Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Statistics, Metrics & Data

August 31, 2014

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Manhattan

,

Statistics, Metrics & Data

[Three Cents Worth #269 NY] Charting A Decade of Manhattan Inventory

read more

June 9, 2014

Charts, Maps, Images, Infographics, Video

,

Distressed Housing

,

Housing Trends & Cycles

,

Op-Ed

,

Statistics, Metrics & Data

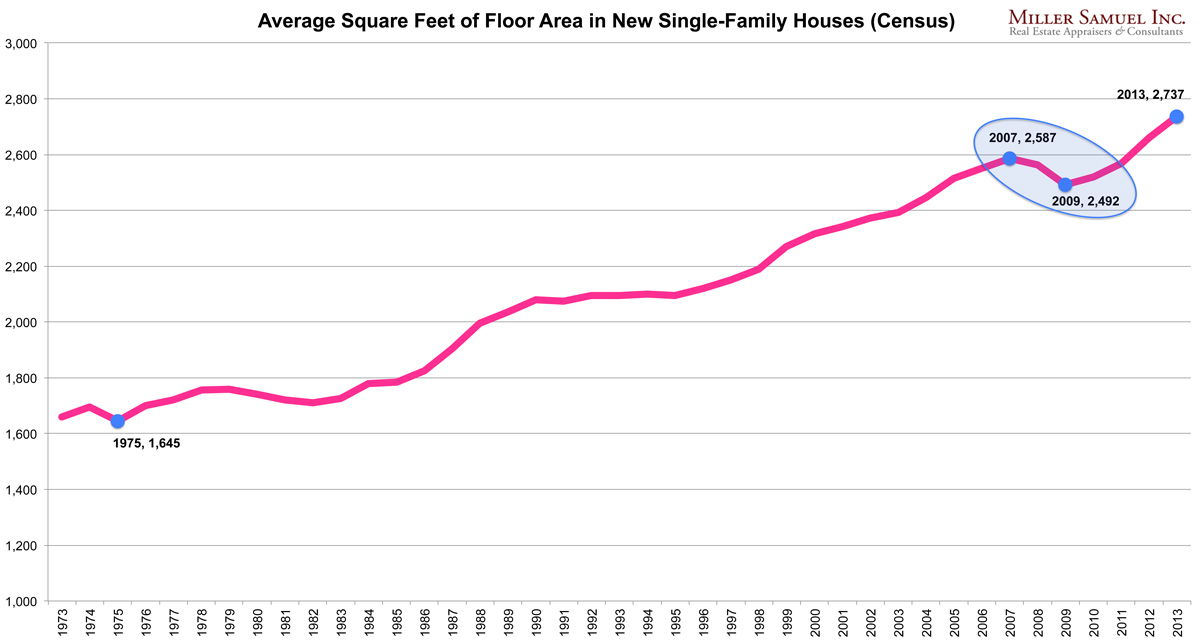

Trends in Home Size and Home Ownership React to Economic Conditions, Not Taste

read more

May 17, 2014

Analysis & Research

,

Backyard BBQ Talk

,

Credit, Finance, Mortgage, Rates

,

Douglas Elliman

,

Manhattan

,

RealtyTrac

,

Statistics, Metrics & Data

Manhattan Home Sales Are NOT 80% All-Cash (They Are 45%)

read more

April 18, 2014

Boca Raton

,

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Housing Trends & Cycles

,

Miami (Beach + Mainland)

