Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› S&P

November 30, 2016

Charts, Maps, Images, Infographics, Video

,

Historical, Landmark, Milestone

,

Housing Indices & Portals

Declaring A Housing Recovery Using A Threshold Based on Fraud

read more

May 27, 2014

Historical, Landmark, Milestone

,

Housing Indices & Portals

,

Housing Trends & Cycles

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

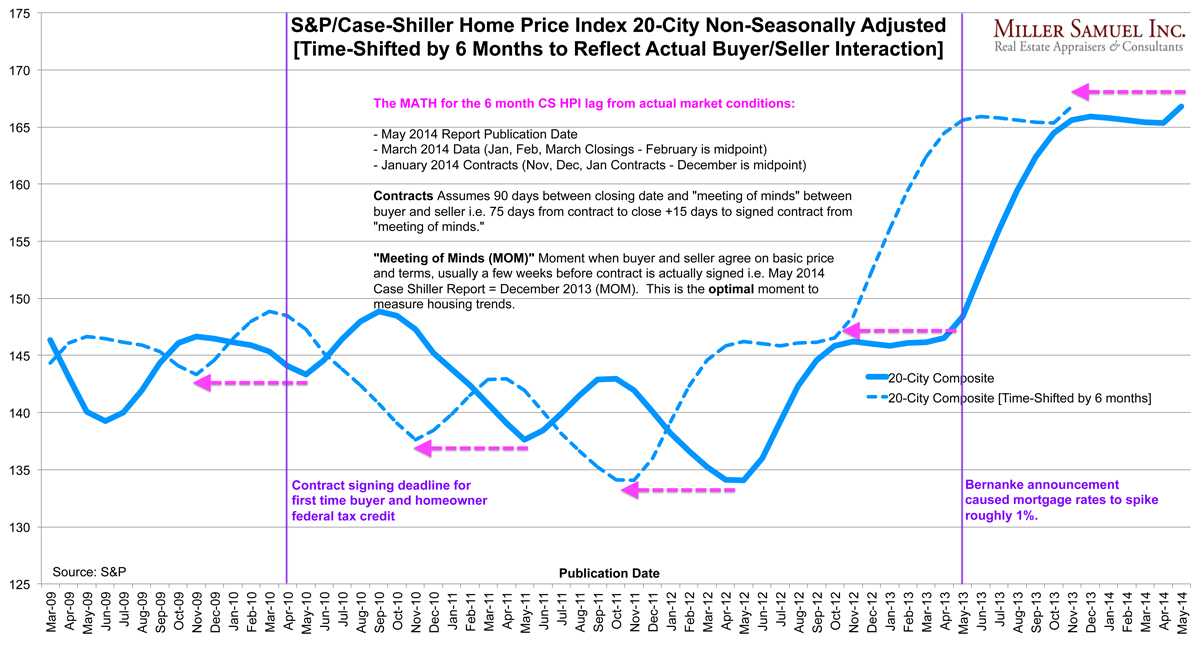

Pulling the Case-Shiller Index Back by 6 Months to Reflect Actual Buyer/Seller Behavior

read more

February 5, 2013

Boom Bubble Bust

,

Credit, Finance, Mortgage, Rates

,

Humor or Whimsy

,

Law, Ethics & Fraud

,

New York Times

Talking Heads: Burning Down The House, S&P Style

read more

September 19, 2005

Boom Bubble Bust

,

Economy

,

Federal Reserve Bank

,

Migration, Psychology, Demographics

,

South Florida

,

Wall Street Journal

S&P: Housing Appreciation Will Ease Gradually, Modestly, Step-By-Step, Bit-By-Bit and Slowly

read more

Page load link

Go to Top