Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Contracts

April 29, 2020

Analysis & Research

,

Brokers, Agents, MLS, NAR

,

Explainer

,

Housing Trends & Cycles

,

Statistics, Metrics & Data

Contract Data Is Pending Data Is Lagging Data

read more

February 5, 2020

Charts, Maps, Images, Infographics, Video

,

Government, Politics, Regulations & Policy

,

Manhattan

,

The Real Deal

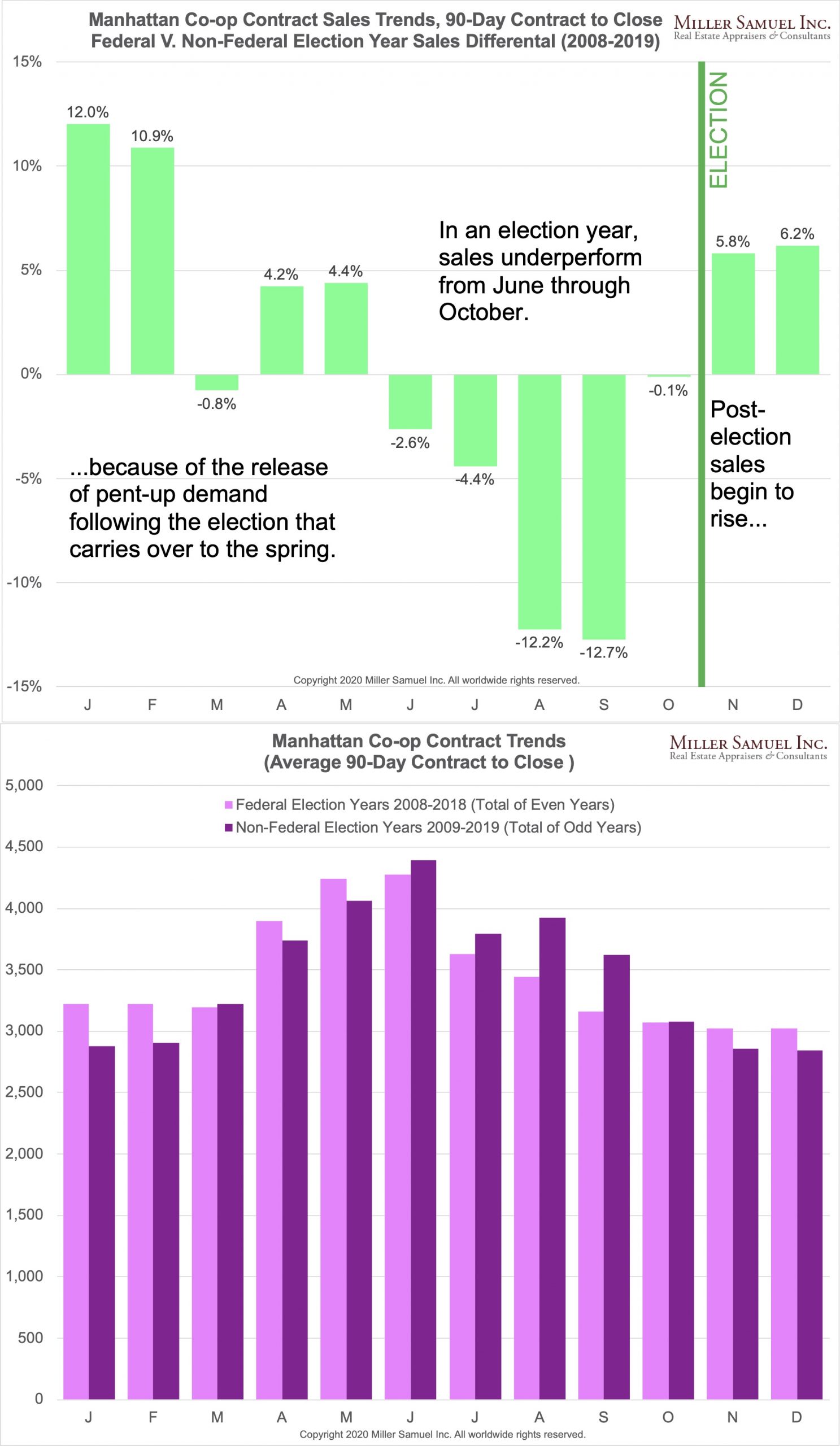

Manhattan Co-op Sales Fall During Federal Election Year

read more

May 4, 2019

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

New York Post

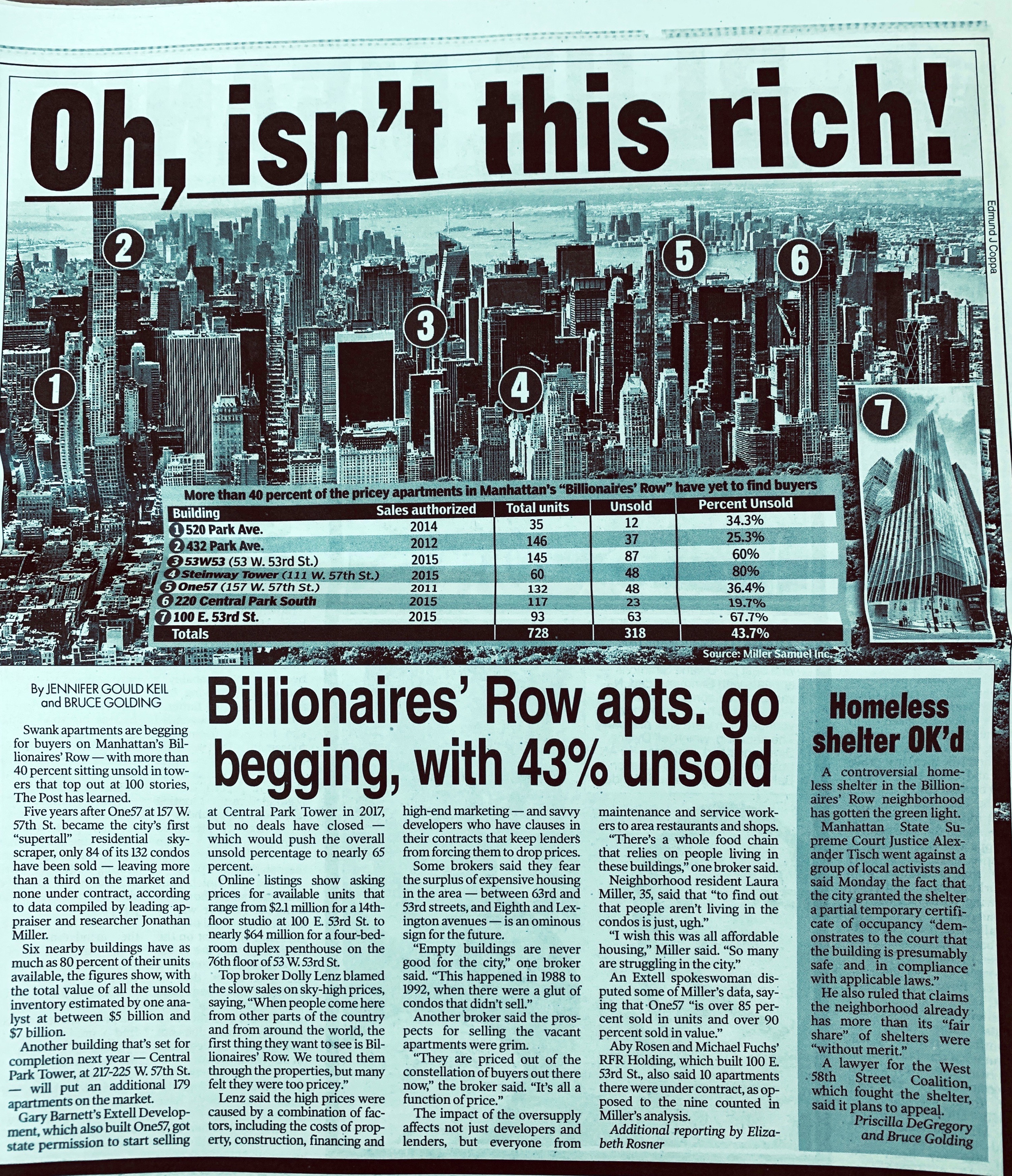

Billionaires Row Continues to be Challenged

read more

May 16, 2015

Charts, Maps, Images, Infographics, Video

