Last week, the well-known discount real estate brokerage firm Foxtons, closed its operations in the US, which was concentrated in the tri-state (NJ, NY & CT) region. Their web site lists them as having 10,000 listings per year (which doesn’t seem like a lot?)

In their announcement, they seem to suggest that the weak housing market was to blame, however, I think its more related to the business model itself.

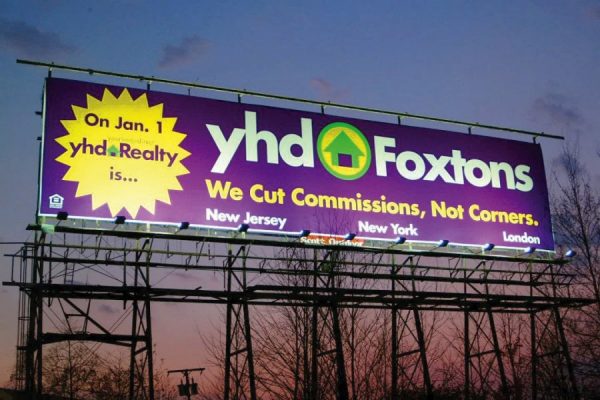

They were originally known as “Your Homes Direct”, morphing into YHD Foxtons, as the British firm bought into them and then eventually dropped the YHD label. Curiously, the firm markets itself as “Full Service Realtors® in NJ, NY & CT.” But they were known as discount real estate brokers.

Their commission structure was originally 2%. I remember seeing the ads on my commute saying something like:

I noticed that some of the houses that were languishing on the market in my town, despite strong market conditions, were switching over to YHD as evidenced by the yard signs, and yet they still languished. I guess that these houses weren’t selling because they didn’t have the right pricing advice.

Or to look at it another way (apply liberal doses of sarcasm here):

if I want to make even more money by not selling my house because its priced too high, then I might as well save even more money by paying a lower commission…er…or something along those lines.

The implication in the Foxtons marketing pitch was that full-service brokers don’t do much for home sellers so why not pocket the difference? It was interesting to me that Foxtons eventually raised their commission to 3%, to about half the going rate to encourage other brokers to show their listings, likely because their overhead was too high.

![]()

I want my MTV…

Foxtons was like watching MTV in the early days. Targeted consumers watched MTV for the music. Targeted consumers listed their house with Foxtons for the low commission.

But both companies found they couldn’t make money the way they had intended so MTV went with reality programming and little or no music while Foxton raised their commission rate and level of service. In the case of the latter, they didn’t adapt fast enough and went under.

During the housing boom, there was a dotcom explosion with innovation running amok looking for solid business plans to latch onto. Some survived and some didn’t. YHD found a suitor in Foxtons, but was not able to find a place in the minds of sellers.

Perhaps the reason for their downfall, is that it is not all about pure cost, but rather a combination of cost, value and service level associated with buying and selling your home. And in a market with lots of competition, full service brokerage firms had better show their mettle and get results with better marketing. Its their chance to recapture market share lost to the discounters. Otherwise, there will be a lot of late nights at real estate brokerage offices spent watching MTV.

Perhaps hybrid versions of these discount models, like Redfin, will survive.

We will have several lean years to find out. And I still don’t want my MTV.

4 Comments

Comments are closed.

Many of the new business model real estate shops condemn the supposed “inefficiencies” of the traditional real estate company, yet with their full-service full-commissioned sales staff, they are best set to weather the storm of a bad economy. Sales agents bear more of the burden of risk individually than the company as a whole and large firms with a large number of agents and a lean management team can make it through a few bad years. Less-motivated and experienced agents may drop out, but the companies themselves will survive and be in a great position when the market heats up again. In a slow market, the costs of sales and marketing increase, so the new models with their paid staff, health insurance and 401K’s are even more prone to failure than the traditional firms.

Mr. Miller,

I have enjoyed your posts, opinions and stats. Between you Roubini, Shiller, and Gross I feel that for the last, well since arriving in the DC area in 2004 and needing to become aware, that you guys have been calling it right and backing it up and educating all at the same time. Many, many blogs out there many pundits on TV. You et al have educated me beyond my widest imagination. I am now at the point where i actually feel like I should leave the federal Govt and make a career as some sort of vulture feeding off what ends up dying off due to greed and picking it up before it spoils.

Anyway, thanks on that. But my question or comment now…since you see where i tend to get my info…is here i am in what 4 years ago was called the insulated, bubble proof, DC MSA.

We were/are far from either..

So i sit with my family and try and predict when to stop renting or what other areas in the MSA to move. My problem come from the fact that our MSA has areas like Fairfax which is now the most expensive place to live in America according to the CB. and we have areas of Southern MD which i happen to live. Its the tri county area of Charles, Calvert and St Marys. Though Charles County borders Prince Georges, we are two distinct demographics…heck even PG county with its size is multiple demos…but I digress.

If you and ytour partners ever are looking for a strangly diverse ‘burb especially one so tied in withh DC commutes…

Please consider Charles, Calvert and St Mary’s as I one day would like to be a homeowner, but do not know if this will ever be the area…..

And quite frankly I could use the help…. The Washington MSA as all the facts figures and advise are given is just too large now to draw any meaningful assumptions or conclusions from.

Very respectfully and thanks again,

Lance

This is a case of a bad business model if I ever saw one. The real estate market here in South Carolina is really making a comeback. I would be willing to bet that we are about to have a strong fall selling season.

It is no surprise that trying to sell a service which can only claim to do it cheaper, rather than better, would eventually fold in today’s marketplace. I think that people demand more today, not less from their agents. Riding on the coattails of a hot market is one thing. Providing real advice and strong marketing to help people sell homes when the market cools a bit, is the job of professionals. There is little value in paying half price for a service that provides almost nothing.