In Q1 08 there was $22T in US residential real estate value and $15T in debt per the Fed (68% LTV). Based on CSI decline trends this year, its probably more like $18T in value now with a 83% LTV. If the prognosticators are accurate and we are halfway through the decline in housing values, it approach 100% LTV in the next two years.

Result: refi wiggle room, more vulnerability to resets (despite lower rates), higher probability of foreclosure and bankruptcy.

Translation: Bad.

There is a fascinating paper published by the San Francisco fed by John Krainer, a senior economist there that sheds more light on the linkage between mortgage lending and the stability of the banking system. Conventional (no pun intended) wisdom is the exclusive domain (no pun intended) of subprime and shoddy Alt-A and prime lending. Of course this is a significant component, but it is also about exposure to and dependence on mortgage lending in its relation to other loan products.

Krainer says

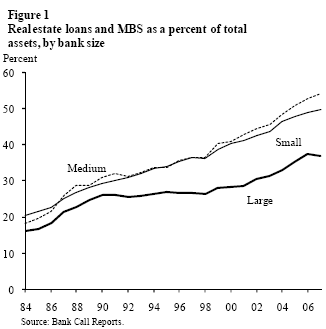

>Over the past several decades, the commercial bank share of total real estate lending has slowly declined as other lenders have entered the market. At the same time, however, the percentage of total bank assets exposed to real estate has increased for banks of all sizes (see Figure 1). In the mid-1980s, for most banks, about 20% of total bank assets were exposed to real estate, and today the exposure is about 50% for small banks (under $500 million in year 2000-level dollars) and medium-sized banks ($500 million to $1 billion in 2000-level dollars) and just under 40% for large institutions. This basic trend is even more pronounced when considering real estate loans as a share of the total loan portfolio: banks now devote about three-quarters of their total loan portfolios to real estate lending.

>The evidence suggests that spillovers of real estate shocks into bank performance are strongest for those types of loans where the collateral is some type of real estate. Spillover effects are strongest for residential loans and construction loans, followed by nonresidential loans. Importantly, all measured effects appear to be much stronger in the 1990s than in the 2000-2007 period. Given that we are currently in a period of declining house prices, it may be reasonable to assume that loan performance will behave more like the observable relationships from the 1990s.

The linkage between mortgage defaults and bank performance is widely understood. Small and mid sized banks were much more aggressive in residential lending since 1980. My guess is that the proliferation of mortgage backed securities in the early 1980s leveled the playing field allowing small banks to grow rapidly this way (remember Countrywide?).

With most of the large banks applying for TARP money, it makes me worry how many small banks didn’t have the legal know how to react as quickly to get on the receiving line of the bailout or more importantly, were a lower priority by the former administration’s Treasury department.

I haven’t digested the whole thing yet, but here is a speech by Fed Governor Elizabeth A. Duke at the Global Association of Risk Professionals’ Risk Management Convention in New York today: Stabilizing the Housing Market: Next Steps.

UPDATE: In response to the 24-7 whining and gloom/doom by many economists (and an appraiser I know), consumers should say: “Well, then what good are you if you can’t tell me what I should do”?