Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› WSJ

June 6, 2024

Appraising

,

Explainer

[WSJ Digital] The Total Renovations Behind This Home’s $1.8M Listing Price

read more

June 25, 2015

Credit, Finance, Mortgage, Rates

,

Fox Business

,

Wall Street, Financial Services

[Video] Fox Business ‘Risk & Reward’ w/Deirdre Bolton 6-25-15

read more

March 17, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Wall Street Journal

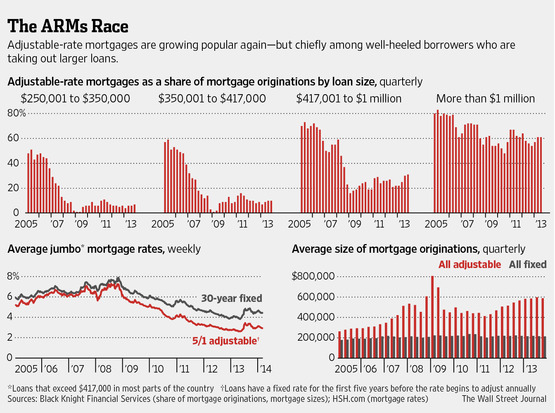

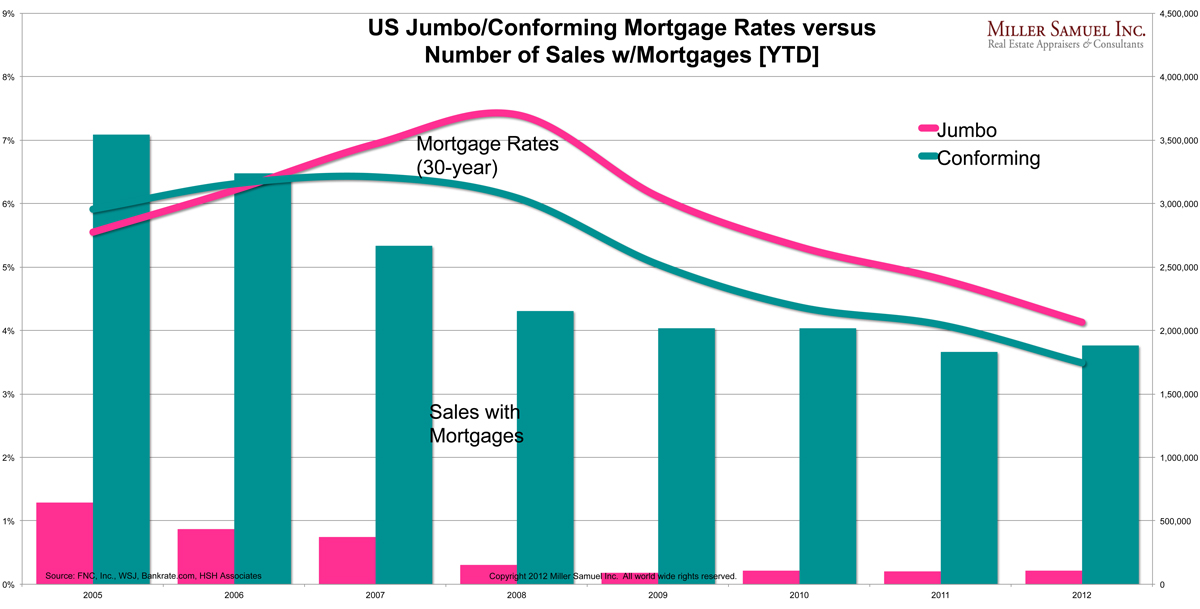

With Plunge in Loan Volume, Lenders Push ARMs to Jumbo Borrowers

read more

