Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Favorites

April 16, 2014

Books & Movies

,

Humor or Whimsy

,

New York City

,

Time Out

Nathan Pyle’s NYC Basic Tips and Etiquette Book Now Available!

read more

March 25, 2014

Amenities, Adjustments & Value Logic

,

Manhattan

,

Media

,

New York Magazine

Repost: Measuring Manhattan Values By Floor Level

read more

March 9, 2014

Appraising

,

Government, Politics, Regulations & Policy

,

Op-Ed

It’s time to debunk the debunking of the 3 biggest myths about your AMC

read more

December 27, 2012

Appraising

,

Credit, Finance, Mortgage, Rates

Appraising for AMCs Can Be Like Delivering Pizza

read more

December 5, 2012

Adventures in Media & Marketing

,

Appraising

A La Mode Software Tells Our Appraisal Story

read more

December 3, 2012

Amenities, Adjustments & Value Logic

,

Appraising

,

New York Magazine

,

New York Times

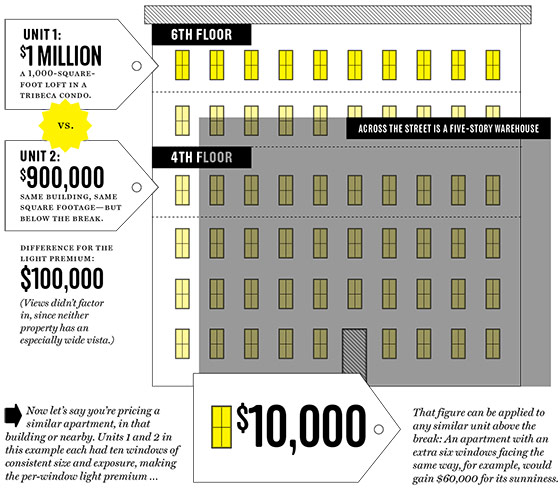

Valuing the Light in Your Condo or Co-op

read more

February 7, 2012

Douglas Elliman

,

Federal Reserve, New York

,

Historical, Landmark, Milestone

,

Manhattan

,

New York Times

Change is Constant: 100 Years of New York Real Estate

read more

June 9, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Charts, Maps, Images, Infographics, Video

,

Manhattan

,

The Real Deal

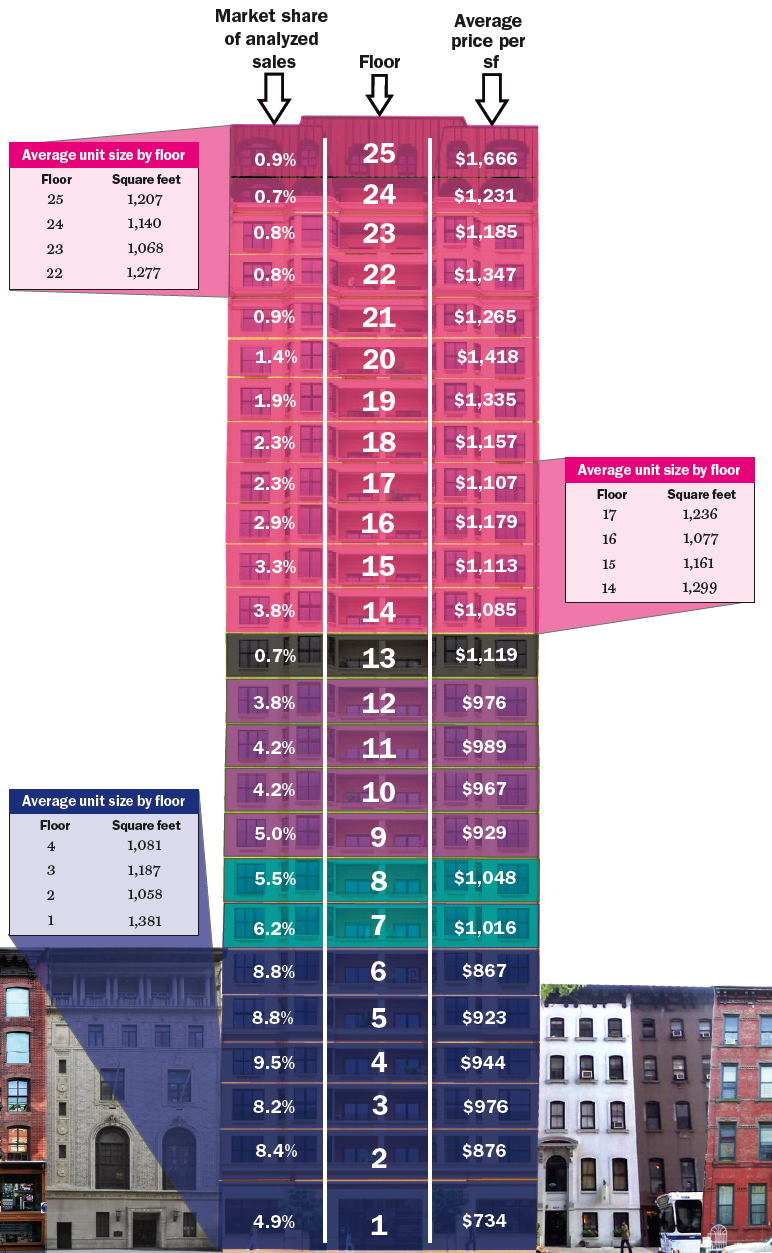

[ChartFloor] Manhattan Price Per Floor Breakdown

read more

May 5, 2010

Amenities, Adjustments & Value Logic

,

Appraising

,

Manhattan

[Terra Logic] Understanding The Value of Manhattan Apartment Outdoor Space

read more

July 5, 2009

Books & Movies

,

Boom Bubble Bust

,

Canada

,

Credit, Finance, Mortgage, Rates

,

Wall Street, Financial Services

Lobster Prices And Subprime Lending

read more

May 19, 2009

Humor or Whimsy

,

Media

,

The Real Deal

1-Across Is No Puzzle

read more

September 19, 2008

Time Out

Talk Like A Pirate Day: September 19, 2008

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top