Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Boom Bubble Bust

June 16, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

,

Economy

,

Federal Reserve, New York

Housing is a Drag: US Student Debt Bubble Made Worse by the Baby Boomer Nanny State

read more

May 31, 2014

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Federal Reserve Bank

,

Law, Ethics & Fraud

,

Wall Street, Financial Services

Spectacular TED Talk on The US Financial Crisis: How it Happened + How to Prevent

read more

May 21, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Homebuying Process

,

Op-Ed

We’re at “Peak Anti-Homeownership”

read more

May 4, 2014

Boom Bubble Bust

,

Canada

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

International

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

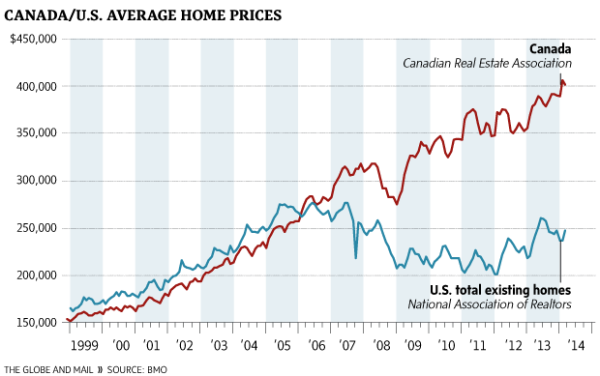

Canadian Housing Prices Now Pushed Up Same Way as US

read more

February 25, 2014

Bloomberg News

,

Boom Bubble Bust

,

Charts, Maps, Images, Infographics, Video

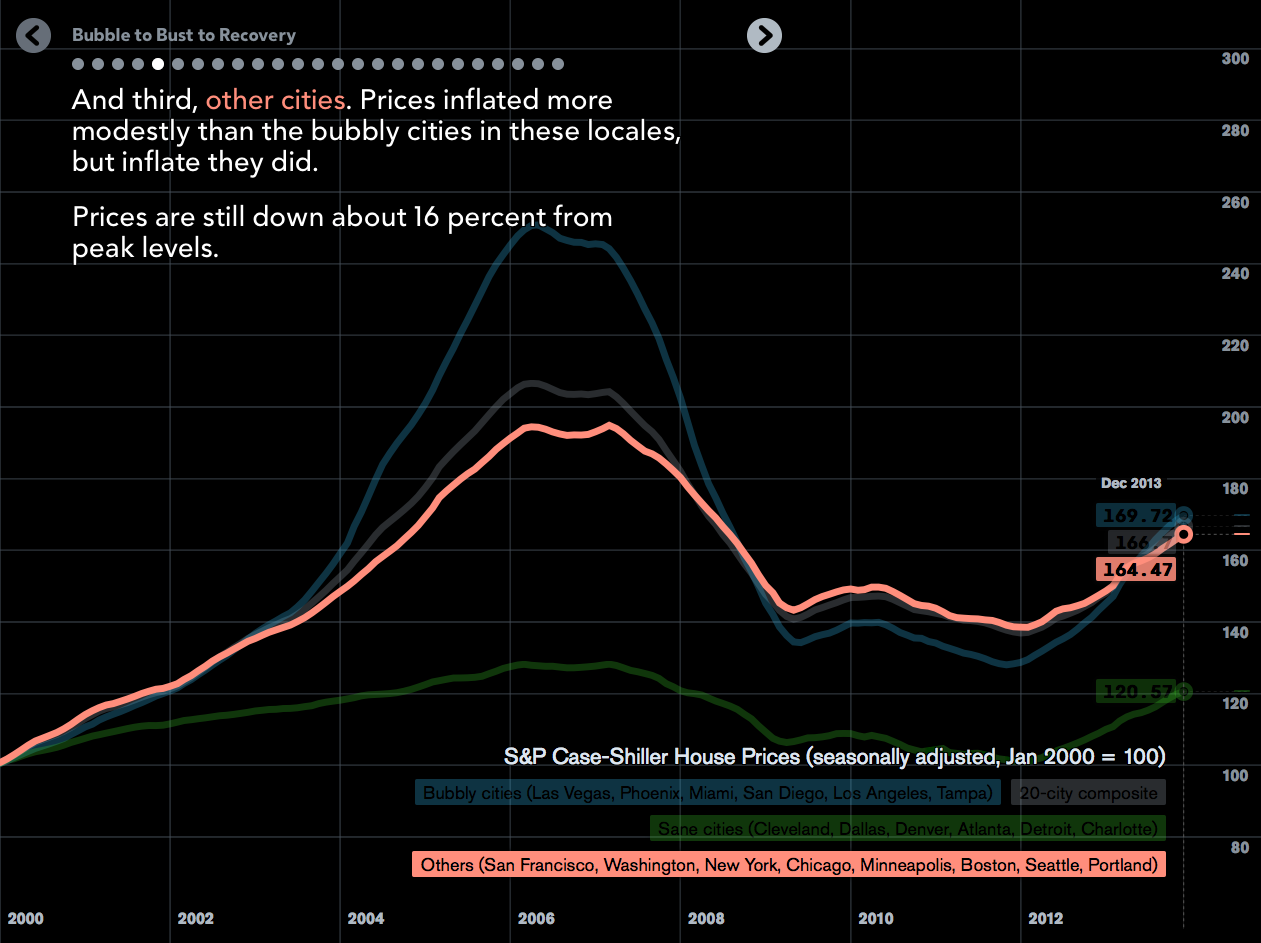

Bloomberg View’s Super Cool Visual: Bubble to Bust to Recovery

read more

September 16, 2013

Appraising

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

