Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Hurricane Katrina

August 31, 2014

Blogging Off The Matrix

,

Bloomberg View

,

Crime, Protests, Social-Unrest

,

Housing Indices & Portals

,

Migration, Psychology, Demographics

,

Weather & Natural Disasters

Bloomberg View Column: The Myth of Real Estate Stigma

read more

June 7, 2012

Boom Bubble Bust

,

Distressed Housing

,

Elliman Reports

,

Federal Reserve Bank

,

Wall Street Journal

,

Weather & Natural Disasters

Visualizing US Distressed Sales – Katrina Edition

read more

May 14, 2007

New York Times

,

South Florida

,

Taxes, Insurance, Fees

,

Weather & Natural Disasters

Insurance Market Forces: Greater Than Category 5

read more

March 12, 2007

Development, Construction, Architecture & Land

,

Government, Politics, Regulations & Policy

,

New York Times

,

Taxes, Insurance, Fees

,

Weather & Natural Disasters

Talkin’ About The Weather Around The House (In Your Hip Boots)

read more

September 20, 2006

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

RealtyTrac

,

Rentals, Investing

,

Weather & Natural Disasters

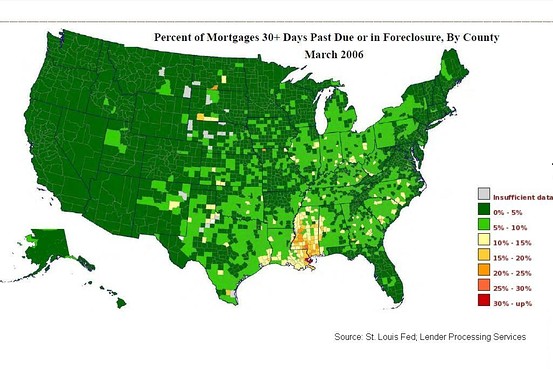

Mortgages: Wondering Where All The Delinquents Are

read more

January 23, 2006

Development, Construction, Architecture & Land

,

International

,

New York Times

,

Weather & Natural Disasters

The US and Mexico Cement Agreement On Imports

read more

January 11, 2006

Adventures in Media & Marketing

,

Boom Bubble Bust

,

Economy

,

Federal Reserve Bank

,

Historical, Landmark, Milestone

,

Migration, Psychology, Demographics

,

New York Times

,

Weather & Natural Disasters

In Good Times and Bad, Negative Milestones Often Define The Real Estate Market

read more

December 20, 2005

Boom Bubble Bust

,

Economy

,

Weather & Natural Disasters

Fannie Mae: Regional Variations In Mortgage Delinquencies Will Make The Overall Numbers Edge Up A Bit

read more

December 14, 2005

Boom Bubble Bust

,

Economy

,

Federal Reserve Bank

,

Wall Street Journal

,

Weather & Natural Disasters

Greenspanspeak Nears Peak: Fed Moves Toward Neutral On Rates

read more

November 28, 2005

Boom Bubble Bust

,

Economy

,

Language, Jargon & Quotes

,

Migration, Psychology, Demographics

,

Weather & Natural Disasters

Fill In The Blank With The Latest Catchphrase: Housing “Expansion”

read more

October 30, 2005

Economy

,

Migration, Psychology, Demographics

,

Weather & Natural Disasters

The Inflation Engine Pushes Mortgage Rates Up: Big Oil Has Some Explaining To Do

read more

October 22, 2005

Boom Bubble Bust

,

Development, Construction, Architecture & Land

,

Economy

,

Migration, Psychology, Demographics

Just Can’t Stop: Surge In Housing Starts and Permits

read more

1

2

Next

Load More Posts

Page load link

Go to Top