Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› AMC

May 18, 2021

Appraising

,

Continuing Education & Licensing

No Diversity: 96.5% Of U.S. Appraisers Are White

read more

March 18, 2020

Appraising

,

Explainer

,

Government, Politics, Regulations & Policy

Some Financial Institutions Care About The Safety Of Appraisers, While Most Do Not

read more

April 27, 2019

Appraising

,

Continuing Education & Licensing

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

BREAKING The New York State AMC Law Is Now In Effect

read more

August 6, 2017

Appraising

Podcast: Guest hosting ‘Voice of Appraisal’ – Week of August 7, 2017

read more

June 15, 2017

Appraising

,

Government, Politics, Regulations & Policy

[Housingwire] Hey 50-percenters, there is no “appraiser shortage” so knock it off

read more

March 23, 2017

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Doubling Down On Appraisers as ‘Lone Wolves’ – Valuation Review

read more

October 7, 2016

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

Media

Voice of Appraisal Podcast: E123 “Solving Problems with Jonathan Miller!”

read more

October 4, 2015

Appraising

,

Brokers, Agents, MLS, NAR

,

IRS

,

Junk Statistical Analysis, Luck, Superstition and Coincidence

,

Law, Ethics & Fraud

Multi-millionaire Motivational Speaker Dean Graziosi Shares His Appraisal Wisdom

read more

May 31, 2015

Appraising

,

Charts, Maps, Images, Infographics, Video

Infographic: 25 Year Demise of the Bank Appraisal Industry and the Rise of AMCs

read more

January 28, 2015

Appraising

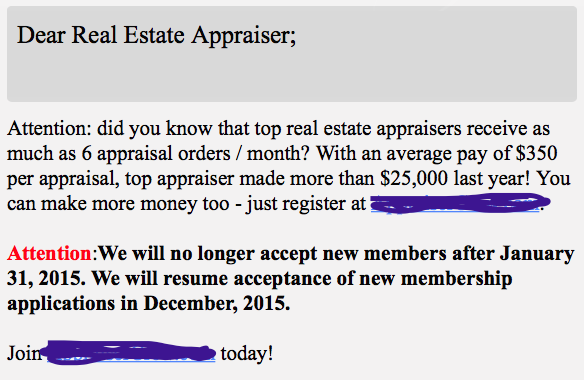

Getting excited about the “Top Appraiser” making $25K last year!

read more

December 26, 2014

Appraising

,

Bloomberg View

,

Charts, Maps, Images, Infographics, Video

Bloomberg View Column: Do Experts Value Your Home More Than You?

read more

October 20, 2014

Appraising

,

Government, Politics, Regulations & Policy

,

Public Speaking

,

Social, Tech, Gadgets, Software

Bad Actors: AMC Appraisal Perspective Through Rhetorical Misdirection

read more

1

2

Next

Load More Posts

Page load link

Go to Top