Stagflation that is.

The Beige Book was released today, an anecdotal description of the economies of the 12 member banks of the Federal Reserve. I’ve always liked it as a way to understand what is going on in the region. It is prepared 8x per year in advance of each FOMC meeting, where financial policy is set.

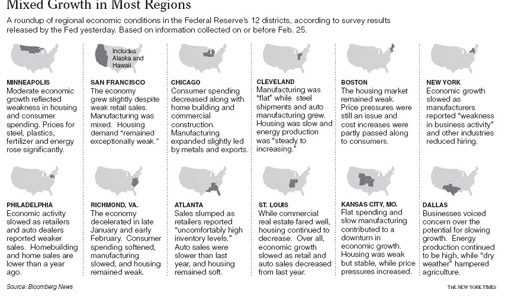

Here’s a summary graphic of each district’s condition in today’s Beige Book. Here’s a good summary article by the NYT’s Floyd Norris.

Residential real estate was reported to remain weak. Here’s an excerpt of all the references to residential real estate:

>Residential real estate markets were generally weak over the last couple of months. Sales were low in every District with very few local exceptions. Sales declines were particularly large in the Boston, Minneapolis, Richmond, and St. Louis Districts; at least some respondents in each of these Districts reported drops in home sales of more than 20 percent year-over-year. Contacts in the Chicago, Kansas City, and Philadelphia Districts cited tight credit conditions as a reason for low sales; each of those Districts either reported or expected stabilization of demand for homes in the low and mid-price ranges.

>Districts that reported home prices all saw overall declines; one exception was the Manhattan co-op and condo market, where prices increased 5 percent compared with a year ago. Inventories remained high as demand was still fairly low. A few contacts in the Chicago, Cleveland, and Richmond Districts reported an increase in inquiries, although this increase in traffic had not yet translated into increased sales. Residential construction declined or remained at low levels in most Districts.

>Even as loan demand for new residential mortgages remained sluggish or declined, lower interest rates prompted increases in refinancing of existing mortgages in a number of Districts, including San Francisco, St. Louis, New York, Richmond, Atlanta, Cleveland, and Chicago. Cleveland cited a small rise in delinquencies, especially for real estate loans, and Atlanta reported an increase in mortgage delinquencies and foreclosures. New York, on the other hand, saw a rise in delinquencies for all loan categories except residential mortgages, which were unchanged. Tight credit standards were reported in the Atlanta, San Francisco, Kansas City, St. Louis, Chicago, Dallas, Richmond, and New York Districts. Kansas City indicated a worsening of overall loan quality, Chicago reported a deterioration of consumer loan quality, and Cleveland also saw a decline in credit quality for business customers and consumers. By contrast, Dallas reported sound credit quality.

There doesn’t seem to be a lot to cheer about, does there?