Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Federal Reserve Bank

May 31, 2014

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Law, Ethics & Fraud

,

Wall Street, Financial Services

Spectacular TED Talk on The US Financial Crisis: How it Happened + How to Prevent

read more

May 10, 2014

Bloomberg News

,

Economy

,

Federal Reserve Bank

,

Housing Trends & Cycles

[Video] “Housing…will be a Necessary Casualty”

read more

March 27, 2014

Analysis & Research

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Market Reports

Pending Home Sales Down 10.2% YOY And That’s Not A Bad Thing

read more

March 26, 2014

Appraising

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Regulators Turn Focus on AMCs, Proposals Include Hiring “Competent” Appraisers

read more

March 20, 2014

Bloomberg News

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Housing Trends & Cycles

,

Media

,

New York City

Talking Interest Rates, Housing on Bloomberg TV’s ‘Surveillance’

read more

March 28, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

Money for Nothing Movie Trailer

read more

February 14, 2013

Celebrity, Pop Culture

,

Douglas Elliman

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

,

RealtyTrac

,

The Real Deal

Housing Data as Pop Culture

read more

February 6, 2013

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

,

New York Times

Tight Credit Is Causing Housing Prices to Rise

read more

December 4, 2012

Brooklyn

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Housing Indices & Portals

[NewYork Fed] Excellent Mapping of Housing’s Recovery Process in Region

read more

November 5, 2012

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

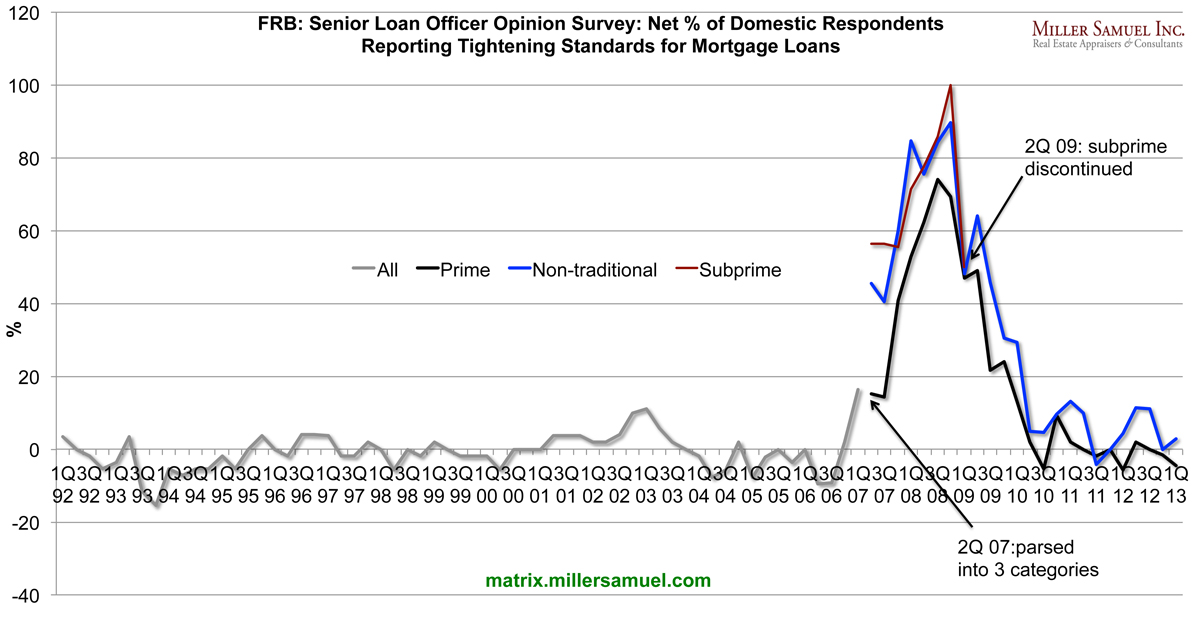

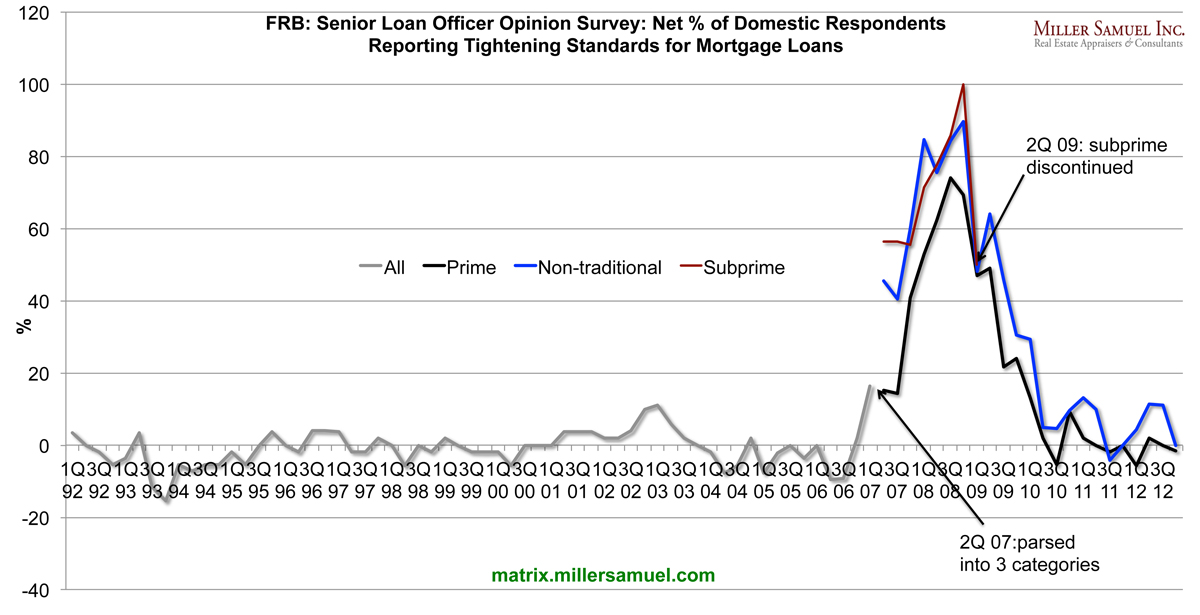

Federal Reserve: Mortgage Underwriting Standards Haven’t Eased

read more

September 18, 2012

Bloomberg News

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Media

[In The Media] Bloomberg Surveillance 9-18-12 QE3, Low Rates and Housing

read more

June 7, 2012

Boom Bubble Bust

,

Distressed Housing

,

Elliman Reports

,

Federal Reserve Bank

,

Wall Street Journal

,

Weather & Natural Disasters

Visualizing US Distressed Sales – Katrina Edition

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top