Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Appraising

August 24, 2017

Appraising

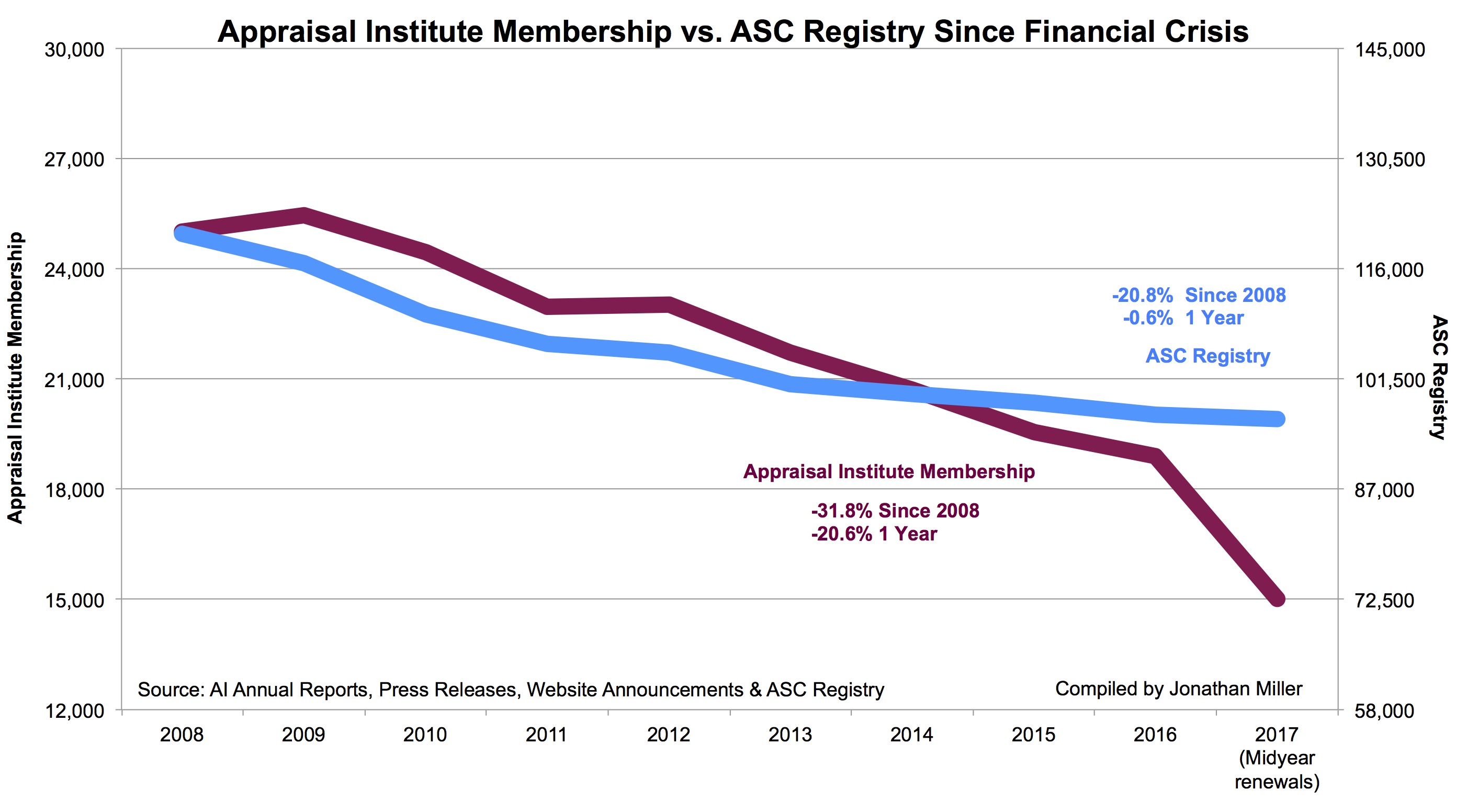

Appraisal Institute Membership Falls Sharply As ASC Registry Levels Off

read more

August 6, 2017

Appraising

Podcast: Guest hosting ‘Voice of Appraisal’ – Week of August 7, 2017

read more

June 15, 2017

Appraising

,

Government, Politics, Regulations & Policy

[Housingwire] Hey 50-percenters, there is no “appraiser shortage” so knock it off

read more

March 23, 2017

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Doubling Down On Appraisers as ‘Lone Wolves’ – Valuation Review

read more

March 8, 2017

Appraising

,

Credit, Finance, Mortgage, Rates

,

Government, Politics, Regulations & Policy

Banks Make Regulations Onerous By Over-Interpreting Them

read more

January 19, 2017

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Voice of Appraisal Podcast: E136 A Deep Dive into A.I. with Jonathan Miller!!!

read more

December 28, 2016

Appraising

,

Law, Ethics & Fraud

Unbelievably, The Appraisal Institute Intimidates A Chapter

read more

December 18, 2016

Appraising

,

Blogosphere

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

Real Estate Industrial Complex versus The Appraisal Institute’s Stealth Culture

read more

December 14, 2016

Appraising

,

Boards & Associations

,

Government, Politics, Regulations & Policy

Incredibly, The Appraisal Institute is taking chapter “excess cash” and charging them for the privilege

read more

December 6, 2016

Appraising

,

Boards & Associations

,

Continuing Education & Licensing

,

Government, Politics, Regulations & Policy

Sadly, The Appraisal Institute is now working against its local chapters

read more

October 7, 2016

Appraising

,

Government, Politics, Regulations & Policy

,

Law, Ethics & Fraud

,

Media

Voice of Appraisal Podcast: E123 “Solving Problems with Jonathan Miller!”

read more

October 4, 2016

Appraising

,

Boom Bubble Bust

,

Manhattan

Miller Samuel at 30, A Short Story

read more

Previous

2

3

4

Next

Load More Posts

Page load link

Go to Top