Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› S&P/Case-Shiller 20-City index

November 30, 2016

Charts, Maps, Images, Infographics, Video

,

Historical, Landmark, Milestone

,

Housing Indices & Portals

Declaring A Housing Recovery Using A Threshold Based on Fraud

read more

August 25, 2015

Analysis & Research

,

Charts, Maps, Images, Infographics, Video

,

Housing Indices & Portals

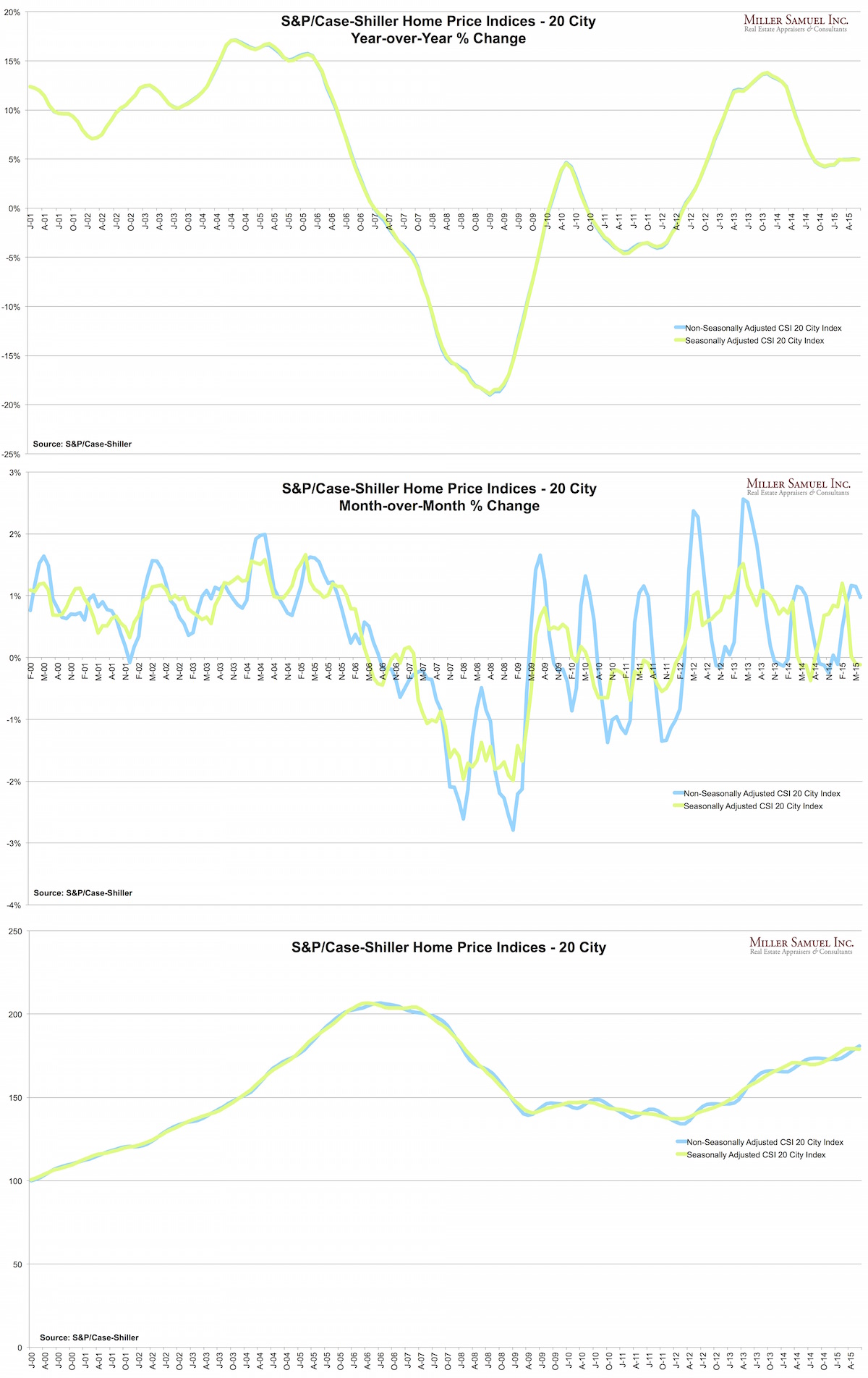

Explainer: Three Ways to Look at S&P/Case-Shiller Index Results

read more

June 3, 2015

Affordability, Affordable Housing

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

,

Economy

,

Government, Politics, Regulations & Policy

,

Rentals, Investing

,

Sales

,

Suburban, Urban, Commuting

Bloomberg View Column: Costly City Housing Is an Economic Drag

read more

Page load link

Go to Top