Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Seasonal Adjustment

May 16, 2015

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Sales

Bloomberg View Column: A Housing Recovery Built to Last?

read more

February 8, 2015

Blogging Off The Matrix

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Homebuying Process

,

Housing Trends & Cycles

,

International

,

Weather & Natural Disasters

Bloomberg View Column: Housing Market Blows Hot and Cold

read more

March 23, 2014

Credit, Finance, Mortgage, Rates

,

Market Reports

,

Weather & Natural Disasters

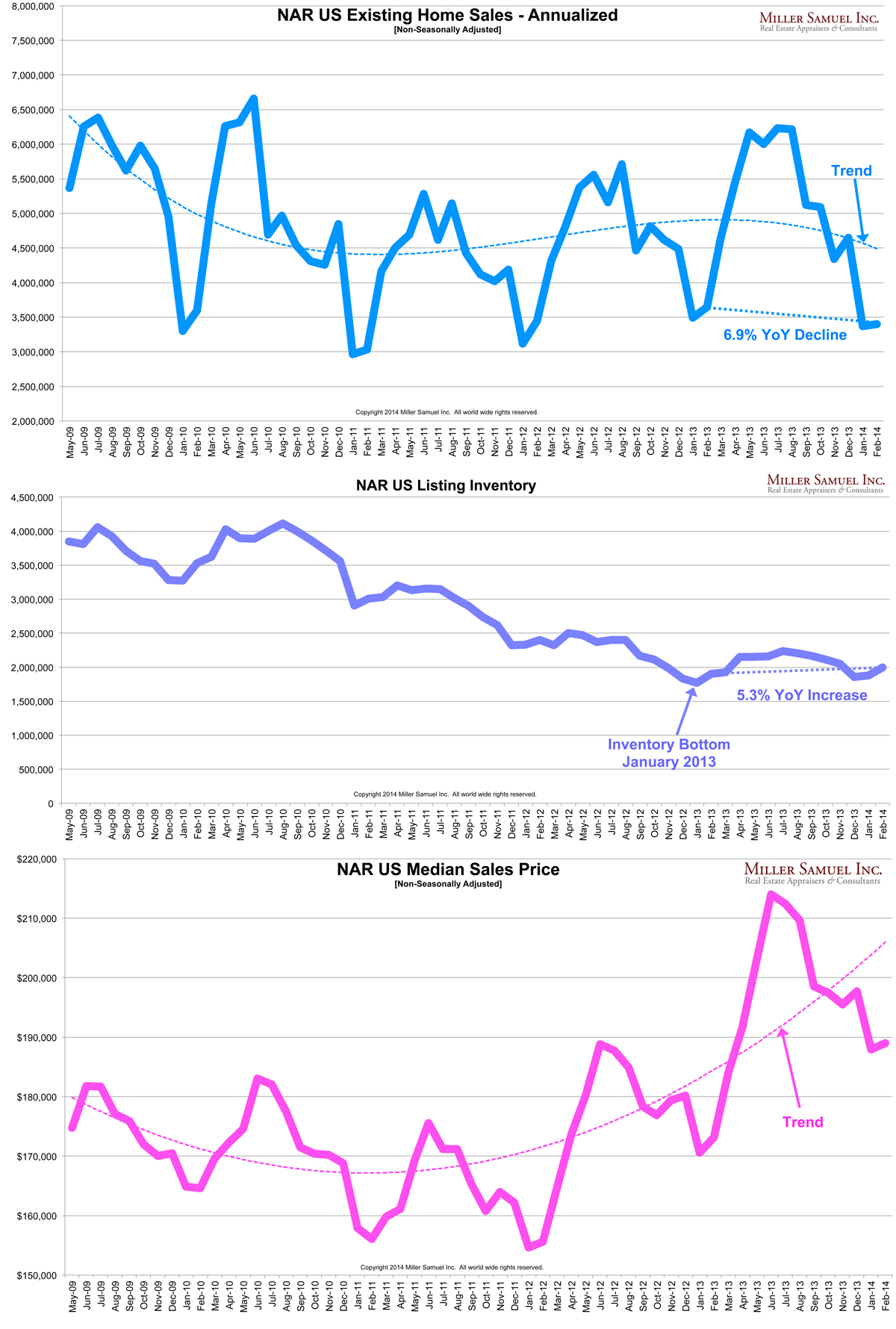

