Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› COVID-19

June 28, 2020

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

New York City

,

Op-Ed

My Forbes Column: Keeping Housing Market Results From The Public Is Never Justified: An Expansive View

read more

May 20, 2020

Housing Trends & Cycles

,

New York City

,

New York City Suburbs

,

New York Times

,

Public Speaking

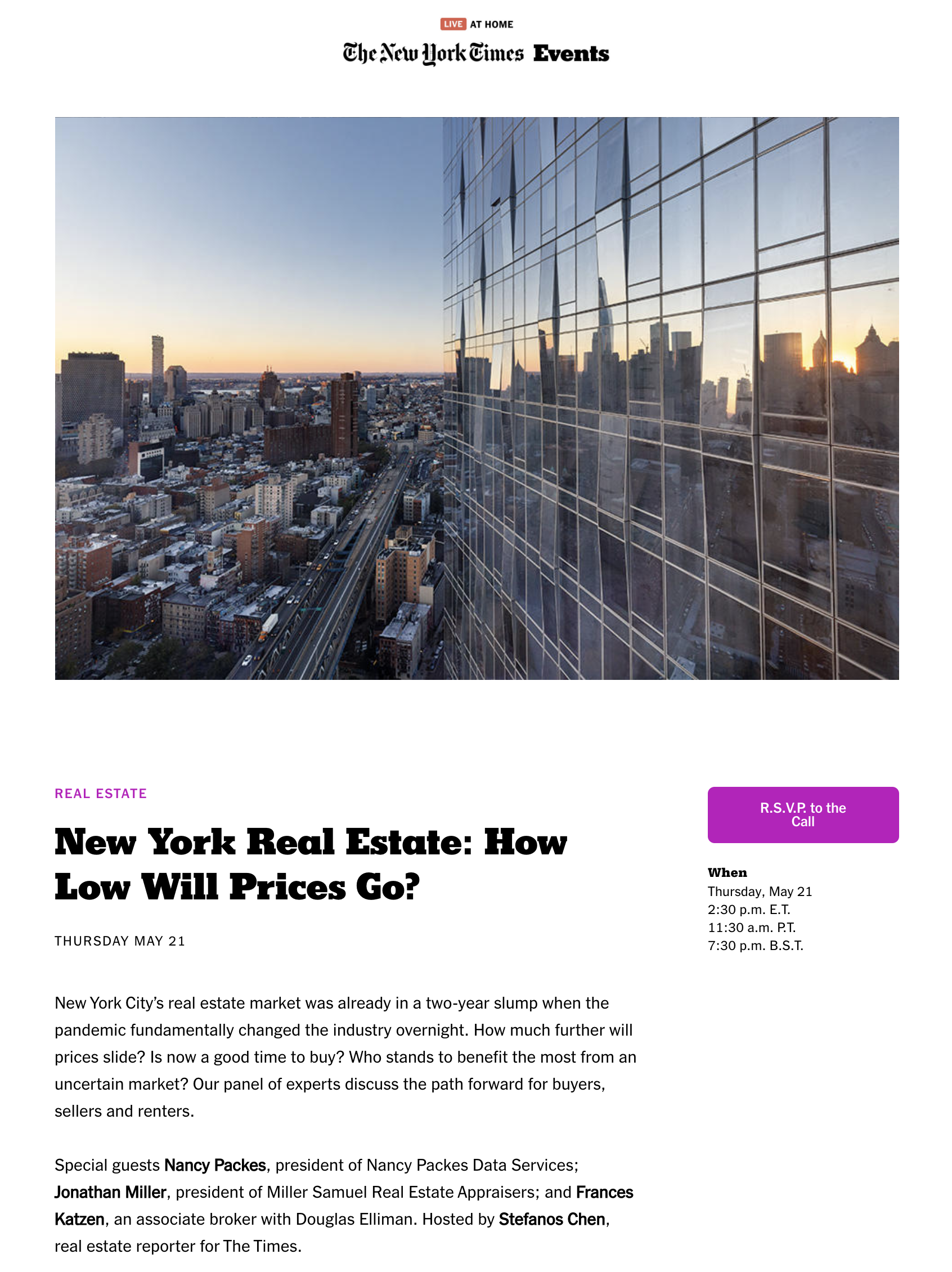

NYT Real Estate Event May 21st @2:30 E.T. New York Real Estate: How Low Will Prices Go?

