Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Realtor.com

September 1, 2015

Charts, Maps, Images, Infographics, Video

,

Housing Trends & Cycles

,

Migration, Psychology, Demographics

,

Suburban, Urban, Commuting

,

Trulia

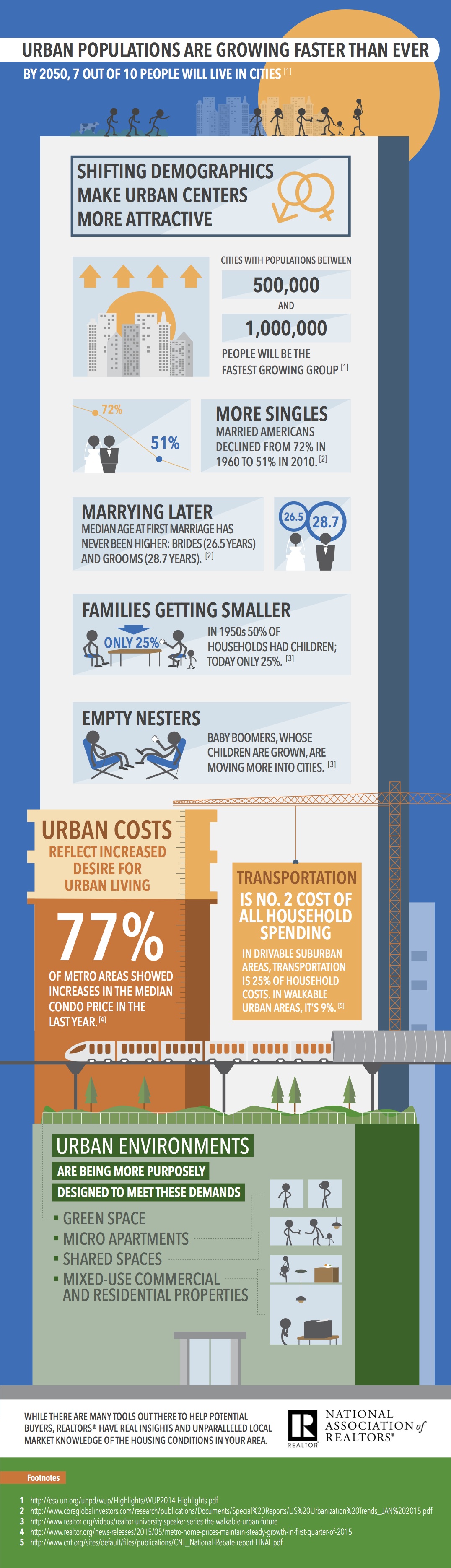

[Infographic] NAR gets into the Urbanization Conversation

read more

November 4, 2012

Brokers, Agents, MLS, NAR

,

Development, Construction, Architecture & Land

,

Humor or Whimsy

,

New York Times

Why Doesn’t NAR Lobby Against Standard Time?

read more

December 1, 2010

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Interviews

,

The Housing Helix

[Press Call] Steve Berkowitz CEO, Sue Stewart SVP, Move, Inc. Realtor.com, Move.com, MortgageMatch.com

read more

December 30, 2007

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Credit, Finance, Mortgage, Rates

,

Economy

Inside Football: Optimistic Contrarian Views On Housing

read more

August 10, 2007

Brokers, Agents, MLS, NAR

,

Inman News

,

New York Times

,

Weather & Natural Disasters

Housing PR Shampoo: Forecast, Revise, Repeat

read more

May 15, 2007

Adventures in Media & Marketing

,

Brokers, Agents, MLS, NAR

,

Social, Tech, Gadgets, Software

Redfin Gets Its 15 in 60 Minutes

read more

May 1, 2007

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Celebrity, Pop Culture

,

Migration, Psychology, Demographics

David Lereah Resigns, Spin Takes A Smoke

read more

March 6, 2007

Adventures in Media & Marketing

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

Lereah: Pickin’ On The Underdog By Using His Mom

read more

February 16, 2007

Adventures in Media & Marketing

,

Boom Bubble Bust

,

Brokers, Agents, MLS, NAR

,

Economy

,

Federal Reserve Bank

,

Market Reports

,

Migration, Psychology, Demographics

,

New York Times

National Housing Prices Slip, Leaving Throats Parched

read more

February 12, 2007

Brokers, Agents, MLS, NAR

,

Government, Politics, Regulations & Policy

,

Migration, Psychology, Demographics

Zillow Gets Zerious About Public Records

read more

February 5, 2007

Adventures in Media & Marketing

,

Brokers, Agents, MLS, NAR

,

Curbed

,

Language, Jargon & Quotes

Real Estate Industrial Complex.com

read more

January 22, 2007

Brokers, Agents, MLS, NAR

,

Celebrity, Pop Culture

,

Law, Ethics & Fraud

,

New York Times

Its A Deal About Nothing: Seinfeld Is Ordered To Pay Commission

read more

1

2

Next

Load More Posts

Page load link

Go to Top