Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Barry Ritholtz

December 27, 2023

Bloomberg Radio

,

Brokers, Agents, MLS, NAR

,

Homebuying Process

Bloomberg’s At The Money Podcast (ATM): The Best Way To Sell A House

read more

November 17, 2023

Bloomberg Radio

,

Brokers, Agents, MLS, NAR

,

Homebuying Process

Bloomberg’s At The Money Podcast (ATM): The Best Way To Buy A House

read more

September 5, 2023

Bloomberg Radio

,

Homebuying Process

,

Housing Trends & Cycles

Bloomberg’s Masters in Business: Jonathan Miller on High Mortgage Rates

read more

May 1, 2021

Appraising

,

Bloomberg Radio

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Housing Note

,

Housing Trends & Cycles

[Podcast] Masters In Business: Jonathan Miller on the Real Estate Industry

read more

April 5, 2020

Bloomberg Radio

Bloomberg Radio’s Barry Ritholtz – Masters in Business Show: Jonathan Miller on Real Estate After the Coronavirus

read more

March 11, 2019

Bloomberg TV

,

Charts, Maps, Images, Infographics, Video

,

Development, Construction, Architecture & Land

,

Luxury, Super, Ultra, Mega

,

Manhattan

,

Sales

Bloomberg TV 3-11-19: The Malling of Hudson Yards

read more

December 30, 2014

Bloomberg View

,

Housing Trends & Cycles

,

Interviews

,

Public Speaking

Barry Ritholtz’ Bloomberg Masters in Business: Me

read more

May 21, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Homebuying Process

,

Op-Ed

We’re at “Peak Anti-Homeownership”

read more

March 16, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Op-Ed

,

Wall Street Journal

The Bi-Partisan Fannie and Freddie Solution That Isn’t A Fix

read more

February 25, 2014

Bloomberg News

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

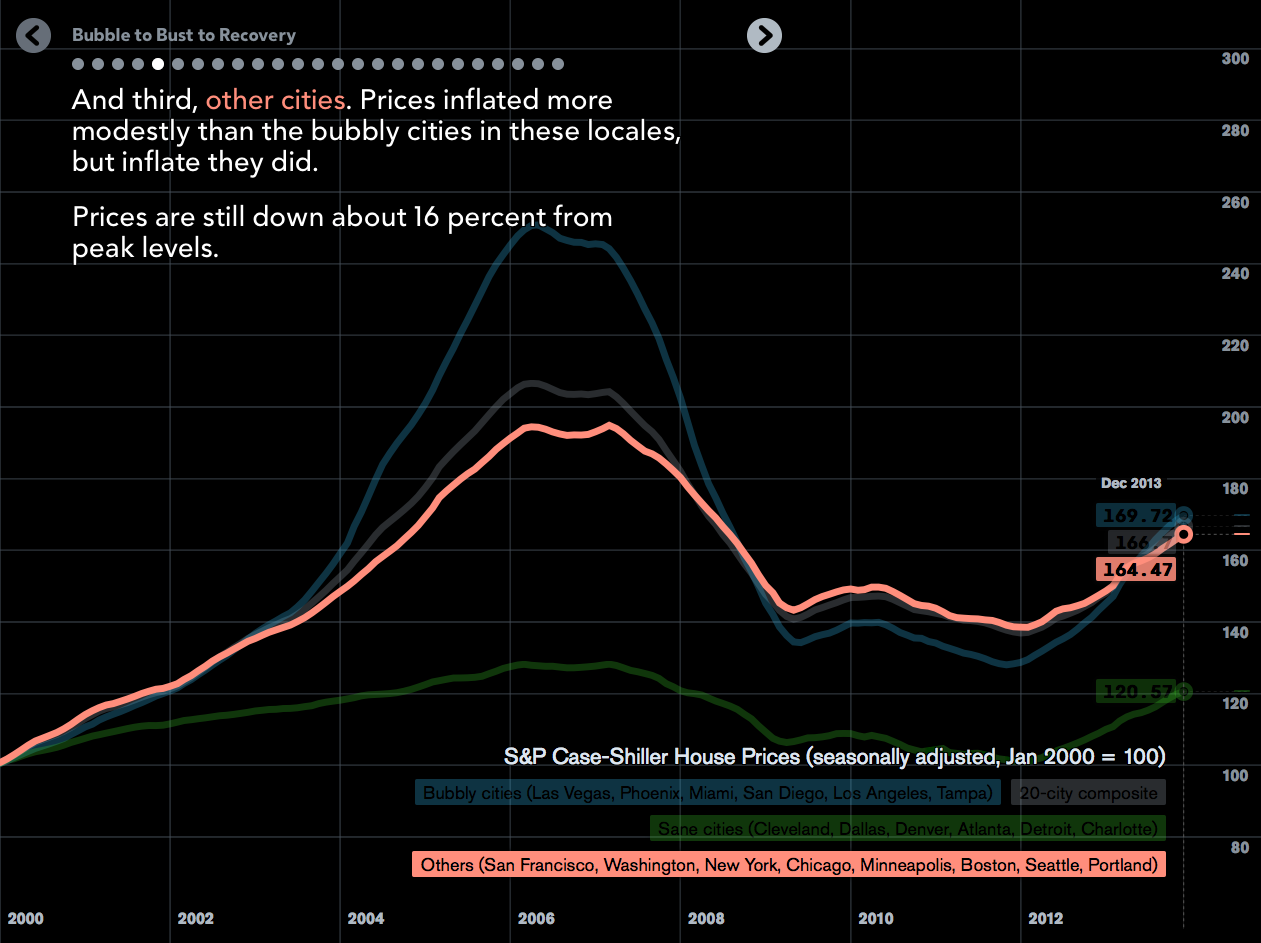

Bloomberg View’s Super Cool Visual: Bubble to Bust to Recovery

read more

August 20, 2013

Economy

,

Housing Indices & Portals

Housing Can’t “Recover” Until Fundamentals Recover

read more

March 28, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

Money for Nothing Movie Trailer

read more

1

2

Next

Load More Posts

Page load link

Go to Top