,

Curbed

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Manhattan

[Three Cents Worth #281 NY] 6 Graphs That Prove New York Real Estate’s Love of Mondays

read more

September 29, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Credit, Finance, Mortgage, Rates

,

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

Bloomberg View Column: Giant Condo Tower Needs More Billionaires

read more

May 29, 2014

Housing Trends & Cycles

,

Market Reports

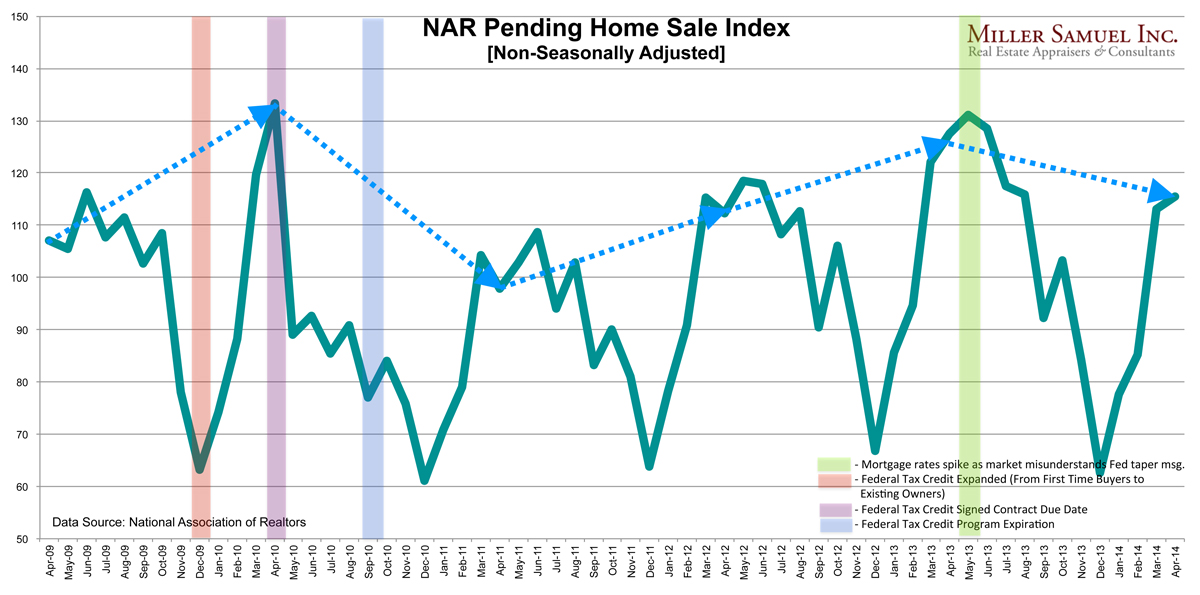

Pending Home Sales Fall Short of Year Ago Sales Surge

read more

February 24, 2014

Humor or Whimsy

,

Language, Jargon & Quotes

,

Law, Ethics & Fraud

Best Real Estate Lawsuit Prose EVER

read more

Page load link

Go to Top