,

Palm Beach

,

South Florida

,

Statistics, Metrics & Data

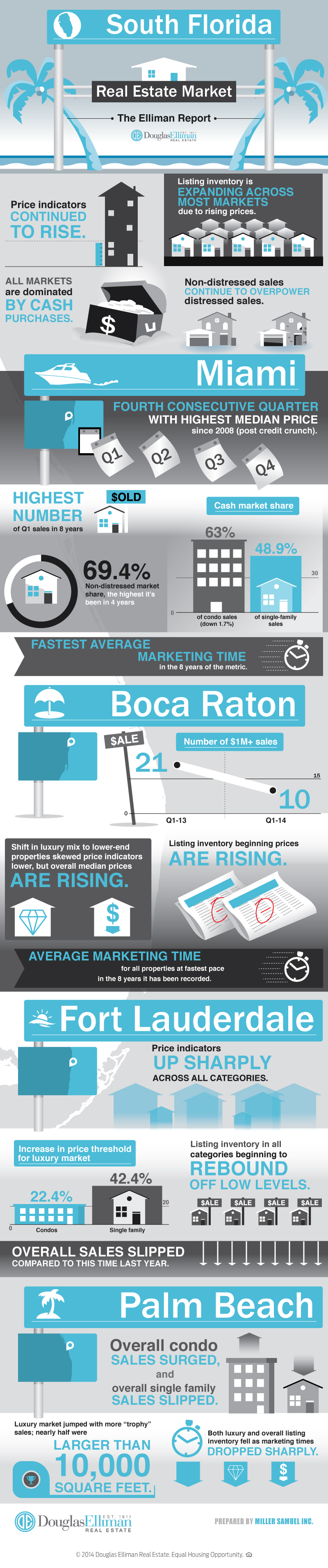

[Infographic] Getting Graphic in South Florida in 1Q 2014

read more

April 3, 2014

Elliman Reports

,

Manhattan

,

Statistics, Metrics & Data

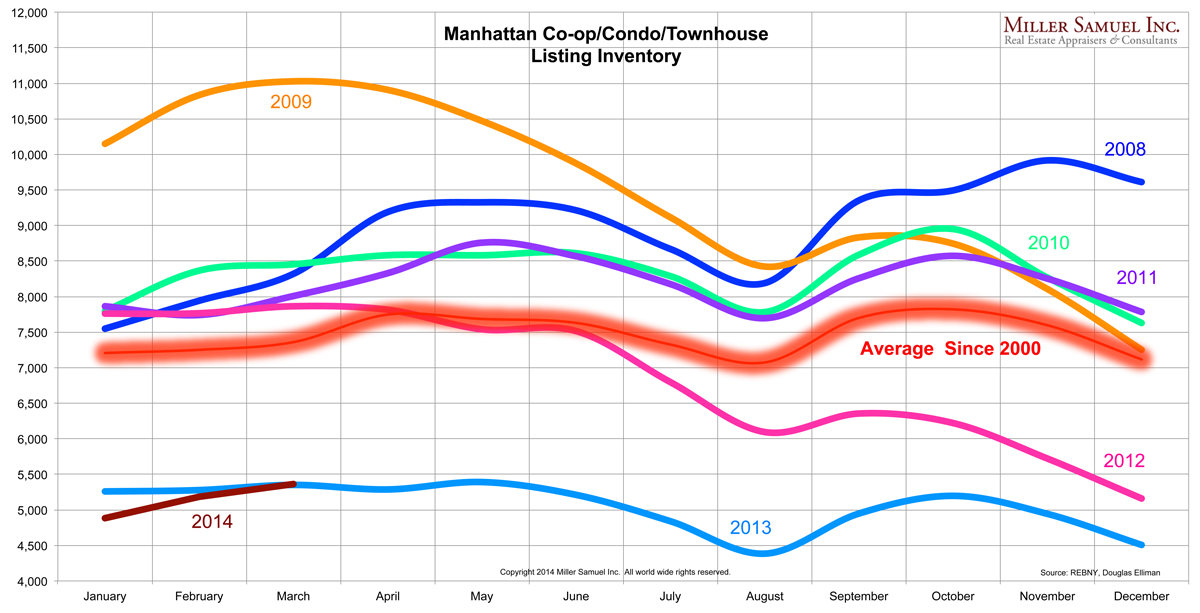

[Chart] Manhattan Co-op/Condo/Townhouse Monthly Listing Inventory Remains Woefully Low