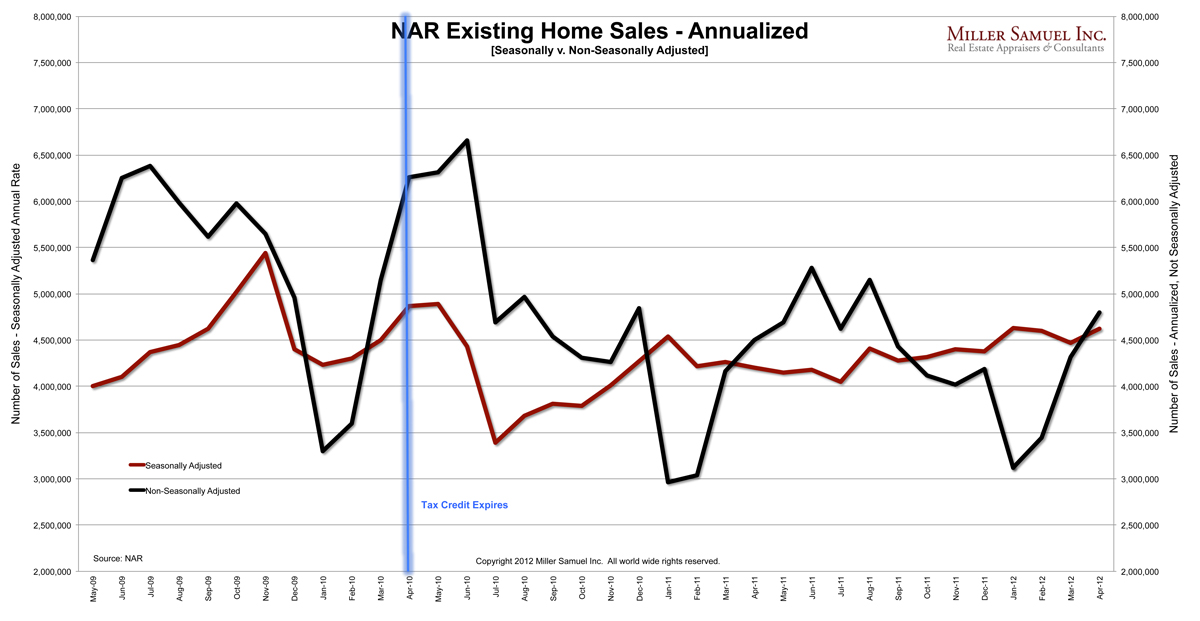

NAR Existing Home Sales Blink, And So What?

read more

October 28, 2013

Brokers, Agents, MLS, NAR

,

Market Reports

,

New York Times

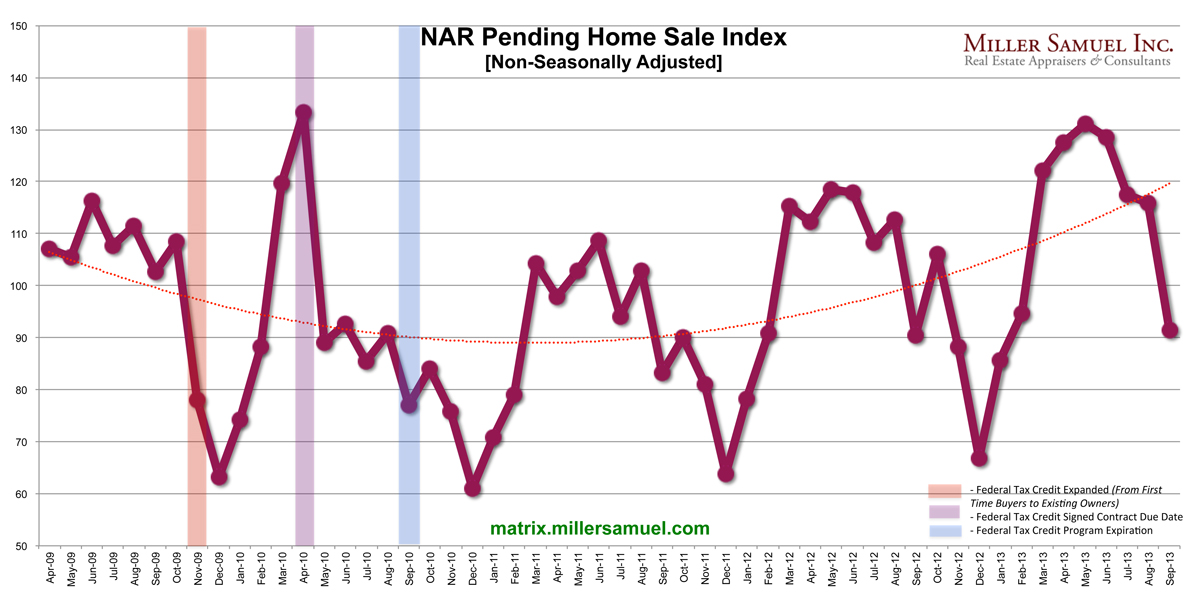

NAR Pending Home Sale Index Sort of Goes Negative

read more

May 29, 2013

Bloomberg News

,

Elliman Reports

,

Housing Indices & Portals

,

Media

Talking Case Shiller on Bloomberg TV’s ‘Street Smart” with Betty Liu/Adam Johnson

read more

February 5, 2013

Blogging Off The Matrix

,

Curbed

[Three Cents Worth NY #222] Is the Bottom Falling Out of Inventory?

