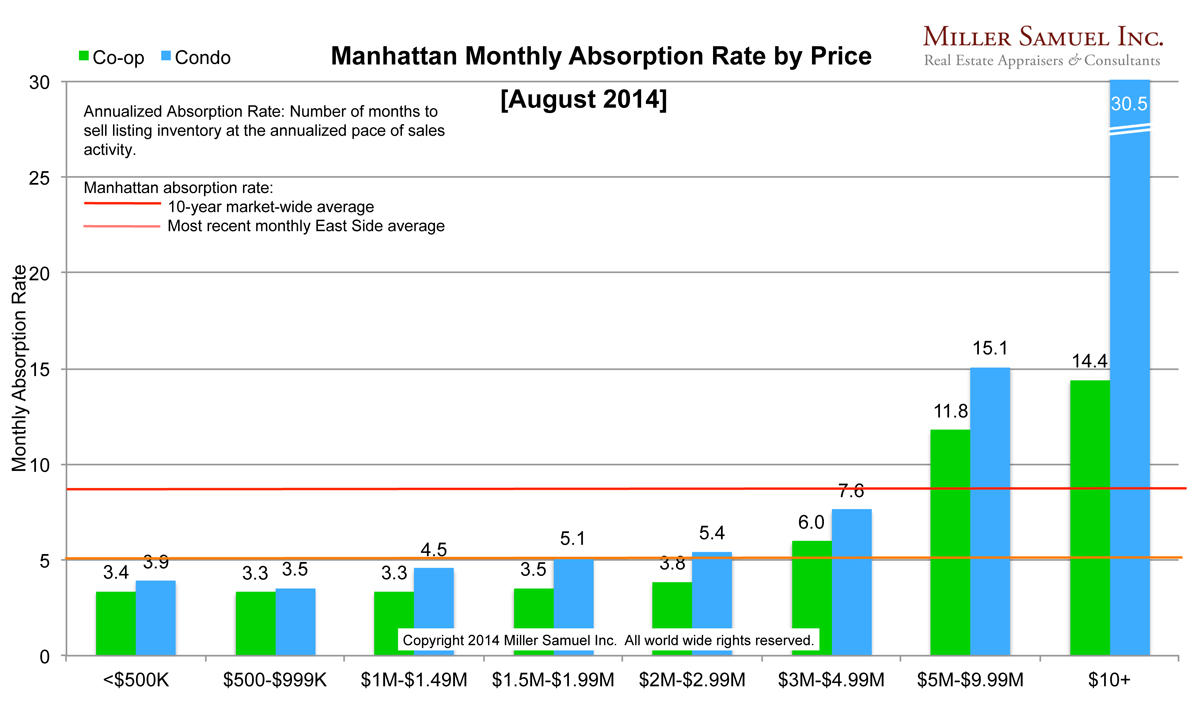

[click to expand] Thoughts Not a big difference from last [...]

Matrix BlogJonathan Miller2024-01-03T19:24:58-05:00

[click to expand] Thoughts Not a big difference from last [...]

21 West 38th Street, 15th Floor New York, NY 10018

© Miller Samuel Inc. 2026 • All Rights Reserved • Website by BlankSlate