read more

May 20, 2020

Charts, Maps, Images, Infographics, Video

,

Dutchess County, NY

,

Government, Politics, Regulations & Policy

,

Hamptons/North Fork

,

Manhattan

,

New York City

,

Putnam County

,

Weather & Natural Disasters

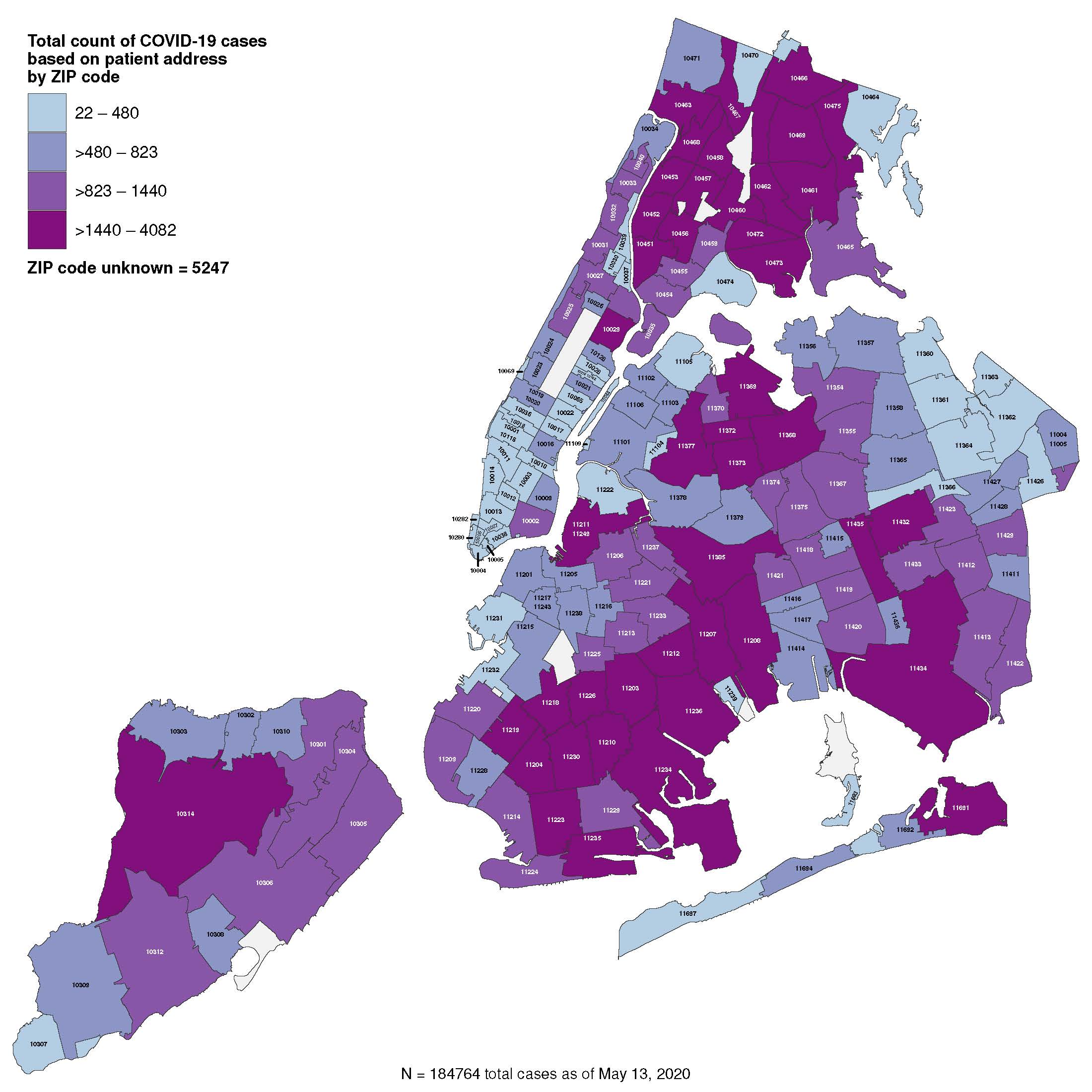

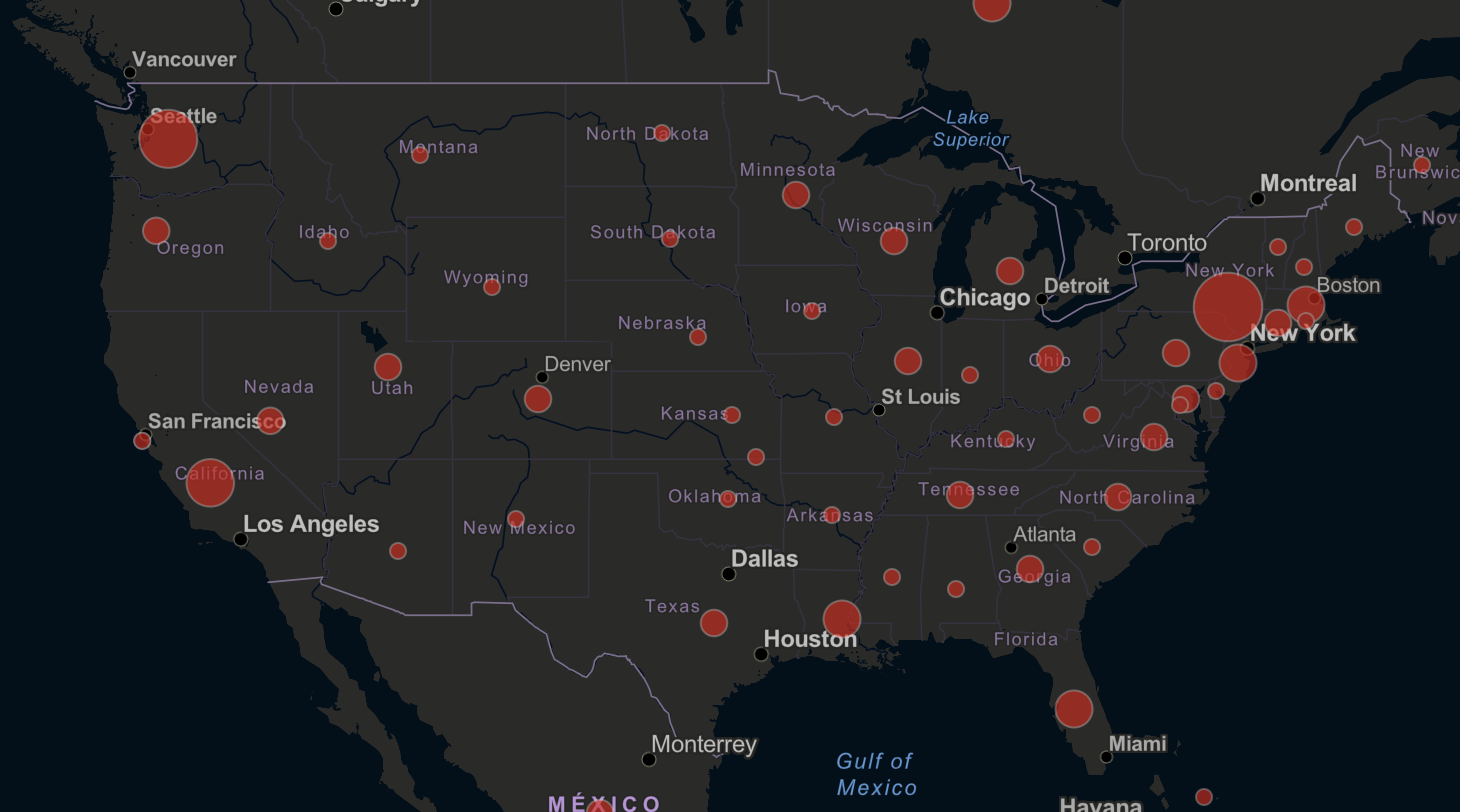

The Overstated COVID-19 Blame on Urban Density in Favor of Suburban Living

read more

May 3, 2020

Government, Politics, Regulations & Policy

,

New York City

,

New York City Suburbs

,

Suburban, Urban, Commuting

,

Weather & Natural Disasters

ABC World News Report 5-2-20 ‘Urban to Suburban’

read more

April 28, 2020

Amenities, Adjustments & Value Logic

