Skip to content

Services

Appraisals

Consulting

Resources

Market Reports

Charts

Matrix Blog

Articles & Research

Press

About

get in touch

Charts

› Business Insider

May 21, 2014

Affordability, Affordable Housing

,

Boom Bubble Bust

,

Homebuying Process

,

Op-Ed

We’re at “Peak Anti-Homeownership”

read more

March 29, 2014

Books & Movies

,

Brokers, Agents, MLS, NAR

,

Charts, Maps, Images, Infographics, Video

,

Homebuying Process

,

International

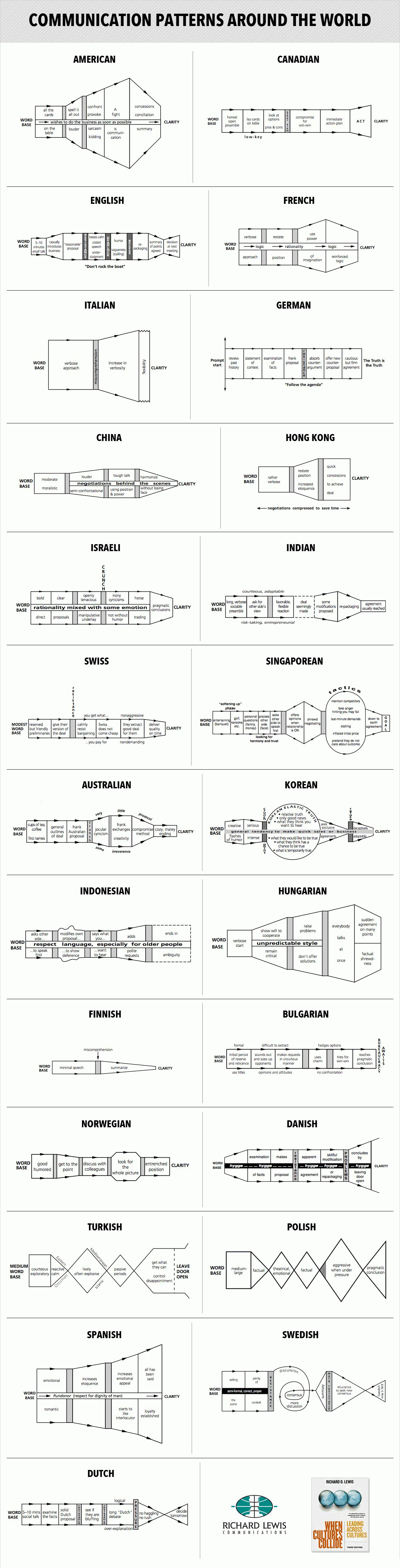

How Real Estate Brokers Can Negotiate With Foreign Buyers, Illustrated

read more

Page load link

Go to Top