March 16, 2014

Charts, Maps, Images, Infographics, Video

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Op-Ed

,

Wall Street Journal

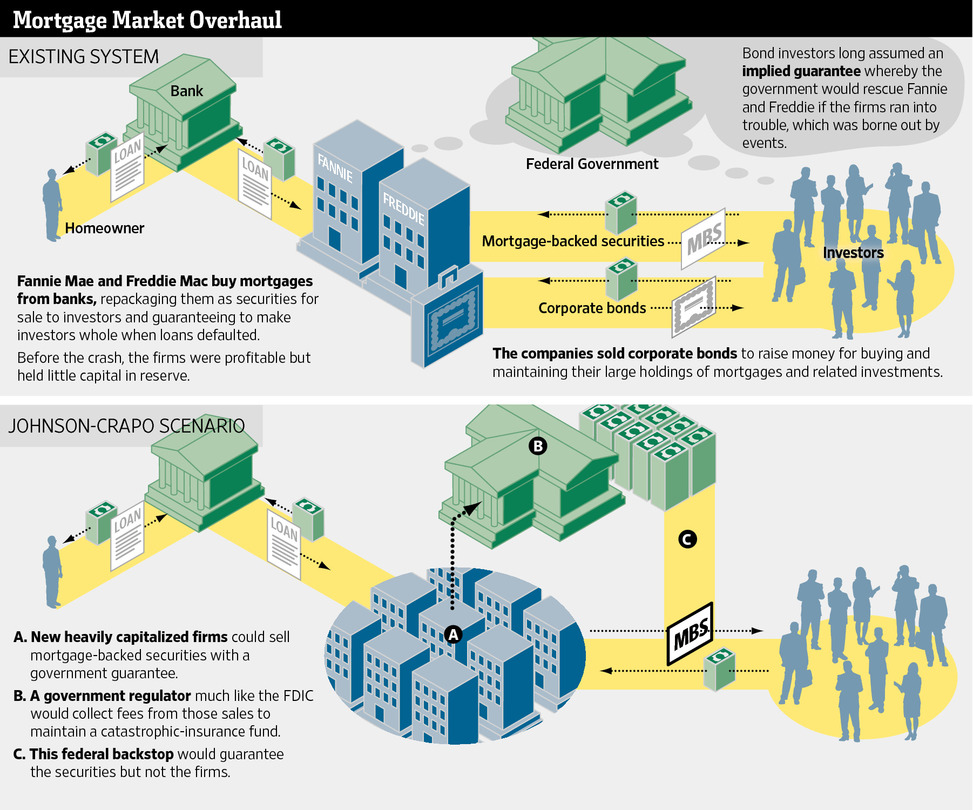

The Bi-Partisan Fannie and Freddie Solution That Isn’t A Fix

read more

July 1, 2013

Charts, Maps, Images, Infographics, Video

,

Economy

,

Wall Street Journal

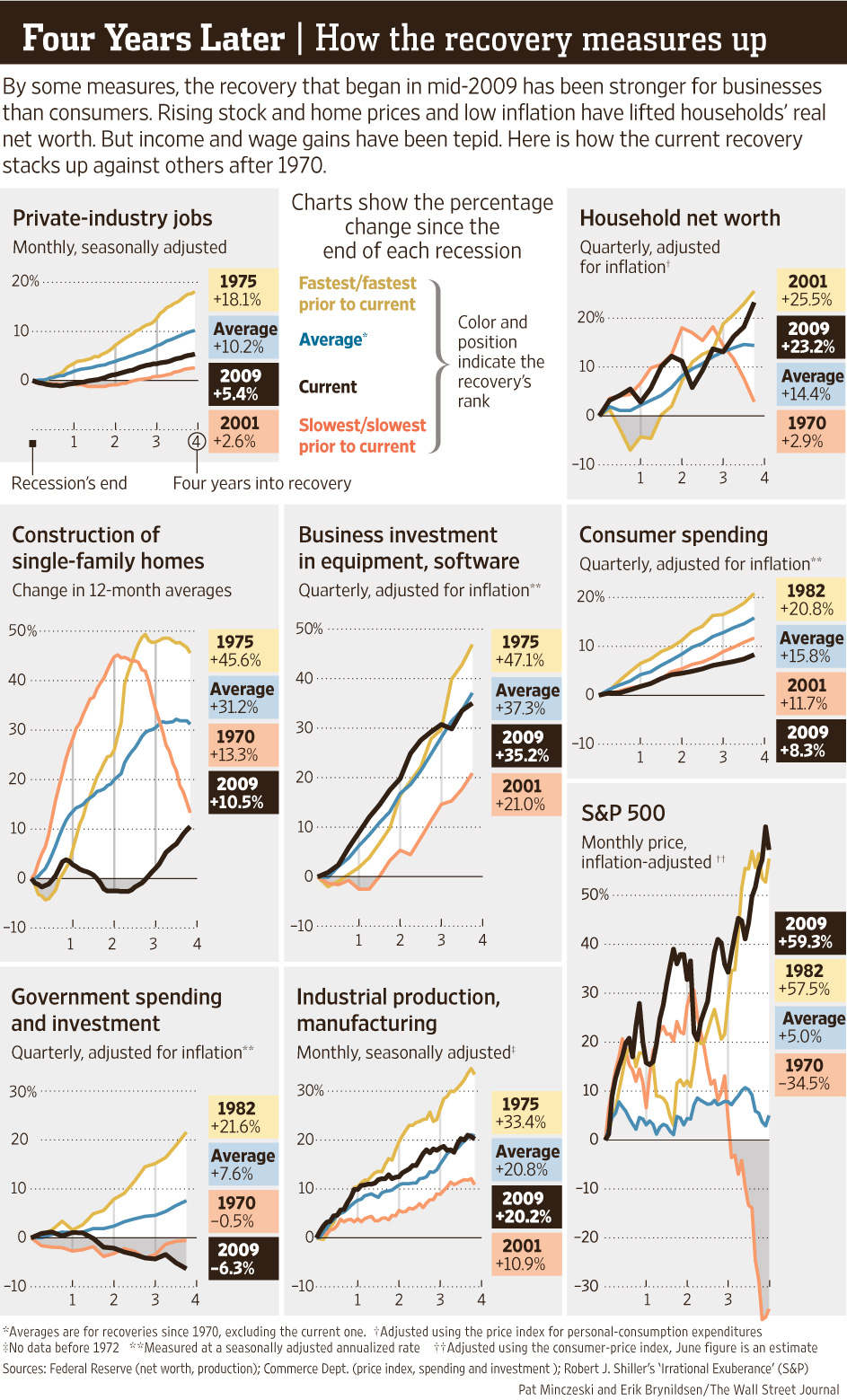

Cool WSJ Infographic on Economic Recovery Since End of Recession

read more

January 29, 2013

Hamptons/North Fork

,

Taxes, Insurance, Fees

,

Wall Street Journal

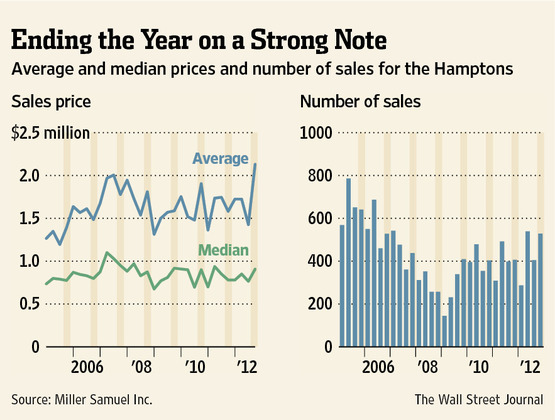

