Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Jumbo Mortgage

November 27, 2012

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

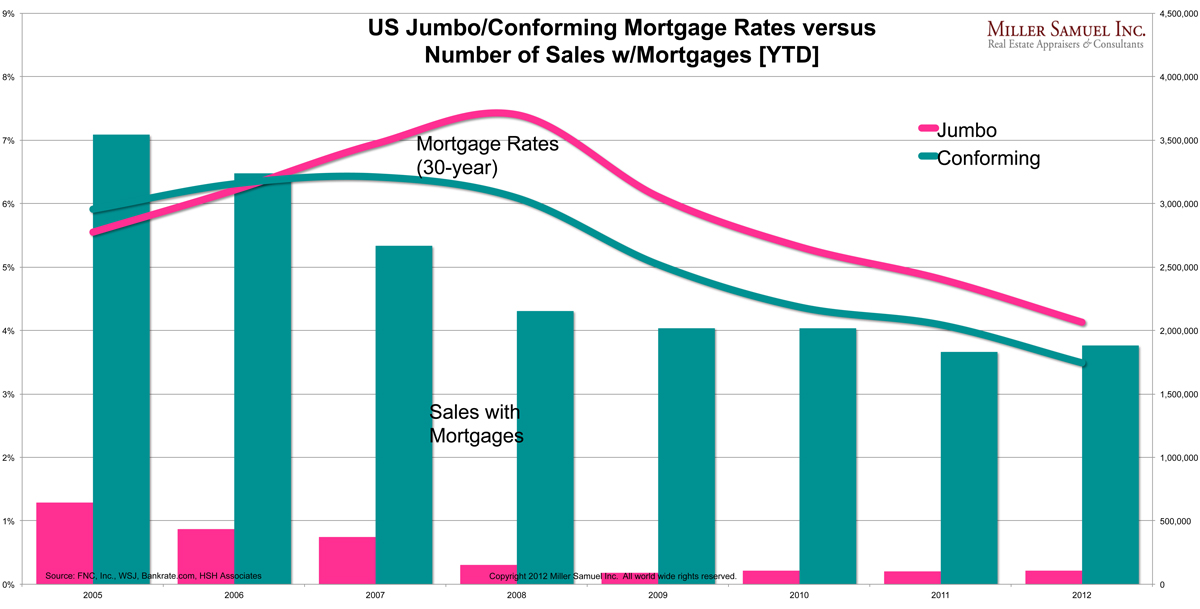

Get Down With It: Falling Mortgage Rates Are Not Creating Housing Sales

read more

November 26, 2012

Credit, Finance, Mortgage, Rates

,

Housing Indices & Portals

,

Wall Street Journal

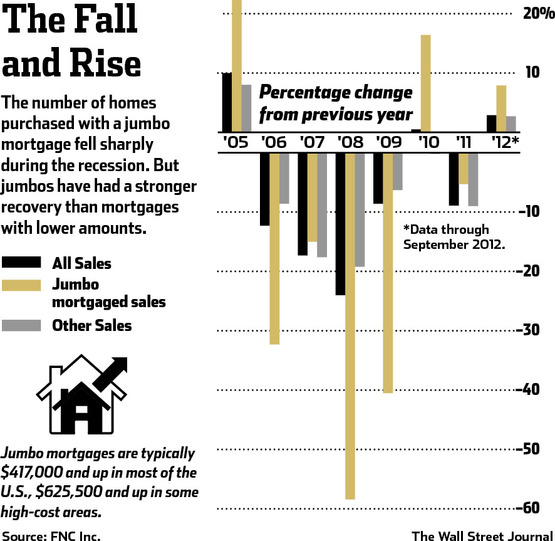

Jumbos Fell Harder, Now Rising Faster, But Off Low Base

read more

March 24, 2009

Appraising

,

Credit, Finance, Mortgage, Rates

,

Migration, Psychology, Demographics

B of A Goes Jumbo Just In Time, Hides Countrywide, Wants Identity (Mine)

read more

December 5, 2008

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Economy

,

Government, Politics, Regulations & Policy

,

Housing Indices & Portals

,

International

,

IRS

,

New York Times

,

Wall Street Journal

[Below 1%] Turning Japanese, I Really Think So

read more

April 27, 2008

Credit, Finance, Mortgage, Rates

,

Economy

,

Federal Reserve Bank

,

Government, Politics, Regulations & Policy

[Bail Out] Worried About Future, Banks Spread Out

read more

April 23, 2008

Books & Movies

,

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Government, Politics, Regulations & Policy

,

Migration, Psychology, Demographics

,

Rentals, Investing

[GSE Searchlight] Oversight Is So Not Over

read more

April 8, 2008

Appraising

,

Baltimore

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Wall Street Journal

[WaMu Goes Retail] Wholesale Mortgage Pipeline Goes Dry

read more

March 27, 2008

Baltimore

,

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Government, Politics, Regulations & Policy

,

New York Times

,

RealtyTrac

,

South Florida

,

Wall Street Journal

[OTS] Foreclosures: From Malaise To Disarray

read more

March 19, 2008

Credit, Finance, Mortgage, Rates

,

Economy

,

Government, Politics, Regulations & Policy

,

New York Times

,

Rentals, Investing

Billion Mortgage March: GSEs To Make Waves

read more

February 13, 2008

Credit, Finance, Mortgage, Rates

,

Distressed Housing

,

Economy

,

Government, Politics, Regulations & Policy

,

New York Times

Economic Dog Ready To Be Stimulated By Booster Shot From Trainer

read more

January 26, 2008

Appraising

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Market Reports

,

New Jersey

State Of New Jersey: Otteau December 2007 Contracts

read more

November 29, 2007

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

,

Wall Street Journal

NAR’s Temporary Housing View

read more

1

2

Next

Load More Posts

Page load link

Go to Top