In Randall W. Forsyth’s column [Fed’s Worry? It’s Housing, Stupid [Barrons subsc]](http://online.barrons.com/article/SB115878726080369267.html?mod=djemBF):

>To be sure, the FOMC made sure to keep up appearances by mentioning its concern about inflation. They’d be drummed out of the central bankers’ club if they didn’t. “Readings on core inflation have been elevated, and the high levels of resource utilization and of the prices of energy and other commodities have the potential to sustain inflation pressures,” which the FOMC cut and pasted from its Aug. 8 directive…

>It’s clear why inflation is off the Fed’s worry list. But why does housing top it? It’s not just that the Fed inflated the housing bubble (which it did) to offset the effects of the bursting of the tech bubble (which it also blew up.) It’s that housing busts hit the economy far harder than equity collapses.

This is consistent with international housing busts based on [a study by International Monetary Fund in 2003 [pdf]](http://www.imf.org/external/pubs/ft/weo/2003/01/pdf/chapter2.pdf), that Mr. Forsyth cites, for the following reasons, housing market corrections:

* impact consumer spending more than stock market corrections

* impact the banking system

* influence other asset classes like equity prices

* result from credit tightening. Home values decline but mortgages do not decline at the same time.

Because of the last point, making credit easier to get (ie lower mortgage rates) probably won’t solve the current housing problem. Current affordability problems are impacted more by housing prices than by mortgage rates or tight credit. In fact, credit has never been easier to get and mortgage rates are relatively low and seem to be poised to go lower.

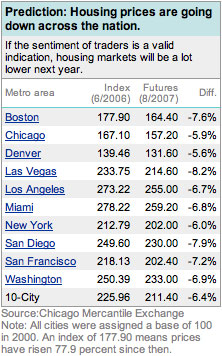

The CME Housing Index seems to support the argument that [housing prices are going to decline. [CNN]](http://money.cnn.com/2006/09/19/real_estate/futures_trading_indicates_housing_drop/index.htm?postversion=2006091911) Trading results were consistent to the actual index for August suggesting some predictive abilities of housing prices, even though the trading volume is too thin to be fully reliable.

Robert Shiller, whose company developed the index, suggests that the index would likely exagerate the decline somewhat due to the risk premium considered by the investors, since they are investing for their opwn protection, not for the local housing markets.

4 Comments

Comments are closed.

But why, then, the map of Leicester?

fatbear – its a map I saw that fit the bill for the post. either you have way too much time on your hands or your have more maps memorized than a Garmin GPS! Thanks though. 😉

2 sec: I saw the map and I noticed the name “Gwendoline Drive” (and the “Close” + “Coppice” above, as well as “The Plantation” as a road name and “Station Road”) – so map might be from an Allingham (or other) mystery I didn’t know, not real, so to google – first google hit is Leicester, thus real – thus the question

These are names and street forms not usual to the city or for that matter other areas in the US – so also wondered why Matrix was using – good choice from graphic point – for a guy in Real Estate you have pretty good graphic chops

Clever! and thanks.