Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Freddie Mac

March 16, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Op-Ed

,

Wall Street Journal

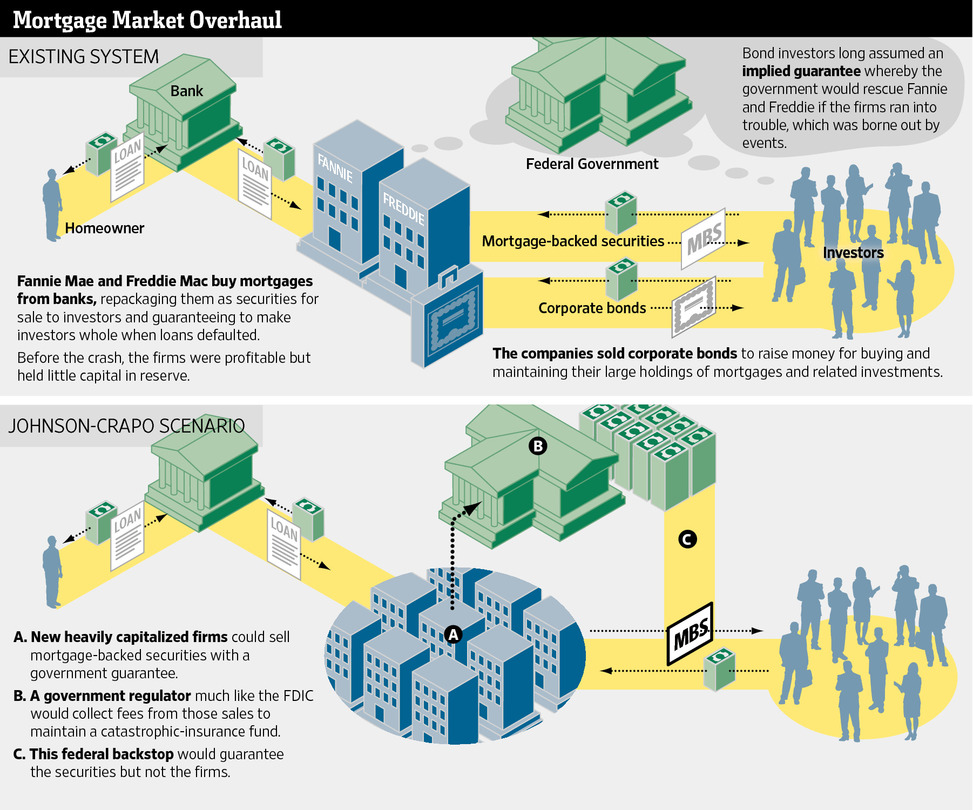

The Bi-Partisan Fannie and Freddie Solution That Isn’t A Fix

read more

February 25, 2014

Credit, Finance, Mortgage, Rates

,

Curbed

,

IRS

,

Manhattan

,

Rentals, Investing

,

Sales

[Three Cents Worth #260 NY] Looking At Manhattan’s Mortgage History

read more

November 26, 2012

Credit, Finance, Mortgage, Rates

,

Language, Jargon & Quotes

‘Structured By Cows’ and other Candid Catchphrases

read more

June 15, 2010

Credit, Finance, Mortgage, Rates

,

Furman Center

,

Government, Politics, Regulations & Policy

,

The Housing Helix

[The Housing Helix Podcast] Mark Willis, Research Fellow, NYU Furman Center

read more

June 7, 2010

Credit, Finance, Mortgage, Rates

,

Federal Reserve, New York

,

Furman Center

,

Government, Politics, Regulations & Policy

[Furman Center] Improving U.S. Housing Finance through Reform of Fannie Mae and Freddie Mac

read more

March 16, 2010

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Law, Ethics & Fraud

,

New York Times

[HVCC and AMCs Violate RESPA?] Here’s a possible solution

read more

May 19, 2009

Economy

,

Government, Politics, Regulations & Policy

[DMV-Like Executives] Placing All Our Housing Hopes On Institutions Losing Billions

read more

March 22, 2009

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

Rentals, Investing

,

Wall Street Journal

[Seeing only 70% of the Risk] Fannie Mae Crushed Condo New Development Sales

read more

January 14, 2009

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

New York Times

,

Rentals, Investing

,

Wall Street Journal

[Mortgage Appraisal Havoc] Of AMCs and Code of Conduct

read more

November 19, 2008

Books & Movies

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

New York Times

[FHFA /OFHEO] On A Mission, With Bear Oversight

read more

November 12, 2008

Appraising

,

Boom Bubble Bust

,

Commercial, Retail

,

Credit, Finance, Mortgage, Rates

[Crazy Inconvenient] Appraiser Should Use Recent Comps

read more

November 10, 2008

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Wall Street Journal

[Conforming Defined] The More Things Change, The More They Stay The Same

read more

1

2

Next

Load More Posts

Page load link

Go to Top