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Historical, Landmark, Milestone

,

Housing Note

,

Manhattan

,

Weather & Natural Disasters

Establishing the COVID-19 Demarcation Line: From ‘Hanks To Banks’

read more

March 18, 2020

Appraising

,

Explainer

,

Government, Politics, Regulations & Policy

Some Financial Institutions Care About The Safety Of Appraisers, While Most Do Not

read more

March 18, 2020

Affordability, Affordable Housing

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Explainer

,

Homebuying Process

,

International

,

Weather & Natural Disasters

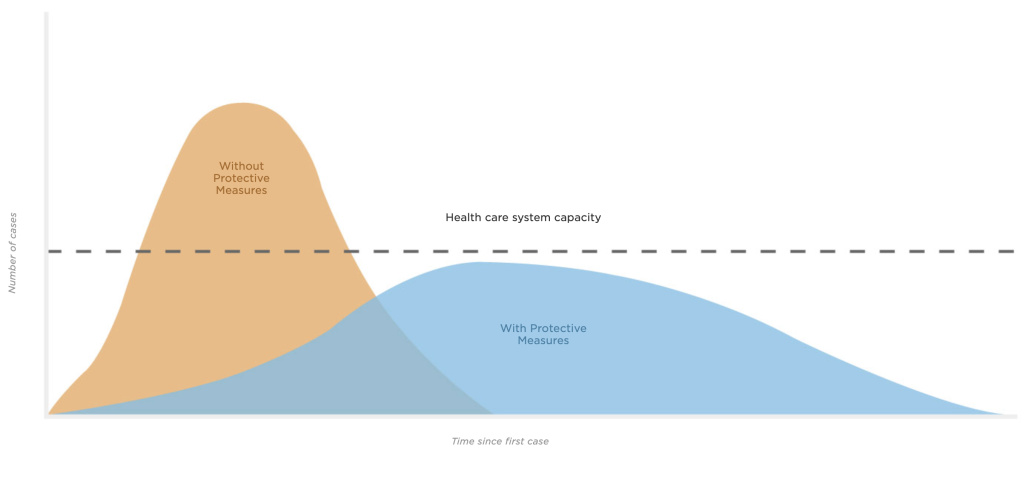

Flattening The Curve And Seeing The Shift From Greed To Fear

read more

Page load link

Go to Top