read more

April 1, 2014

Charts, Maps, Images, Infographics, Video

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Statistics, Metrics & Data

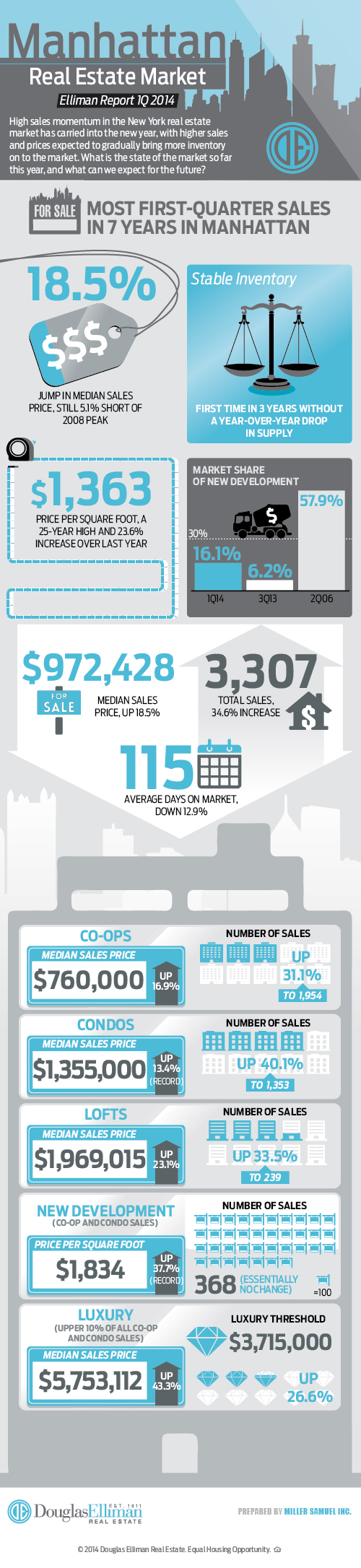

[Infographic] Manhattan Sales Market 1Q14

read more

March 21, 2014

Charts, Maps, Images, Infographics, Video

,

Federal Reserve, New York

,

New Jersey

,

New York City

,

Statistics, Metrics & Data

NY Fed: New York City and State Expanding at “Brisk Pace”

read more

March 15, 2014

Brooklyn

,

Douglas Elliman

,

Elliman Reports

,

Manhattan

,

Rentals, Investing

,

Statistics, Metrics & Data

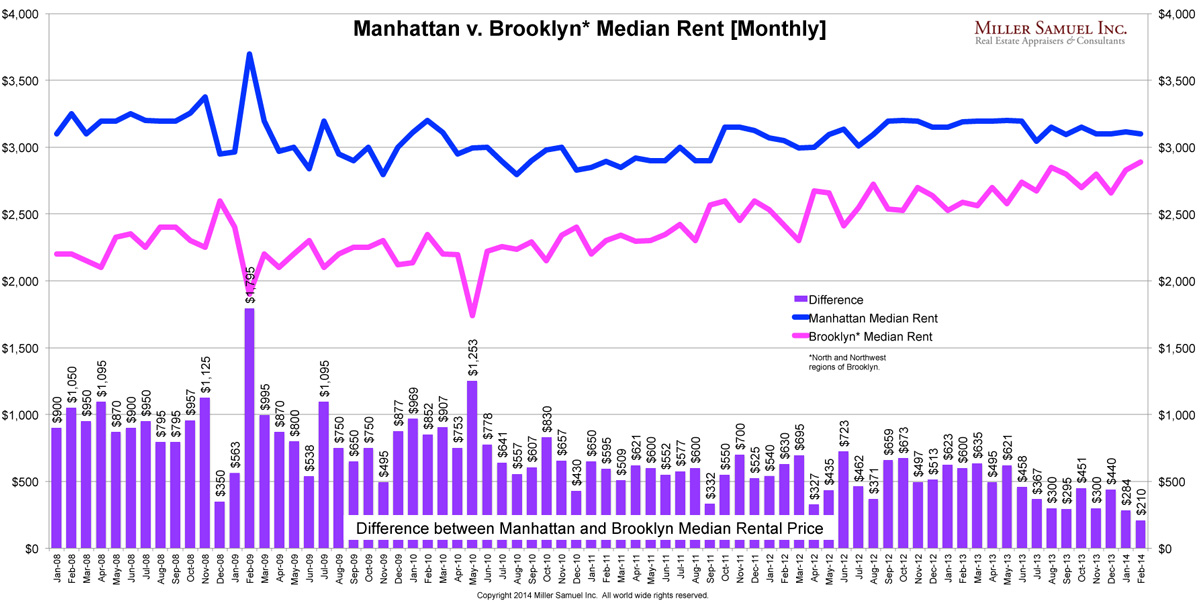

[Chart] The Manhattan-Brooklyn Median Rental Price Smackdown

read more

February 20, 2014

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Media

,

Statistics, Metrics & Data

,

Weather & Natural Disasters

Housing Starts Drop: Whether the Weather or New Trend?

read more

March 11, 2013

Analysis & Research

,

Bloomberg News

,

Government, Politics, Regulations & Policy

,

Media

,

Statistics, Metrics & Data

On Bloomberg TV, Surveillance w/Tom Keene 3-11-13: Housing, Mortgages, Rising Prices

read more

December 10, 2012

Analysis & Research

,

Appraising

,

Boom Bubble Bust

,

Celebrity, Pop Culture

,

Statistics, Metrics & Data

,

Wall Street, Financial Services

Serious Jibber-Jabber: Lessons from Nate Silver to Filter Out Housing Noise

read more

June 17, 2010

Government, Politics, Regulations & Policy

,

Market Reports

,

Statistics, Metrics & Data

[Commerce Dept] US Housing Starts May 2010

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top