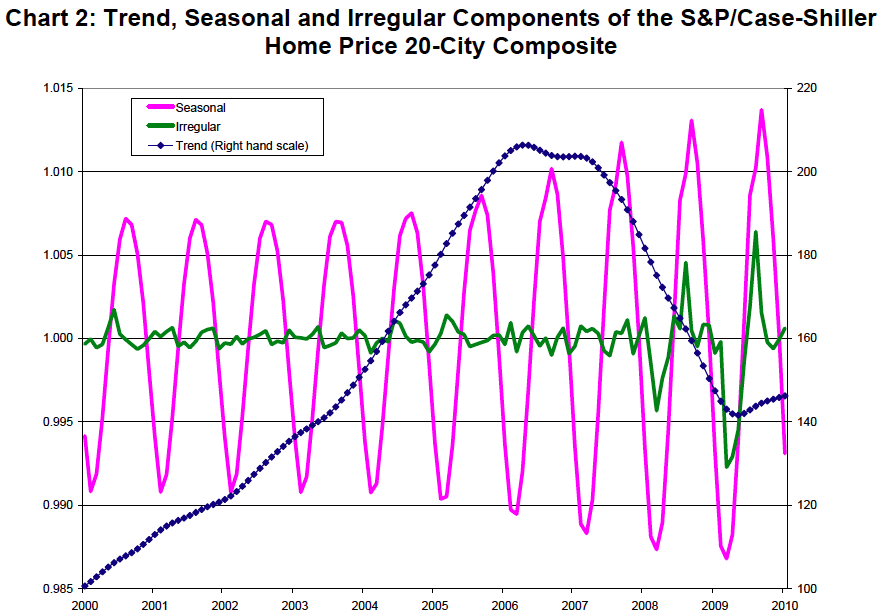

[Seasonality Adjustments] are Confusing and Perhaps, Misleading

read more

February 11, 2010

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Government, Politics, Regulations & Policy

,

New York Times

,

RealtyTrac

,

South Florida

[RealtyTrac] 10% Drop In Foreclosures, Surge Expected Over Next Few Months

read more

November 23, 2009

Bloomberg News

,

Books & Movies

,

Brokers, Agents, MLS, NAR

,

IRS

,

Market Reports

,

Wall Street Journal

[Tax Credit] Existing Home Sales Up 10.1% M-O-M, 23.5% Y-O-Y

read more

November 2, 2009

Brokers, Agents, MLS, NAR

,

Housing Indices & Portals

,

IRS

,

Market Reports

[Seasonalized?, Annualized?] Pending Home Sales Index Up 8th Consecutive Month

read more

July 30, 2009

Blogging Off The Matrix

,

Books & Movies

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

IRS

,

New York Times

,

Statistics, Metrics & Data

[HuffPost] Current Wave of Housing Euphoria May Extend Downturn

read more

July 23, 2009

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Long Island

,

Market Reports

[Going Long] 2Q 2009 Long Island Market Overview Available For Download

read more

July 2, 2009

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Market Reports

[Where Credit Is Due] 2Q 2009 Manhattan Market Overview Available For Download

read more

May 6, 2009

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Language, Jargon & Quotes

,

New York Times

[FIFO and Bottoming?] Glimmer Is More Popular Than Location These Days

read more

March 25, 2009

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Economy

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

[Selling MOM Out] Month Over Month, ‘Cause It Looks Better

read more

January 26, 2009

Charleston, SC

,

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

City Of Architecture: 2008 Market Report For Charleston, SC

read more

August 26, 2008

Affordability, Affordable Housing

,

Bloomberg News

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Migration, Psychology, Demographics

,

New York Times

[Bullish In Technicolor] Housing Prices Show More Weakness

read more

July 14, 2008

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Economy

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

New York Times

[Smoking Gun Crack] Signs Of Housing Recovery

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top