read more

December 27, 2012

Amenities, Adjustments & Value Logic

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

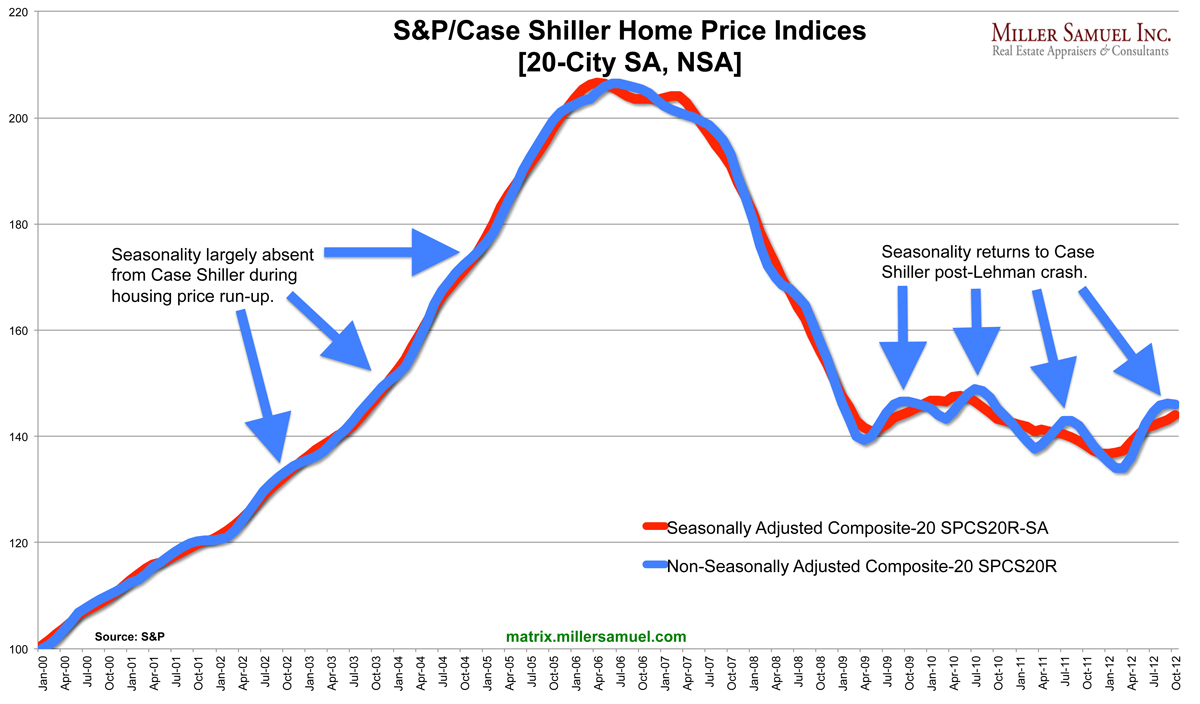

[Case Shiller] Recovery Is Back In Season

read more

July 31, 2012

Blogging Off The Matrix

,

Curbed

,

Douglas Elliman

[Three Cents Worth NY #200] Manhattan’s Seasons, “The 200” Version

read more

May 22, 2012

Bloomberg News

,

Brokers, Agents, MLS, NAR

[NAR] Existing Home Sales Continue to Edge Higher +10% Y-O-Y

read more

May 3, 2010

Credit, Finance, Mortgage, Rates

,

Economy

,

Social, Tech, Gadgets, Software

[Charticlismic] Matching Google Searches To Real Estate

read more

April 27, 2010

IRS

,

Westchester County, NY

[WPAR] 1Q 2010 Westchester County, NY: Tax Credit Driving Sales

read more

April 27, 2010

Appraising

,

Guest Post (Vortex)

,

Westchester County, NY

[Vortex] The Hall Monitor: Seasonality Should be Considered in Comp Selection

read more

1

2

Next

Load More Posts

Page load link

Go to Top