Hampton Year End Sales And Price Spike, Fiscal Cliff Style

read more

December 1, 2012

Appraising

,

Law, Ethics & Fraud

,

Media

,

Wall Street Journal

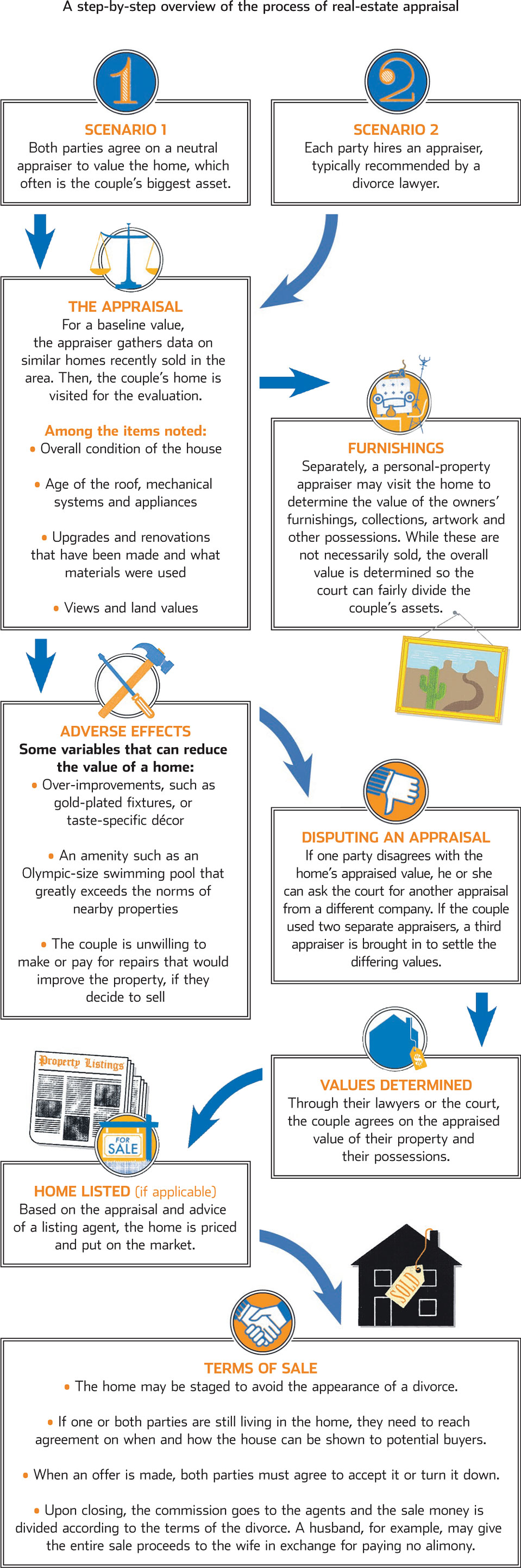

Divorce Valuations: Appraiserville Meets Splitsville

read more

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

June 9, 2012

Elliman Reports

,

Housing Indices & Portals

,

Trulia

,

Wall Street Journal

,

Weather & Natural Disasters

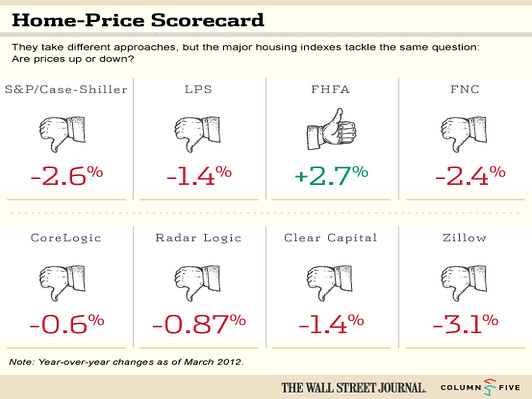

[WSJ] The Crazy 8: Comparing Results of National Home Price Indices

read more

Page load link

Go to Top