New York Times

,

Wall Street Journal

The Low Appraisal “Hassle” is a Symptom of a Broken Mortgage Process

read more

July 14, 2013

Boom Bubble Bust

,

Douglas Elliman

,

Manhattan

,

New York Times

Appearing on New York Times’ Page One NEVER Gets Old…But It’s A Process

read more

May 29, 2013

Boom Bubble Bust

,

Brooklyn

,

Media

BBC TV On Brooklyn’s Soaring Market

read more

March 28, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Federal Reserve, New York

,

Government, Politics, Regulations & Policy

,

Wall Street, Financial Services

Money for Nothing Movie Trailer

read more

February 5, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Humor or Whimsy

,

Law, Ethics & Fraud

,

New York Times

Talking Heads: Burning Down The House, S&P Style

read more

January 3, 2013

Boom Bubble Bust

,

Manhattan

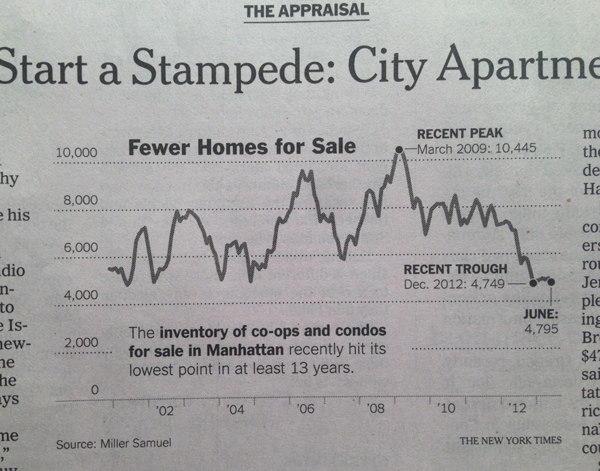

Manhattan Listings Fall off “The Cliff”

read more

December 13, 2012

Analysis & Research

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Housing Trends & Cycles

[Housing Recovery Update] Proclamations Over Reasons, Statistics Over Logic

read more

Previous

1

2

3

Next

Load More Posts

Page load link

Go to Top